Market participants are modestly bullish on stocks and bonds this year, the latest survey shows.

(Bloomberg) — After the biggest loss for 60/40 portfolios since the global financial crisis, better days may lie ahead for the trillion-dollar complex of balanced investment strategies.

Amid optimism that inflation has peaked, more than 60% of 610 respondents to the latest MLIV Pulse survey are betting stocks and bonds will move in opposite directions this year — re-establishing a time-honored relationship that has powered pension and endowment funds over the past two decades.

If they’re right, it would mark a big shift from the last year when equities and debt plunged in concert on runaway price growth. Big in-tandem market losses have sparked existential angst about the future of the investing style that drives 60% of assets into shares and 40% into bonds — while fueling a Wall Street hunt for alternative hedges.

Now survey participants are getting modestly bullish on bonds. The 10-year yield is seen dipping to 3.5% by the end of 2023, down from last year’s high of 4.24%.

Another big MLIV Pulse call: 2023 will see an uptick in moderate risk-taking with the S&P 500 eking out a gain of about 4%. The projections are in line with the similarly restrained prediction among market strategists as an economic downturn threatens to undercut corporate earnings in the months ahead.

“The next operation for the Fed, once they are done, is going to be cuts,” said John Madziyire, senior portfolio manager and head of US Treasuries at Vanguard Group Inc. “Before we actually get to it, bonds will front-run that. That means bonds do become a diversifier again.”

After being negatively correlated for much of the past twenty years, the relationship between stocks and bonds flipped decisively in 2022 as elevated inflation and subsequent interest-rate hikes hurt both asset classes, meaning bonds largely failed to hedge down days in equities.

Meanwhile, more than a third of respondents tout stocks as their preferred asset, with the median year-end target for the S&P 500 at 4,000, not too far off from the 4,075 forecast from strategists surveyed by Bloomberg. MLIV projections vary from as low as 2,000 to as high as 5,800, underscoring conflicted views on the investing outlook in the grip of an expected economic downturn on both sides of the Atlantic.

“We expect to turn more positive on risk assets at some point in 2023 – but we are not there yet,” the world’s largest asset manager BlackRock wrote in its investment outlook. “Equity valuations don’t yet reflect the damage ahead.”

The corporate earnings drop could be worst since the global financial crisis and may spark a new stock-market low, according to Morgan Stanley strategist Mike Wilson. Even one of Wall Streets biggest optimists, JPMorgan Chase & Co.’s Marko Kolanovic, sees the S&P 500 potentially retesting its bear-market October lows by the end of the first quarter.

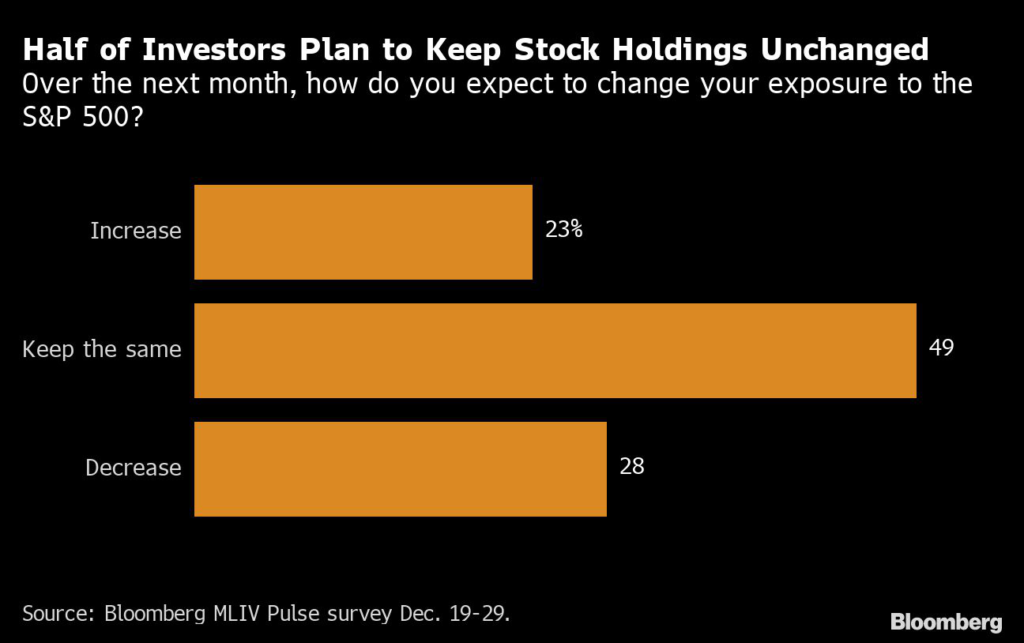

The muted outlook has most investors overall keeping their stock holdings largely unchanged for now. Professional money managers are more bearish in the short run, survey results show. Overall, some 23% of survey participants expect to increase their holdings over the next month compared to 28% who said they expect it to go down. Among retail investors, 26% expect to boost exposure and 15% plan to cut it.

The historic pattern of the past eight years showed that individual investors boosted their equity and exchange-traded fund purchases in January, particularly after reduced activity into year-end, according to data compiled by Vanda Research. Should the trend repeat, “retail traders will offer a strong tailwind to US stocks,” analysts wrote in a note.

Some 42% of survey respondents are in agreement with policy makers that interest rates will peak at a range of 5%-5.25%. Still, about 52% of individual traders are betting that the much longed-for Fed pivot will arrive sometime in 2023, while 54% of professional money managers expect it in 2024.

That’s setting up a fresh battle between the Fed and the market. Central bankers have indicated that rates need to remain in restrictive territory in the months ahead, warning Wall Street shouldn’t expect any rate reductions this year. Yet futures traders continue to bet that the first policy cut will land before 2023 is out.

“The market’s been way ahead of the Fed from the get-go,” Nancy Tengler, CEO and chief investment officer at Laffer Tengler Investments Inc said in a telephone interview. “The market is smarter than the Fed.”

About 27% of survey participants picked Elon Musk as the face of 2023 after he dominated headlines last year. More than a third of respondents chose to write in a name, rather then choose between suggested choices of Musk, Binance Holdings Ltd. Chief Executive Officer Changpeng ‘CZ’ Zhao and Russia’s President Vladimir Putin. Fed Chairman Jerome Powell, China’s Xi Jinping, Warren Buffett and Ukraine’s President Volodymyr Zelenskiy were the most popular written-in choices.

Some 47% of participants also saw lower bonuses at Wall Street banks in 2023.

For more markets analysis, see the MLIV Blog. To subscribe and see previous MLIV Pulse stories, click here.

–With assistance from Liz McCormick and Airielle Lowe.

(Adds a word cloud in third graph from the end.)

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.