(Bloomberg) — Amid the carnage in emerging-market currencies this year, there’s been a surprisingly resilient outlier: the Mexican peso.

It’s held up as almost every peer succumbed to the dollar’s relentless push higher, an outperformance so stark that a few analysts have taken to calling it the “super peso.”

Some of the strength stems from fairly typical drivers — a tight fiscal policy and interest-rates increases that have lifted the carry trade.

But another key factor is expectations for a sea change in global trade in coming years that could bring a surge in foreign direct investment.

Mexico is luring factories from China as higher wages and a jump in transportation costs undermine what had been its competitive advantages.

A Covid-induced aversion to far-flung supply chains is also pushing companies to move operations from Asia to nearer the US — the world’s biggest market — a shift known as “nearshoring.” Adding to those logistics concerns are the strict shutdowns as part of China’s Covid Zero policy and concerns that China could make a move against Taiwan that would spur sanctions from Western countries.

It’s the beginning of a turnaround from two decades ago, when China joined the World Trade Organization and quickly displaced Mexico as the top manufacturing hub for US companies.

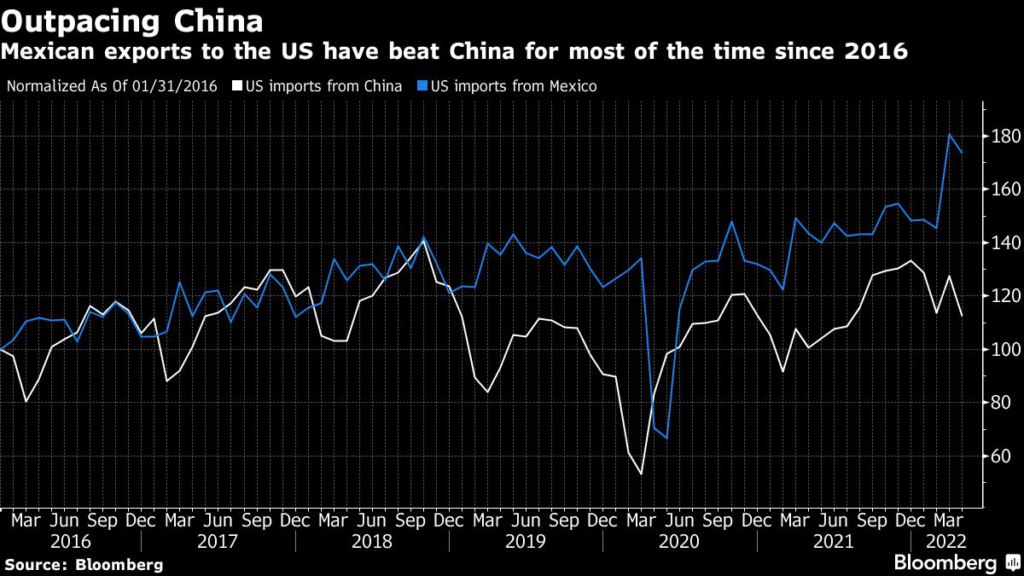

Now, Mexico’s exports to the US are narrowing the gap with China, and the currency market is being roiled, shocking investors who at the end of last year were forecasting the peso would be one of the world’s biggest losers in 2022.

“Mexico is beginning to reclaim the competitive advantages it lost decades ago,” said Hari Hariharan, the chief executive officer of New York-based hedge fund NWI Management.

“This is going to be a decade of an ascent of Mexico at the expense of China.”

The shift can also be seen in the Mexican peso’s performance against China’s yuan. Since the height of the pandemic selloff in March 2020, the peso has rallied about 15% versus its Chinese counterpart, one of the best performances among major currencies.

Nearshoring will accelerate this trend in the coming decade, according to Hariharan.

The boom can be seen across Mexico’s industrial north. From Tijuana on the West Coast to Matamoros at the southern tip of Texas, bulldozers and excavators are everywhere.

At least six suppliers for Tesla Inc. — Taiwanese companies EnFlex Corp. and Quanta Computer, French firm Faurecia SE, Germany’s ZF Friedrichshafen AG and APG Mexico — have set up in the state of Nuevo Leon since 2021.

Meanwhile, China’s Contemporary Amperex Technology Co., the world’s biggest maker of batteries for electric vehicles, is considering locations in Mexico for a plant to supply automakers, Bloomberg reported this month.

In a year during which the dollar has climbed to a record in its best annual run since 2015, the peso has gained less than 1% to about 20.4 per dollar, marking the second-best performance among major currencies behind Brazil’s real.

Still, some skeptics doubt the shift to Mexican production will be significant enough to form the basis for long-term gains for the currency.

The dollar value of Mexico’s exports to the US still trail China’s by a large margin, even as the gap grows ever narrower.

And there have been times in the past when analysts thought Mexico was poised for a breakout that didn’t come to fruition. Most notably, the predictions surfaced in 2007 and 2008 as surging oil prices raised transportation costs, then again when US President Donald Trump rattled trade relations with China during his tenure in office.

More recently, Mexican President Andres Manuel Lopez Obrador’s nationalist energy policies and skirmishes with companies have been seen as a deterrent to investment.

Last week, the US said Mexico’s energy policies violated North America’s free-trade deal, though there was little fallout in the peso market.

In the first quarter of this year, Mexico reported a record inflow of $19.4 billion in foreign direct investment, up 5.8% from the same period of last year after excluding one-off mergers.

Vacancy rates at industrial parks in Juarez, Reynosa and Monterrey hit record lows in the first quarter on nearshoring demand, Credit Suisse analysts said in a June report. During his trip to Washington this month, Lopez Obrador forecast US investment in the country would reach $40 billion between now and 2024.

Mexico’s exports to the US have been growing faster than its Asian rival’s for most of the time since 2016.

The Inter-American Development Bank in June 2022 estimated nearshoring could add up to $35.3 billion a year more in annual exports from Mexico.

Mexico exported $422 billion to the US in the past 12 months, $121 billion less than China.

That gap was almost $200 billion four years ago.

The transformation of supply chains will take time but the snarls caused by China’s zero-Covid policy will push companies to diversify operations on a “just-in-case basis,” said John Paul Lech, a portfolio manager at Matthews International Capital Management in San Francisco.

“Mexico is in a good position,” Lech said.

“Nearshoring could be a theme that impacts Mexico over longer durations of time.”

Peso Undervalued

The peso’s relatively cheap valuation is an additional lure for foreign investors.

On a trade-weighted basis, the currency has been on the weaker side of its 10- and 20-year averages since 2015, according to data compiled by Bank for International Settlements. China’s trade-weighted exchange rate, on the other hand, now hovers near seven-year highs.

“We see the issue of nearshoring as a medium- to long-term positive factor for the MXN,” HSBC FX strategists Joseph Incalcaterra and Clyde Wardle wrote in a July 14 note.

While US recession risks may weigh on the peso in the short term, resilient balance of payment flows should allow the currency to outperform regional peers, they wrote.

The bank sees the peso gaining about 6% to 19.25 per dollar by the end of next year, they wrote.

(Updates peso price in 10th paragraph)

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.