Turkey’s election this year threatens to reverse one of the best bond trades.

(Bloomberg) —

Turkey’s election this year threatens to reverse one of the best bond trades.

The country’s local bonds returned 25% last year — topping a Bloomberg gauge of developing market debt that lost 9% overall — thanks to a global rally in risk assets from mid-2022 and, crucially, regulations that pushed Turkish banks to buy lira-denominated debt.

The nation’s junk-rated sovereign dollar debt — over a third of which is held by foreign investors — also beat all other major peers, with a return of around 2%, and its corporate debt did well too.

But because there are presidential and parliamentary elections in the second quarter of this year — the political and economic outcome of which are unclear — investors aren’t willing to risk long-term exposure to Turkey’s bonds.

“Most of our peers, ourselves are included, are short Turkish exposure given the unorthodox monetary policy and the pressures that the Turkish economy is going through with balance of payments under strain,” said Yerlan Syzdykov, global head of emerging markets at Amundi, which has $2 trillion under management.

“Anything between now and June would be just a tactical opportunity unless you have a crystal ball.”

President Recep Tayyip Erdogan’s unconventional belief that lowering rates would ease inflationary pressures prompted the central bank to cut the main rate by 500 basis points last year.

It was a policy move that stood out among global peers, which raised their key rates aggressively to help cool the biggest rise in consumer prices in decades, and it diminished the appeal of lira assets, especially given that Turkey has had a current account deficit since late 2021.

The lira plummeted 29% last year, the most in emerging markets after the Argentine peso.

To help curb the currency’s drop, the central bank introduced a number of policies to support the local bond market, including some that discouraged banks from holding inflation-linked bonds as collateral for funding from the central bank and others that encouraged lenders to buy longer-term government bonds.

The currency is little changed in 2023.

“We need to see what kind of macroeconomic strategy will come out after elections and this is very, very unclear, said Pierre-Yves Bareau, global head of emerging market debt at JPMorgan Asset Management, who manages $40 billion in emerging-market debt.

“We need to see adjustments that will put the Turkish economy on a sustainable path.”

A recent survey by Metropoll showed approval for Erdogan at around 45%, suggesting he may struggle to win the more than 50% of the vote needed for a first-round victory and giving the opposition alliance hope of ending his roughly 20-year rule.

For now, investors see some stability, as Erdogan won’t risk market turmoil that could hurt his chances.

But increased government spending ahead of the vote and populist measures such as boosting minimum wages, housing for the poor and early retirement packages may come at a cost. The government sees the year-end budget deficit at 3.4% of Turkey’s $830 billion economy, higher than the five-year average of 2.3%.

The gap between yields on dollar bonds maturing in February 2025 and those due May 2047 has widened to as much as 212 basis points, with buyers opting for short-term debt instead of longer maturities.

The 2047 bonds are still trading at less than 70 cents on the dollar, according to data compiled by Bloomberg.

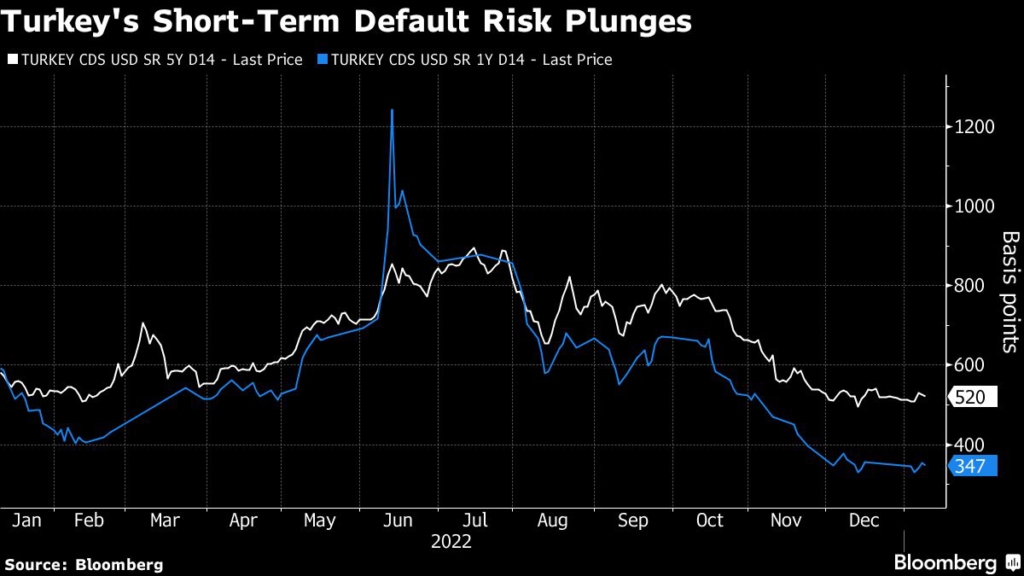

The reduced risk in the short term is also reflected in credit default swaps — an instrument showing the cost of insuring against default.

One-year Turkish CDS have fallen below their medium-term historical average, while five-year CDS are 100 basis points above their historic average. That level also suggests a cumulative probability of default of around 30% over the next five years, according to calculations by ICE Data Services.

“Selling short term protection and buying long term CDS makes sense,” said Jochen Felsenheimer, managing director at Munich-based XAIA Investment, who said he sees no risk of market turbulence before the vote.

“I do not like longer maturities due to the obvious risk of a traditional EM crisis.”

There’s also the general risk of holding on to Turkish assets, given that the currency has declined for 10 straight years through to the end of 2022.

Foreign investors’ holdings of local debt has fallen from $72 billion in 2013 to a record low of $1.2 billion this month, according to data from the central bank. International money managers account for about 35% of holders of Turkish sovereign debt, down from over 50% in January 2021.

And that’s despite the financial assistance Turkey got from Saudi Arabia and other Gulf states, combined with money transfers from Russia and a surge in tourist revenues, the combination of which sent foreign reserves to a peak of $86 billion in mid-December and kept the lira relatively stable in the second half of last year.

“When foreign ownership of Turkish assets is at historically low levels, even small flows help change the situation and make assets perform better,” said Amundi’s Syzdykov.

“The big question is how Turkey will address balance of payments situation and monetary policy going forward, will it have enough dollars as net reserves are extremely negative despite record tourism and export performance in 2022.”

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.