A two-century-old bank in the New England countryside suddenly became one of the hottest stocks in US finance a couple of years ago after making an unlikely proclamation: It was willing to help cryptocurrency ventures.

(Bloomberg) — A two-century-old bank in the New England countryside suddenly became one of the hottest stocks in US finance a couple of years ago after making an unlikely proclamation: It was willing to help cryptocurrency ventures.

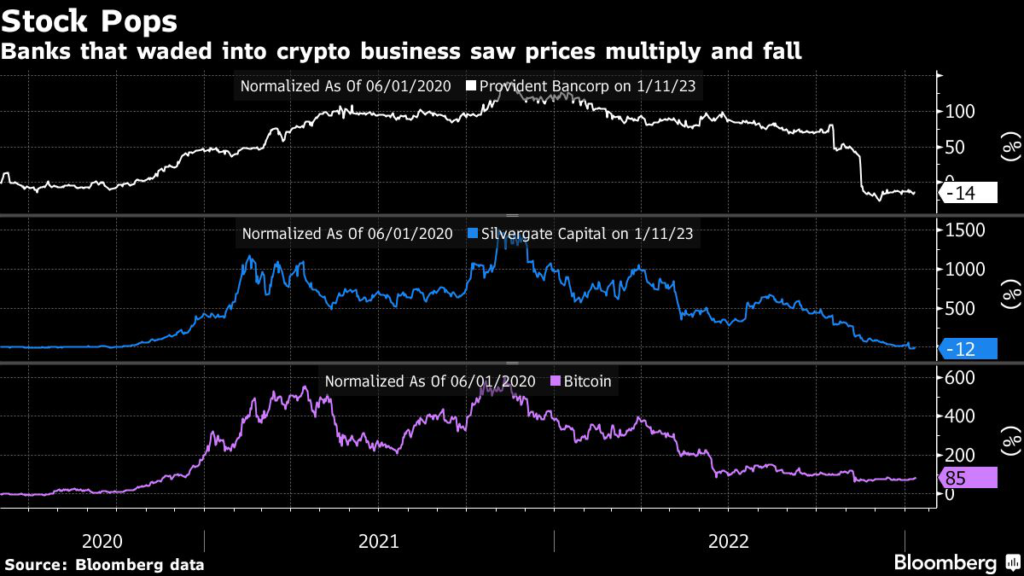

Provident Bancorp Inc., whose first chairman fought under George Washington in the Revolutionary War, watched its stock skyrocket 140% in just 14 months as Bitcoin hurtled toward a record high in November 2021.

But as crypto prices fell and took down the FTX exchange last year, Provident’s stock plunged, ultimately going lower than where it started.

The bank’s market value has declined by about two-thirds since the peak, erasing more than $230 million.

Call them minibubbles.

Across the US financial industry, a pattern is emerging of small lenders plowing into crypto and a variety of other hot niches, sending their stocks soaring and eventually crashing. It’s played out with online lending, commercial real estate and even taxi medallions over the past several years.

As the number of lenders getting stung kept climbing in recent years, some industry stalwarts grew flummoxed by the willingness of so many bankers to eschew longstanding tenets against taking concentrated risks from a single or unproven source.

“Areas that skyrocket all of a sudden are, almost by definition, going to come back to Earth, and have outsize risk and very little likelihood of consistent reward,” said Gene Ludwig, a comptroller of the currency under President Bill Clinton.

“Finance of any sort is a potential fire and that conflagration can get roaring pretty quick.”

Firms including Signature Bank and Customers Bancorp Inc. that once excited shareholders with forays into crypto-related business lines have instead been trying to assuage their concerns in recent months.

Then last week, a bank that flew even higher, Silvergate Capital Corp., chalked one of the most dramatic drops yet.

At one point, it lost almost half its market value in a matter of hours.

Silvergate had soaked up roughly $12 billion in deposits from crypto ventures, turning a profit by plowing the money into securities.

That stopped working during FTX’s downfall, when depositors rushed to pull their cash and weather the storm. To keep up with payouts, Silvergate sold off holdings at a loss and tapped wholesale funding, including $4.3 billion in short-term cash advances from the Federal Home Loan Bank as of the end of last month.

The firm’s market capitalization peaked at $5.9 billion in 2021, almost 20 times greater than at the start of 2020.

That was down to $386 million on Wednesday — a dramatic wipeout for shareholders in a bank where annual profits never breached $100 million.

Provident has said it remains well capitalized despite losses on loans to crypto miners.

Last month the Amesbury, Massachusetts-based lender named interim replacements for its chief executive officer. There was no response to messages seeking comment.

Silvergate has said it “still believes in the digital-asset industry,” and is committed to maintaining a “highly liquid balance sheet with a strong capital position.”

Watchdogs’ Warning

With cautionary tales piling up, regulators warned banks this month not to go too deep into digital currencies.

“It is important that risks related to the crypto-asset sector that cannot be mitigated or controlled do not migrate to the banking system,” the Federal Reserve, Federal Deposit Insurance Corp.

and the Office of the Comptroller of the Currency said in a joint statement, expressing concern about business models that are too concentrated in crypto-related activities.

But crypto is just the latest example of an age-old phenomenon where a handful of smaller firms become the go-to banks for some business fad.

For investors who get in early, the booms offer a rare chance to multiply their money betting on an industry that — when risk-taking is conservative — can draw derisive comparisons to utilities.

Such fortunes can fade quickly.

Signature and Customers both saw their stock prices multiply ahead of Bitcoin’s peak in 2021, only to give up much or all of the gains last year.

This month, Metropolitan Commercial Bank announced a retreat from crypto-related services that once boosted its revenue and deposits.

One upside, at least, is that smaller banks can experiment with emerging technologies or new strategies without damaging the broader financial system if something goes wrong, said Sydney Menefee, a partner at accounting firm Crowe who oversaw midsize and community bank supervision at the OCC.

“We need to avoid losses to depositors” and the FDIC’s backstop, she said in an interview.

“But the system is set up for the traditional shareholder to take the loss. They get the upside, but they also get the downside.”

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.