The Bank of Japan’s decision to keep its settings unchanged Wednesday gave global investors a modest jolt, leaving markets from the yen to Treasuries at risk from a potentially larger shock if officials opt to shift policy in the future.

(Bloomberg) — The Bank of Japan’s decision to keep its settings unchanged Wednesday gave global investors a modest jolt, leaving markets from the yen to Treasuries at risk from a potentially larger shock if officials opt to shift policy in the future.

Standing pat caught some traders by surprise, but it’s unlikely to douse speculation that the BOJ will normalize policy as inflation in Japan accelerates and Governor Haruhiko Kuroda nears the end of his term.

It suggests just a temporary setback to bets on a stronger yen and a bond selloff as analysts say it’s still a question of when — not if — the central bank exits its yield-curve control policy.

Indeed, while Japan’s currency at one stage slumped more than 2% against the dollar in the wake of the decision, it clawed back some ground as the session proceeded, helped by a swath of US economic data that dented the greenback.

Japanese government bonds surged as traders covered short positions and stocks pushed higher. US Treasury yields declined.

“We see it as a pause on the road to further policy normalization,” Mayank Mishra, a strategist at Standard Chartered Plc, said referring to the BOJ decision.

“We remain bullish on the yen, expecting yield differentials to continue to turn more supportive of the currency on further BOJ policy normalization and slowing global growth/inflation.”

The dollar-yen rate climbed as much as 2.7% to 131.58 Wednesday, but then proceeded to drop as low as 127.57, down 0.4% on the day.

“The dollar has actually peaked,” Henry McVey, head of global macro balance sheet and risk at Kohlberg Kravis Roberts & Co., told Bloomberg Television on Wednesday.

“The yen got hit very hard and then ultimately rallied back. The US is starting to slow down and the Fed will not get to 6% on short rates. The yen will continue to rally because ultimately we’re leaving deflation in Japan.”

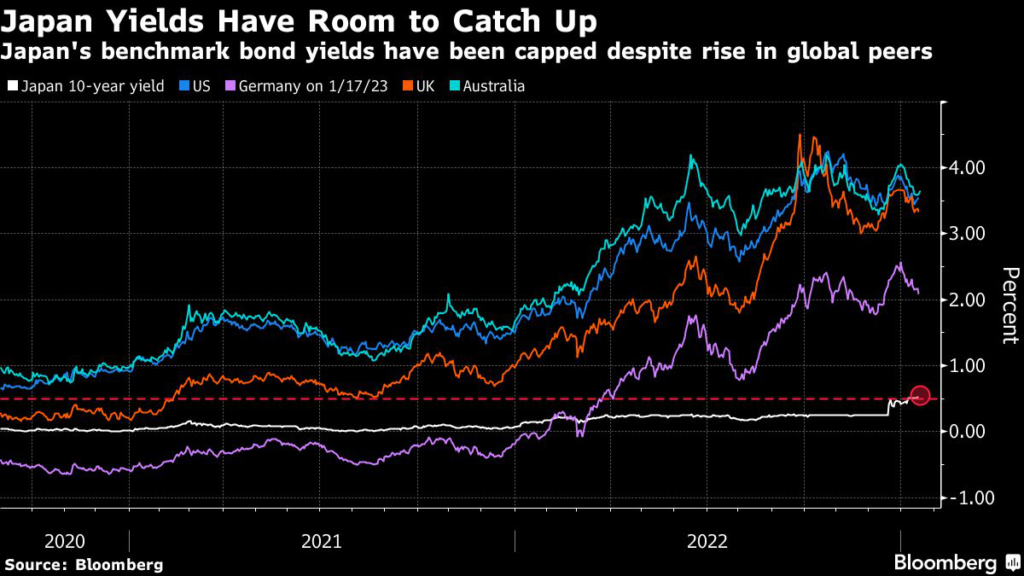

Bonds in other global markets were seen as most at risk from any policy shift that pushes Japanese yields higher, which may trigger a wave of money flowing back to the nation out of substantial overseas holdings.

Japanese investors are the largest foreign owners of Treasuries and strategists have said bonds in Australia and France are also vulnerable.

Last year’s rise in local yields helped fuel a record sale of ¥21.7 trillion ($168 billion) of foreign bonds in 2022, according to preliminary data from the Ministry of Finance going back to 2005.

“The big fear was the mass dislocation that could have unfolded if Japanese investors exited US, euro zone and Australian bond markets en-masse thanks to tastier local yields,” said Richard Franulovich, head of currency strategy at Westpac Banking Corp.

“This news today keeps the BOJ positioned as a anchor for global yields.”

The BOJ kept its main policy settings unchanged Wednesday, leaving its negative interest rate at -0.1%, while maintaining a trading band of 50 basis points around 0% for 10-year bonds.

There had been some expectation that it would raise the cap or drop the yield curve control.

Kuroda said he didn’t see the need to widen the yield range further, speaking later at the press conference following the statement.

BOJ Pushes Back on Speculation, Prompting Slide in Yen, Yields

“The market was looking for something that wasn’t there in terms of a policy shift from the Bank of Japan,” said Kerry Craig, a global market strategist at JPMorgan Asset Management in Melbourne.

“It was relatively clear that they were going to focus on attaining their ability to direct markets, rather than letting the market dictate to them what was going to happen.”

Its stance potentially opens up the path for short-term yen weakness with some analysts saying it could fall to around 135 per dollar.

But Others highlighted the unsustainability of the BOJ’s bond purchases as a path to renewed yen strength.

“We don’t think this changes anything as BOJ will be forced to continue to defend YCC by buying more JGBs,” Amir Anvarzadeh, strategist at Asymmetric Advisors Pte.

wrote in a note. “Sooner or later they need to tweak YCC again whether under Kuroda’s reign or the next governor, but the volume of their JGB purchases remain unsustainable and the yen will strengthen again toward the 120 level.”

The central bank said it would continue large-scale bond buying and increase purchases on a flexible basis if needed.

It also enhanced a provision for loans to commercial banks in a bid to encourage them to buy more debt — another tactic in its stubborn defense of policy.

The loan program was a “positive surprise for the market” and why Treasuries and Australian government debt climbed, said Hidehiro Joke, a senior bond strategist at Mizuho Securities Co.

in Tokyo. “Some market participants expected this kind of tweak to control the yield curve, including swaps, but I think up to 10 years is a large extension.”

Shift Timing

Further out, economists are positioning for a change, with a number bringing forward their expected timing for a shift, according to this month’s Bloomberg survey.

Some now predict an adjustment in April, the first meeting scheduled under a new governorship, while others expect a pivot in June.

Wednesday’s decision “means there are higher chances that the BOJ will pass the current policy framework to the next leadership rather than changing it under Kuroda,” said Hideo Kumano, executive economist at Dai-Ichi Life Research Institute.

–With assistance from Ruth Carson, Marcus Wong, David Finnerty, Yoshiaki Nohara, Naomi Tajitsu, Aline Oyamada, John McCorry, Alix Steel and Guy Johnson.

(Updates prices throughout.)

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.