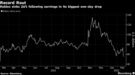

(Bloomberg) — Roblox Corp. tumbled in its worst decline on record after a disappointing earnings report, marking a departure from the double-digit share gains the quarterly updates typically spur for the video-game company.

The 26% slump on Wednesday is the biggest decline for Roblox in the session following its results.

In November, the stock surged 42% after the company reported third-quarter bookings, a measure of sales, that topped analysts’ estimates even as Covid-19 restrictions eased.

Yet, in its fourth-quarter report released after markets closed Tuesday, Roblox reported bookings that fell short of Wall Street estimates.

The company also posted bookings for January, which analysts said were weak and signaled decelerating growth.

“Our prior view assumed RBLX would continue to grow users and bookings at outsized rates through reopening.

We were wrong,” Morgan Stanley analysts led by Brian Nowak wrote in a note, downgrading the stock to equal-weight from overweight.

Roblox jumped 21% on May 11 after posting its first quarterly report as a public company.

In August, when bookings missed Wall Street estimates, the stock slipped just 1.1%.

Besides Morgan Stanley, other analysts remained unmoved by the report. Roblox has 16 buy ratings, three holds and one sell, according to data compiled by Bloomberg.

Firms including Bank of America Corp. and Needham & Co. have touted the company’s growth potential for the metaverse.

The average price target among analysts tracked by Bloomberg is $104, implying nearly 90% return potential for the next 12 months.

Roblox shares are up 23% since the company made its public debut in March.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.