(Bloomberg) — With major earnings letdowns from Netflix Inc. and PayPal Holdings Inc. still fresh in the memory, the bar is high for Nvidia Corp. given that the chipmaker’s valuation far exceeds most U.S.

benchmarks and its rivals.

Even after being caught up in the selloff that’s pummeled fast-growing technology stocks, Nvidia trades at about 49 times projected profit and is 2-1/2 times more expensive than the Philadelphia semiconductor index average, according to Bloomberg data.

Wedbush analyst Matt Bryson expects a “strong” fourth-quarter and outlook when the maker of graphics processors reports later on Wednesday.

“Our concern remains predominantly tied to valuation,” he said.

The stakes have never been this high for Nvidia as the Federal Reserve’s aggressive rate hike path has roiled stocks with extreme valuations.

The shares have been a star performer over the past decade, returning a whopping 7,000%, although more than $170 billion in market value was wiped out in the recent selloff.

What’s more, analysts see more gains: 39 of the 47 that cover the stock have buy ratings and the average price target points to 33% upside in the next 12 months.

However, the combination of rapid revenue growth and a lofty valuation has made Nvidia prone to violent swings, such as the final three months of 2018 when it tumbled more than 50%.

Nvidia shares were down 2.6% at 1:45 a.m.

in New York trading on Wednesday, pushing year-to-date losses over 12%.

Rising Estimates

Investors will be looking for forecasts and commentary in the earnings that show Nvidia is expanding at a clip that can support its valuation, especially in its data center business.

Despite the recent share-price drop, analyst estimates for revenue and profit in the current fiscal year have crept up in the past two months, according to Bloomberg data.

For the fourth quarter, Nvidia is projected to deliver earnings per share excluding some items of $1.22 on revenue of $7.4 billion.

That would represent year-on-year growth of 58% and 48%, respectively.

“Nvidia is very expensive, but it is expected to grow much faster than other names in the space,” Deepon Nag, senior research analyst for technology hardware at Clearbridge Investments, said in an interview.

“The near-term setup looks pretty favorable.”

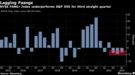

Tech Chart of the Day

The NYSE Fang+ Index, home to the likes of Apple Inc., Amazon.com Inc. and Alibaba Group Holding Ltd., is underperforming the benchmark S&P 500 Index in the first quarter to date.

If losses hold, it will mark a third straight quarter of decline. Investors have been reducing bets on these fast-growing stocks as central bankers prepare to raise rates rapidly.

Top Tech Stories

- Airbnb beat revenue and profit estimates in the fourth quarter, bucking a resurgent wave of Covid-19 infections and heading into this year even stronger than before the pandemic

- Roblox shares tumbled in premarket trading after fourth-quarter bookings missed analysts’ estimates, reflecting a retreat from the pandemic-inspired boost over the last two years

- Mark Zuckerberg unveiled a list of principles for work at Meta Platforms Inc.

in which he calls its employees “Metamates”

- The U.S. Chamber of Commerce is taking up the cause of giant technology companies facing fresh antitrust threats from the Biden administration and Congress

- Alphabet’s Wing unit elevated its leading technology official to head the company as it seeks to rapidly expand its drone delivery operations, including in the Dallas suburbs

(Updates share performance and valuations throughout.)

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.