(Bloomberg) — Chinese authorities held emergency meetings with banks after growing alarmed that an increasing number of homebuyers across the country are refusing to pay mortgages on stalled projects, according to people familiar with the matter.

The Ministry of Housing and Urban-Rural Development met with financial regulators and major Chinese banks this week to discuss the mortgage boycotts on concern that more buyers may follow suit, said the people, asking not to be identified discussing a private matter.

While there was no immediate solution, regulators asked local watchdogs and banks to report the impact, including property projects affected in their jurisdictions, as soon as possible, the people said.

Some banks plan to tighten their mortgage lending requirements in high-risk cities, two of the people said.

The housing ministry didn’t immediately reply to a fax requesting comment.

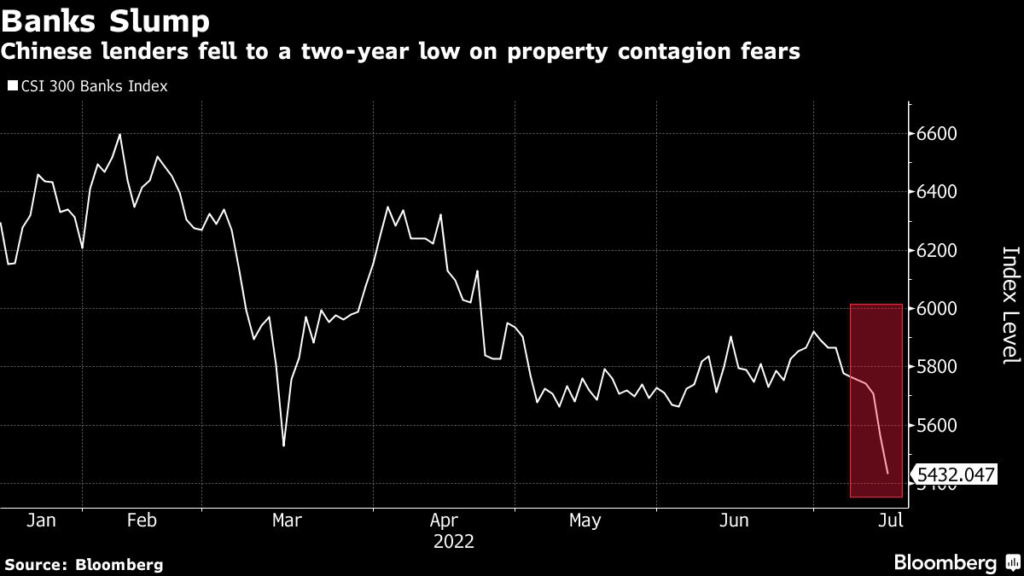

Reports of rapidly escalating refusals to pay mortgages in recent days have sparked losses in Chinese bank shares and developer bonds, reflecting concerns that the nation’s property crisis may spread to the financial system and trigger social unrest.

Chinese lenders already grappling with challenges from liquidity stress among developers now also have to brace for homebuyer defaults.

Homebuyers have stopped mortgage payments on at least 100 projects in more than 50 cities as of Wednesday, figures from researcher China Real Estate Information Corp.

show. That’s up from 58 projects on Tuesday and only 28 on Monday, according to Jefferies Financial Group Inc. analysts including Shujin Chen.

While it’s not clear how many homebuyers are snubbing repayments, the delayed projects make up about 1% of China’s total mortgage balance, according to Jefferies.

Should every buyer default, that would lead to a 388 billion yuan ($58 billion) increase in non-performing loans, Chen said.

Some major Chinese banks rushed to respond during trading hours on Thursday as the CSI 300 Banks Index fell as much as 3.3%.

State-owned Agricultural Bank of China Ltd. said it held 660 million yuan of overdue loans on unfinished homes, while smaller rival Industrial Bank Co. said 1.6 billion yuan of mortgages were impacted, of which 384 million yuan have become delinquent.

China Construction Bank Corp., the nation’s largest mortgage lender, said overall risks are controllable as its exposure to delayed projects is small.

Chinese policymakers face a dilemma in dealing with the problem, according to Chen at Jefferies.

On one hand, easing lending rules to favor homebuyers waiting for their properties to be completed may encourage more delinquencies. On the other, social stability remains the top priority for the government.

Avoiding a deeper property crisis that sends shockwaves across markets and banks is a political necessity ahead of this year’s Communist Party Congress.

Any move to tighten mortgage lending would put further pressure on already weak home sales as potential buyers balk at higher borrowing costs and longer loan approvals.

The outlook for sales — which some say recently bottomed — is also being dimmed by a resurgence in Covid cases and potential restrictions.

The crisis engulfing Chinese developers is reaching a new phase, with a debt selloff expanding to firms once deemed safe from the cash crunch, including Country Garden Holdings Co., the largest builder by sales.

China high-yield bonds were indicated slightly weaker Thursday as liquidity remained light, according to credit traders, though some Country Garden and CIFI Holdings Group Co.

dollar bonds gained. A Bloomberg Intelligence gauge of Chinese developer shares fell as much as 2.7%.

Nomura Holdings Inc. said the refusal to pay mortgages stems from the widespread practice in China of selling homes before they’re built.

Confidence that projects will be completed has weakened as developers’ cash woes intensified.

“We are especially concerned about the financial impact of the homebuyers’ ‘stopping mortgage repayments’ movement,” Nomura economists led by Ting Lu wrote in a note on Wednesday.

“China’s property downturn may finally adversely affect onshore financial institutions after hitting the offshore high-yield dollar bond market.”

Lu estimated that Chinese developers have only delivered around 60% of homes they presold between 2013 and 2020, while in those years China’s mortgage loans rose by 26.3 trillion yuan.

GF Securities Co. expected that up to 2 trillion yuan of mortgages could be impacted by the boycott.

Until recently, the nation’s 46 trillion yuan of outstanding mortgages have been considered as the safest banking assets because of high down payments and collateral value.

Their non-performing ratio has been steady at around 0.3% for years, the central bank said in April, compared with 1.69% for all loans.

(Updates with bank statements in the eighth paragraph)

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.