(Bloomberg) — Anyone betting the stocks they bought during the pandemic bull market would return enough to keep them ahead of inflation has reason to worry.

Not only are spiraling prices clogging up the economy and raising recession risk, they’re debasing the value of what’s left of an investor’s equity gains.

Since the pre-Covid peak in February 2020, the S&P 500 has appreciated 11% a year, well above the historic average. But inflation was 5.2% over the same stretch, eating almost half the equity increase.

It’s a brutal one-two punch that gets worse in a shorter lens, with this year’s 14% drop worsened when stacked next to surging consumer prices.

Adjusted for inflation, the S&P 500 is down in value at an annualized rate of roughly 40%, worse than any full year since 1974, data compiled by Bank of America Corp. show.

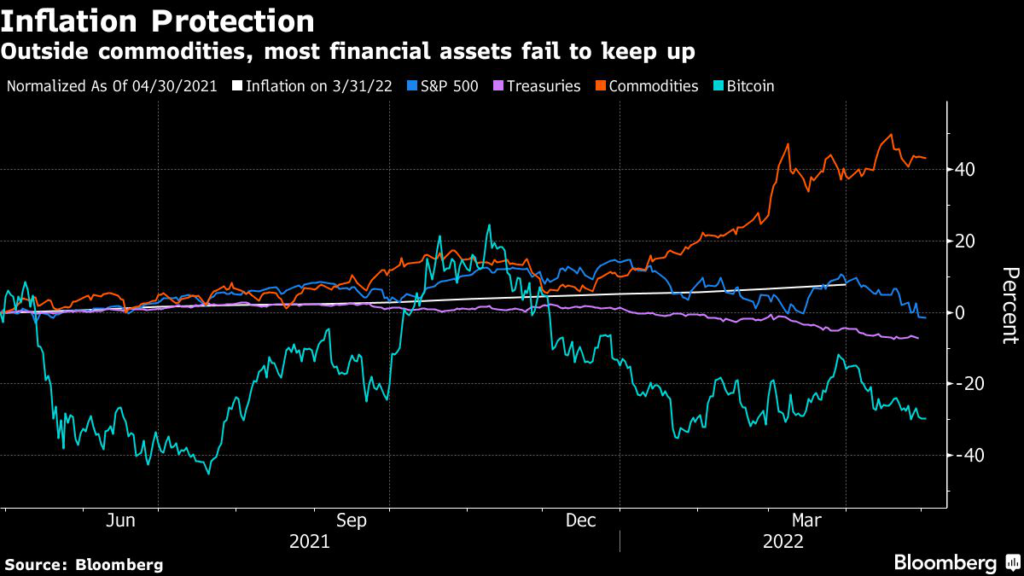

The data counter a popular narrative that stocks can serve as a haven during times of hot inflation.

They also show the danger of following any old playbook in the post-pandemic world where the Federal Reserve embarks on an aggressive rate-hiking cycle to curb growth.

With the exception of commodities, all major financial assets have lost money in real terms over the past year, including Bitcoin, something that crypto bulls once touted as a store of value.

“We are in the worst part of the market cycle now,” Dennis DeBusschere, the founder of 22V Research, wrote in a note Monday.

“Inflation/economic growth data are stubbornly firm, and markets are discounting significant tightening, but with still high uncertainty on how much MORE the Fed needs to do to slow growth/inflation.”

Since pricing pressure started to mount in April 2021, Bitcoin has lost roughly a third of its value as investors dumped risky assets in anticipation of tighter central bank policy.

Fixed income has endured deep losses too.

Investment-grade bonds are down 10% in the past year, followed by a 7% drop in Treasuries and a decline of 5% in high yield. Even those meant to work as an inflation hedge are losing money, with Vanguard Short-Term Inflation-Protected Securities Index Fund (VTIP) and iShares TIPS ETF (TIP) sliding 3% and 6.7%, respectively.

Read more: Bridgewater’s Top Strategist Says Fed Has to Ramp Up Rate Hikes

Betting on stocks as a harbor during the inflation storm hasn’t worked either.

The S&P 500’s 1% slide over the past year translates to a real loss of almost 10%, when the latest annualized inflation of 8.5% is factored in.

The real return is even worse for the tech-heavy Nasdaq 100 and the Russell 2000 of small-cap stocks, which are down roughly 15% and 25%, respectively.

“Anyone who tells you we are in a bull market has got a lot of explaining to do,” said Mike Wilson, chief U.S.

equity strategist at Morgan Stanley. “Perhaps, stocks are no longer the inflation hedge investors expect.”

That argument held that corporate America tends to benefit in a high-inflation environment in part because it can pass on rising costs to end consumers.

And that resilience in earnings can help stocks thrive.

Profit estimates for this year and next have gone up in the past 12 months. Yet with the Fed committing to raise rates to battle inflation running at a four-decade high, the specter of higher borrowing costs has sparked a quick reassessment of equity valuations and a broad selloff.

Commodities have rallied, with a Bloomberg measure tracking everything from oil to wheat climbing more than 40% over the past year.

Still, Societe Generale strategists led by Andrew Lapthorne warn investors not to lean too much on the asset, in part because of its “notoriously volatile” prices that can be affected by idiosyncratic factors, such as geopolitical events or seasonal variations.

“We want to be long inflation up until the point tightening creates the conditions whereby supply and demand are brought back into balance by an economic slowdown or, even worse, a recession,” Lapthorne wrote in a note last week.

“In that regard, commodity prices, bond yields and equities are all involved in a game of chicken with central bank tightening. If central banks are successful, these inflation hedges will become problematic.”

To mitigate the risk, the team created a multi-asset model to hedge inflation.

In commodities, rather than wagering on further gains, they developed a trend following strategy to ride the ebbs and flow of prices. Similarly in bonds, they’re long yield volatility, as opposed to placing an outright bet on a continued rise in rates.

In stocks, the model calls for better returns from inflation beneficiary versus the market.

“We are simply changing the implementation of what are traditional inflation hedges,” Lapthorne said.

“We like the logic of being long the problem (commodities), being long a reaction to that problem (rates volatility) and being long the beneficiaries of that problem (inflation-linked equities).”

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.