(Bloomberg) — Asian stocks and US equity futures edged up Wednesday in cautious trading dominated by a dimming economic outlook and an anxious wait for data that may show US inflation at a fresh four-decade high.

MSCI Inc.’s regional share gauge added about 0.5%, bolstered by a rebound in Chinese technology shares.

S&P 500 and Nasdaq 100 futures were in the green, but European contracts dipped.

Steadier Covid trends in Shanghai and the possibility of looser Hong Kong quarantine rules may have aided Asian sentiment.

Taiwan rallied after authorities made a rare pledge to prop up domestic shares.

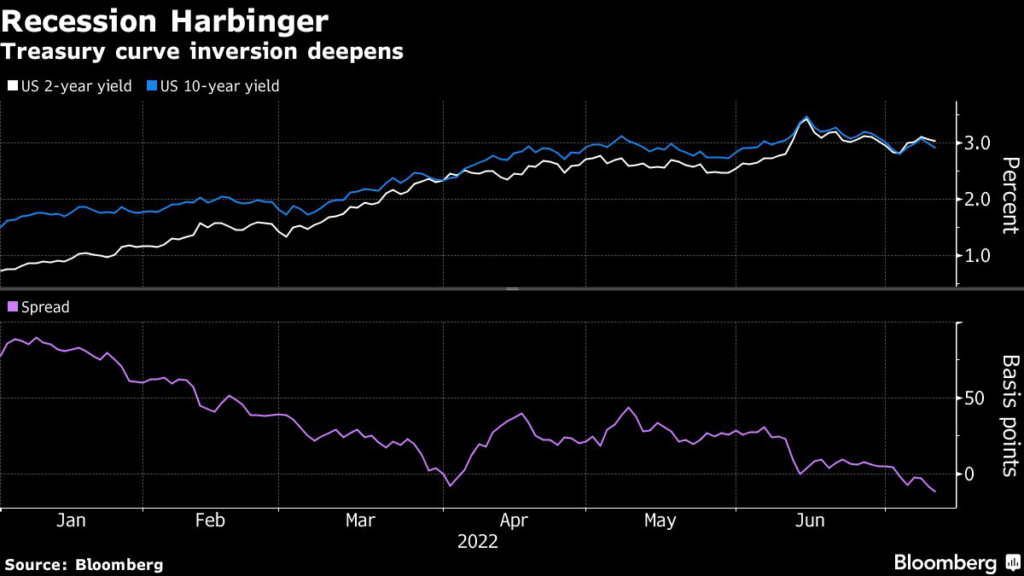

Treasuries were steady and a key part of the yield curve remains inverted, a potential signal of recession ahead.

The 10-year yield at one point Tuesday was 12.4 basis points below the 2-year rate, a level unseen since 2007.

Oil stabilized at about $96 a barrel after a tumble. The dollar hovered near the highest levels since March 2020.

The euro remained in sight of parity with the greenback. Bitcoin slipped toward $19,000.

Rapidly tightening monetary policy in the US and elsewhere to fight price pressures is fueling worries about growth and leaving markets nervous.

South Korea and New Zealand became the latest to hike interest rates further.

Economists project US inflation likely hit a pandemic peak in June that will keep the Federal Reserve geared for another big rate increase.

The consumer-price index probably rose 8.8% from a year earlier, the largest jump since 1981, according to a Bloomberg survey ahead of the release Wednesday.

“This is widely expected to be a really strong print,” Lauren Goodwin, economist and portfolio strategist at New York Life Investments, said on Bloomberg Television.

“Even if it is not, I don’t think that changes the Fed’s perspective in a couple of weeks. We won’t have enough evidence that inflation is convincingly turning over.”

The International Monetary Fund cut its growth projections for the US economy and warned that a broad-based surge in inflation poses “systemic risks” to both the country and the global economy.

Traders are also on tenterhooks for the latest corporate earnings and monitoring for a brewing energy crisis in Europe if Russia cuts off gas supplies in the fallout from its invasion of Ukraine.

What to watch this week:

- Earnings due from JPMorgan, Morgan Stanley, Citigroup, Wells Fargo

- US CPI data, Wednesday

- Federal Reserve Beige Book, Wednesday

- US PPI, jobless claims, Thursday

- China GDP, Friday

- US business inventories, industrial production, University of Michigan consumer sentiment, Empire manufacturing, retail sales, Friday

- G-20 finance ministers, central bankers meet in Bali, from Friday

- Atlanta Fed President Raphael Bostic speaks, Friday

Will the eurozone avoid a recession or a debt crisis?

How will the euro and stocks perform in the next six months? Share your views and participate in the latest MLIV Pulse survey. It only takes a minute, so please click here anonymously.

Some of the main moves in markets:

Stocks

- S&P 500 futures rose 0.2% of 12:52 p.m.

in Tokyo. The S&P 500 fell 0.9%

- Nasdaq 100 futures added 0.3%. The Nasdaq 100 fell 1%

- Japan’s Topix index rose 0.3%

- South Korea’s Kospi index rose 0.7%

- Australia’s S&P/ASX 200 Index was steady

- China’s Shanghai Composite index climbed 0.4%

- Hong Kong’s Hang Seng index added 0.8%

- Euro Stoxx 50 futures lost 0.3%

Currencies

- The Bloomberg Dollar Spot Index was steady

- The euro was at $1.0035

- The Japanese yen was at 137.15 per dollar, down 0.2%

- The offshore yuan was at 6.7343 per dollar

Bonds

- The yield on 10-year Treasuries rose one basis point to 2.98%

- Australia’s 10-year bond yield fell three basis points to 3.39%

Commodities

- West Texas Intermediate crude was at $95.90 a barrel

- Gold was at $1,727.12 an ounce

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.