(Bloomberg) — In his 20s, he was a hedge-fund wunderkind. By his 40s, a hedge-fund legend. But suddenly, Chase Coleman is stumbling, and hard.

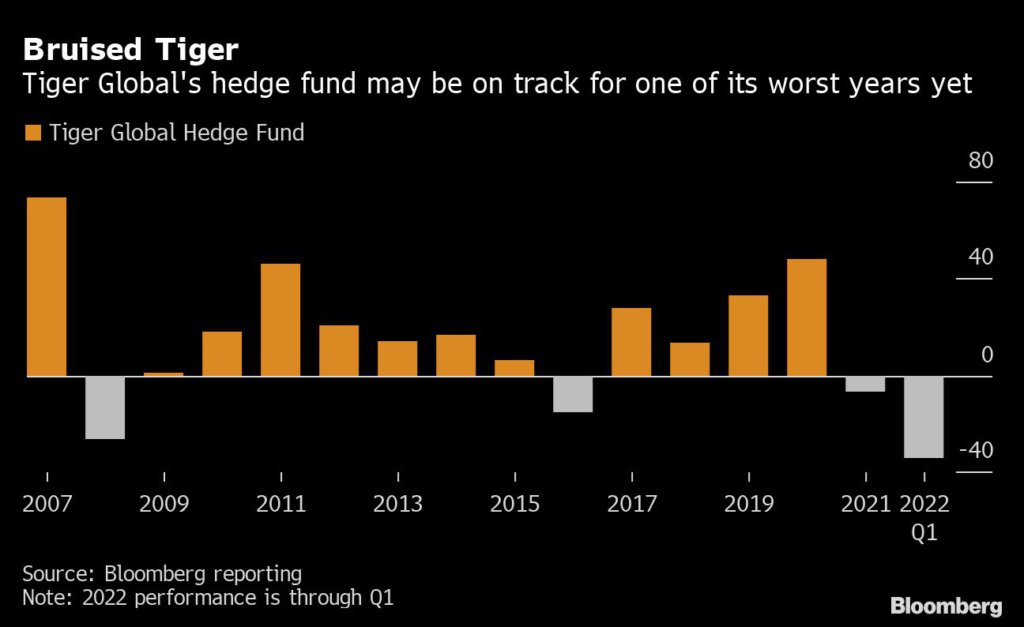

After a tough 2021, his Tiger Global Management has piled up losses this year that have set the industry abuzz — a staggering 34% slump for the firm’s hedge fund through March.

The speed of the reversal has shocked just about everyone, considering that Coleman is celebrated as one of his generation’s brightest stars, a standout among the elite money managers mentored by the famed Julian Robertson.

The bad run has been fueled by massive bets on stocks that have been hammered, market gyrations amid Russia’s invasion of Ukraine and a serious rough patch for the fast-growing tech companies in the U.S.

and China that for so long drove Tiger Global’s gains. On Friday, the poor performance prompted humility, something the $100 billion behemoth has rarely had to express over its two decades of nearly unblemished success.

“In this moment, we are humbled, but steady in our conviction and confident about the go-forward opportunity,” the firm’s investment team wrote in a letter sent to investors.

“We are reassessing and refining our models using all the inputs available to us.”

A Tiger Global spokeswoman declined to comment.

Built by Coleman and his partner Scott Shleifer, Tiger Global has long been seen as a throwback to the industry’s glory years, when double-digit returns were the norm and hotshot managers unerringly backed winning companies and shorted the losers.

Coleman, 46, showed that fees of 2-and-20 could still be a price worth paying: in 2020 alone, his flagship hedge fund jumped 48%.

The recent turn in Tiger Global’s fortunes have hurt more than Coleman’s professional pride.

Across the firm’s $35 billion in funds focused on public companies, this year’s losses have triggered a more than $10 billion hit to investors that include foundations, endowments and pension funds, as well as Tiger Global insiders.

And Coleman’s personal wealth has dropped by $1.3 billion, according to calculations by the Bloomberg Billionaires Index.

Coleman worked as a technology analyst at Robertson’s Tiger hedge fund for less than four years before he became an official Tiger Cub in 2001, the term for Robertson proteges who started their own firms.

Originally Tiger Technology, the new shop expanded to payments, education and other sectors and changed its name to Tiger Global.

In the early 2000s, Coleman and Shleifer added private investments to the mix, realizing before many of their peers that they might find higher returns outside of public markets.

The firm’s first serious bump was during the 2008 financial crisis, when it lost 26%, followed by a 1% gain the next year.

Coleman regrouped, vowing to return to his tech roots and avoid industries where politics or macro events could interfere.

That approach paid off spectacularly. Through 2020, Tiger Global’s annualized returns at its hedge fund were more than 20%, with just two years of losses.

Failing Bets

But now its biggest wagers are dragging the fund down.

While markets were already jittery this year due to high inflation and expectations of rate hikes, Russia’s war against Ukraine triggered a flight from risk.

The tech-heavy Nasdaq 100 and the Russell 2000 of small-caps each entered a bear-market decline of 20% in the first quarter, though losses were pared at the end of March.

Tiger Global’s particular undoing was sticking closely to tech companies, particularly from China, that had brought it so much success.

One example is JD.com Inc., which started out as a $200 million bet in 2009 and eventually produced a $5 billion net profit.

As of Dec. 31, it was the fund’s largest holding.

Battered by the markets, a regulatory crackdown in China and rising tensions between Beijing and Washington, JD.com slid 20% last year in New York trading and is down 16% in 2022.

“In hindsight, we should have sold more shares across our portfolio in 2021 than we did,” Tiger Global’s investment team said in Friday’s letter.

The fund isn’t alone in its struggles.

Fellow Tiger cub Philippe Laffont’s Coatue Management, another firm that’s had stellar performance on the back of its tech wagers, tumbled 10% in the first quarter. Some of its biggest equity holdings at year-end, Rivian Automotive Inc.and Moderna Inc., dropped 52% and 32%, respectively.

The MSCI World Information Technology Index, which rose 562% in the decade through 2021, fell 10% in the first three months of the year, according to data compiled by Bloomberg.

Private Questions

The damage for Tiger Global’s hedge fund extended to its private holdings.

Managers have “adjusted valuations down” for the fund’s private investments to account for pressure on their public-market peers, they said in the letter to clients.

The fund owns shares of private companies including ByteDance, Stripe, Checkout and Databricks.

It’s unclear what those mark downs mean for Tiger Global’s venture capital business, where assets were $65 billion at the end of last year.

Almost a quarter of Tiger’s private wagers as of August were in China, which has become a minefield for investors amid the regulatory crackdown.

President Xi Jinping tightened his grip on the nation’s tech sector, imposing new restrictions and imprisoning some executives to rein in what he sees as capitalism’s excesses.

While recent signals from the ruling Communist Party suggest the crackdown may be easing, the policy has shaken faith in even the biggest and most successful firms.

Also weighing on share prices has been an auditing dispute between China and the U.S.

that threatens to result in Chinese companies being booted off American exchanges. There was fresh optimism Saturday that such an outcome could be avoided after China signaled a willingness to grant U.S.

regulators full access to corporate audit reports.

In its letter, Tiger Global said it’s been “encouraged” by China’s recent support for stable capital markets and statements that the government is focused on the competitiveness of tech companies.

Still, the firm said it’s aware that risks remain and will be “data-seeking as the situation evolves.”

Led by Shleifer, Tiger’s Private Investment Partners funds — which take non-controlling stakes in startups — have returned 27% annually on average.

Last year, those funds gained 54% and returned $4 billion to investors, according to a person familiar with the matter. Even amid the tumultuous start to this year, investor appetite remains undimmed: in Friday’s letter, the firm said it had received net inflows every month this year in its public funds and recently closed its PIP 15 venture fund with $12.7 billion.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.