(Bloomberg) — US futures slipped as a rally that powered US stocks to their best month since 2020 turned fragile with central bankers driving home the message higher interest rates are needed to bring inflation under control, despite rising recession risks.

Contracts on both the Nasdaq 100 and S&P 500 traded lower on the heels of the best month for stocks since the year of the pandemic.

The Stoxx 600 Index rose 0.3%, led by banks, as HSBC Holdings Plc posted better-than-estimated profits.

The dollar fell against all of its Group of 10 peers ahead of data later Monday expected to show a slowdown in US manufacturing for July.

Oil declined after poor Chinese economic data added to concerns that a global slowdown may sap demand.

West Texas Intermediate dropped below $96 a barrel after sinking almost 7% in July in the first back-to-back monthly loss since late 2020.

Traders are speculating the Federal Reserve will tone down its anti-inflation campaign and opt for a slower path of rate hikes after data showed the US economy shrank a second quarter.

While that sentiment drove July’s market turnaround after historic first-half losses, over the weekend some Fed officials sought to reinforce the message that higher rates are needed to stamp out price pressures and downplayed recession risks.

“The fact that a very weak run of data is seen as equity bullish just purely on the basis of lower rates speaks to just how utterly dominant Fed policy has become in driving investor behavior,” said James Athey, investment director at abrdn.

“Unless the Fed pulls off a miracle I am afraid the bear market is absolutely not over.”

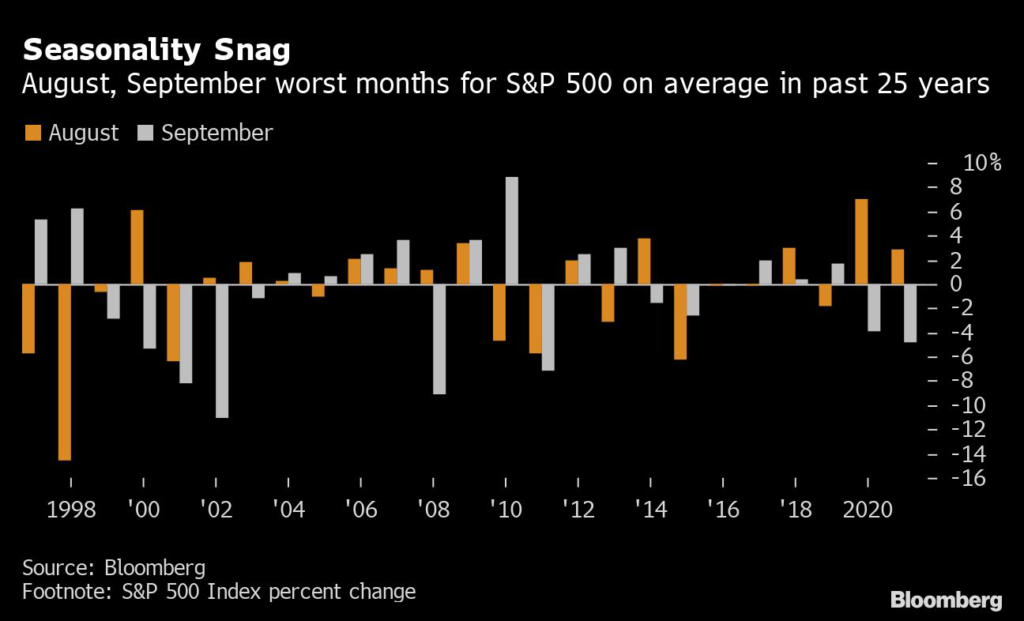

Despite a 12.6% advance from a low on June 16, the S&P 500 could be facing an ugly stretch. Wall Street lore says October is the most dangerous month for the stock market because of crashes in 1929, 1987 and 2008.

But August and September are actually worse, with the S&P 500 averaging declines of 0.6% and 0.7%, respectively, over the past 25 years.

Read more: Surging Stock Market Is Heading Into Riskiest Months of the Year

Treasury yields steadied with the 10-year rate at 2.65%, well down from June’s peak near 3.50%.

Italian bonds rallied, sending the 10-year yield below 3% for the first time since May, as investors bet that a new government will stick to commitments needed to unlock European Union funds.

Bitcoin declined after reaching the highest levels since mid-June on Saturday amid optimism that the market may have recovered from its worst levels.

Investors are also monitoring US House Speaker Nancy Pelosi’s trip to Asia.

A statement from her office skipped any mention of a possible stopover in Taiwan. A visit may stoke US-China tension over the island.

What to watch this week:

- Airbnb, Alibaba and BP are among earnings reports

- US construction spending, ISM manufacturing, Monday

- Reserve Bank of Australia rate decision, Tuesday

- US JOLTS job openings, Tuesday

- Chicago Fed President Charles Evans, St.

Louis Fed President James Bullard due to speak at separate events, Tuesday

- OPEC+ meeting on output, Wednesday

- US factory orders, durable goods, ISM services, Wednesday

- BOE rate decision, Thursday

- US initial jobless claims, trade, Thursday

- Cleveland Fed President Loretta Mester due to speak, Thursday

- US employment report for July, Friday

Some of the main moves in markets:

Stocks

- Futures on the S&P 500 fell 0.3% as of 8:15 a.m.

New York time

- Futures on the Nasdaq 100 fell 0.2%

- Futures on the Dow Jones Industrial Average fell 0.1%

- The Stoxx Europe 600 rose 0.3%

- The MSCI World index rose 0.3%

Currencies

- The Bloomberg Dollar Spot Index fell 0.3%

- The euro rose 0.1% to $1.0233

- The British pound rose 0.5% to $1.2227

- The Japanese yen rose 0.7% to 132.30 per dollar

Bonds

- The yield on 10-year Treasuries was little changed at 2.65%

- Germany’s 10-year yield was little changed at 0.82%

- Britain’s 10-year yield was little changed at 1.87%

Commodities

- West Texas Intermediate crude fell 3.2% to $95.43 a barrel

- Gold futures rose 0.4% to $1,789 an ounce

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.