The Swiss National Bank will almost certainly raise interest rates this week, but economists are split three ways on how aggressively officials will act to tame inflation that’s the lowest in the OECD.

(Bloomberg) — The Swiss National Bank will almost certainly raise interest rates this week, but economists are split three ways on how aggressively officials will act to tame inflation that’s the lowest in the OECD.

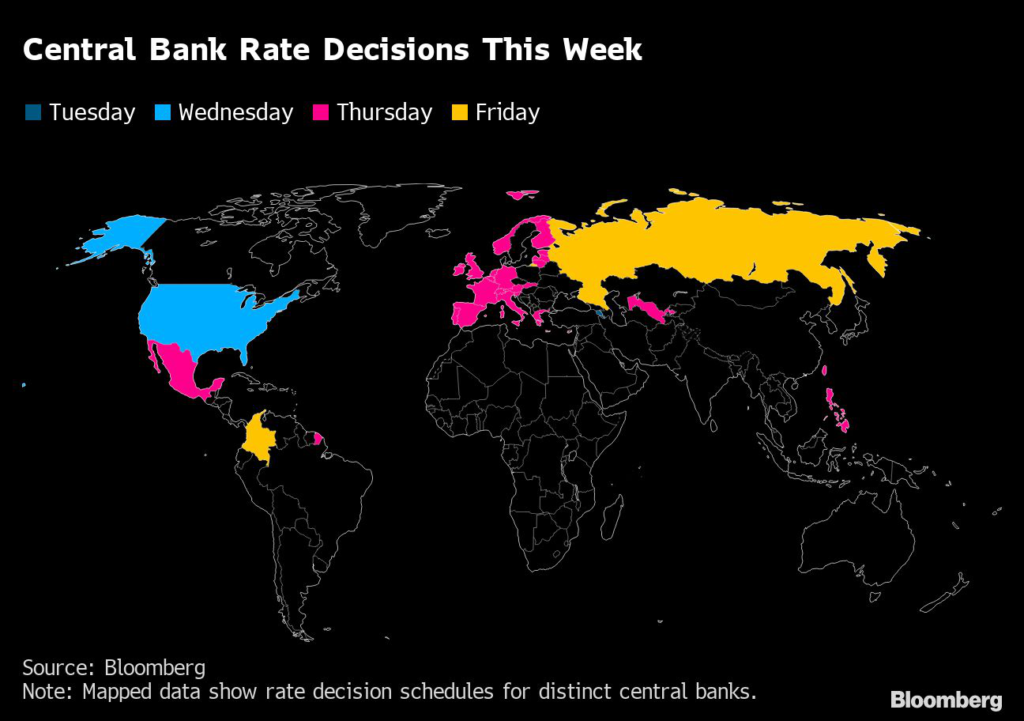

While a large majority of forecasters anticipates a half-point hike on Thursday to reach 1%, Bloomberg’s survey also shows predictions for a larger or smaller step by the central bank led by President Thomas Jordan.

Any move would be the third since the Swiss began raising rates half a year ago.

The divergence in estimates reflects limited signaling by the SNB, and a relatively benign inflation and growth backdrop, by global standards, that has left observers at odds on the required response.

“There are good reasons to do little, but also good reasons to do a lot,” said Alessandro Bee, an economist at UBS.

“The SNB will choose the middle path.”

Bee’s prediction of a half-point move is what economists also anticipate from the European Central Bank, the US Federal Reserve and the Bank of England.

Those three and the SNB will all take rate decisions within a 24-hour period this week.

While inflation at 3% doesn’t warrant an overreaction, the Swiss need to avoid too large a gap between their rate and those of others, and also need to show some aggression to currency traders, the UBS economist reckons.

“If the decision is too dovish, the markets could come to believe that the SNB is not prepared to take big steps and start speculating against the franc,” he said.

The Case for Less

The SNB will deliver only a quarter-point hike after having overestimated the strength of prices, according to Maxime Botteron, an economist at Credit Suisse.

In the survey of 27 forecasters, only he and one other see that smaller move transpiring.

“Inflation has fallen below SNB’s forecast in recent months,” he said. “We saw rising wages this year and continue to expect further raises.

But domestic and core inflation never went above 2% — the main drivers of price growth are still abroad.”

Botteron emphasizes that the 125 basis points in SNB hikes so far have already brought borrowing costs significantly higher in real terms than in the surrounding euro area.

Inflation in the region is more than three times as fast.

He reckons price growth will already return to the SNB’s ceiling of 2% by the second quarter of 2023. Meanwhile if pressures on the currency mounted, officials could still sell some of their huge FX reserves.

The Case for More

“The SNB must send a signal that inflation remains too high for comfort,” says Patrick Haefeli, an economist at St.

Galler Kantonalbank. “Particularly in view of the strong Swiss labor market, it’s important to prevent a wage-price spiral.”

He is among five forecasters predicting a second consecutive increase of 75 basis points.

Among other institutions doing so are Goldman Sachs and Citigroup.

With unemployment at only 2%, Haefeli’s worry is that Switzerland’s resilient labor market will prove fertile ground for pay pressures to take off.

“I believe that there is a risk of inflation expectations going up if the SNB does not take a 75 basis point step now,” he said.

Excess Liquidity

Aside from raising rates, the SNB could also revisit its move in September to impose so-called reverse tiering to drain excess liquidity built up during the years of negative monetary policy.

That decision meant that not all deposits are remunerated at the central bank rate, but only those up to a certain threshold.

Interest on exceeding reserves is discounted by 50 basis points, which currently means that they gain nothing at all.

While the discount will probably stay the same, the SNB is going to lower the threshold up to which deposits are paid for, according to Credit Suisse.

Balance Sheet

The large size of the central bank’s balance sheet, built up over years of interventions to defend the franc, could also feature at the decision.

In a Bloomberg survey, a majority of economists expect the hoard to reduce either this quarter or in the coming first quarter of 2023.

–With assistance from Harumi Ichikura.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.