Russia’s biggest companies, even those that haven’t been directly targeted by recent sanctions, are bypassing Wall Street to repay their outstanding debt after the crackdown broadly disrupted the financial plumbing needed to service bonds.

(Bloomberg) — Russia’s biggest companies, even those that haven’t been directly targeted by recent sanctions, are bypassing Wall Street to repay their outstanding debt after the crackdown broadly disrupted the financial plumbing needed to service bonds.

Oil giant Lukoil PJSC — via its special purpose vehicle Lukoil Securities Limited — went through brokers in Cyprus to buy back all of its outstanding eurobonds, according to several people familiar with the matter who asked not to be identified discussing confidential information.

Others, including Uralkali PJSC, MMC Norilsk Nickel PJSC and Metalloinvest Holding Co.

have asked bondholders for permission to change bond documentation so they can make direct payments to investors in rubles instead of the currency the debt was issued in, public filings show. Gazprom PJSC and Magnitogorsk Iron & Steel Works PJSC have substituted some of their eurobonds for ruble debt.

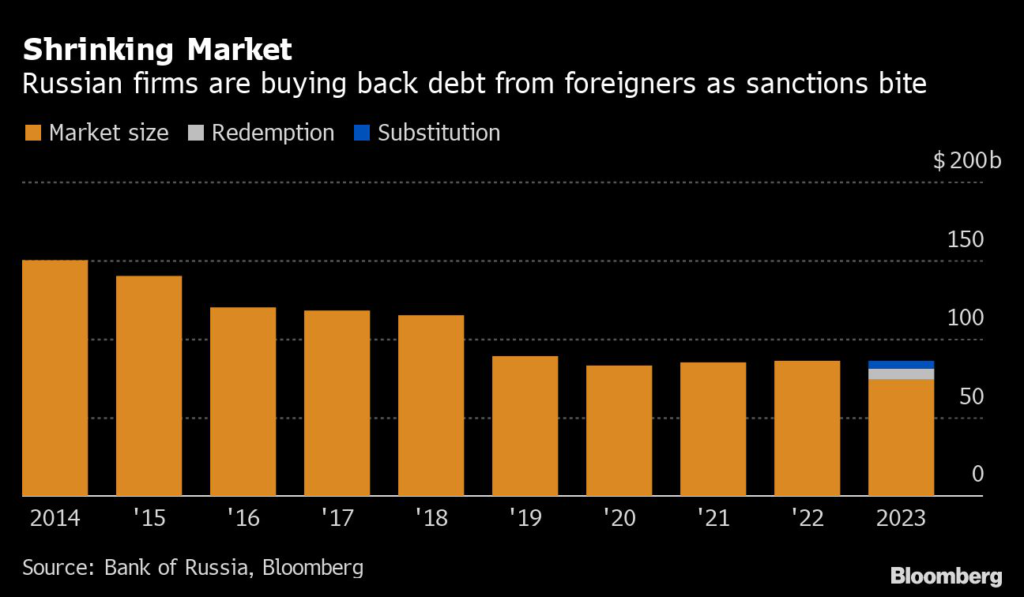

Worth $85.6 billion before the invasion of Ukraine, Russia’s international corporate bond market has shrunk by about $12.7 billion since President Vladimir Putin’s invasion of Ukraine prompted the US, UK and European Union to block Russia’s access to foreign capital, Bloomberg calculations based on central bank data show.

And it’s set to contract further this year after Gazprom makes more planned swaps.

Even in cases where the borrower doesn’t fall under sanctions, companies and their investors have found that the restrictions target so many of the processes needed for the bonds to keep functioning, that it’s become necessary to take them out of the market.

“In a couple of months everything is going to be bought out” by local investors, said Dmitry Dorofeev, a portfolio manager at Armbrok investment company in Yerevan, Armenia, which has traded some Russian eurobonds in recent months.

“Russian companies will replace bonds and return to Russia.”

While coupon and principal payments do go through, the process has become complicated and there are significant delays. Companies need to get paperwork sorted in Russia to repay foreign bondholders, and the financial plumbing used to get payments through hasn’t run smoothly since sanctions were imposed.

And Euroclear Bank SA and Clearstream Banking SA, Europe’s two major central depositories, only process transactions that have been vetted and processed by paying agents, according to people familiar with the matter who asked not to be named discussing private information.

Some firms have opted for other alternatives, including swaps, buybacks and direct payments to bondholders, although that last option is only for accounts in Russia.

The hurdle, however, is that Euroclear and Clearstream have been unwilling to process corporate actions, such as buybacks, since sanctions were introduced, the people said. Spokespeople for the two depositories declined to comment on the matter.

Read More: JPMorgan, BofA Among Banks to Resume Trading Russian Bonds

And so companies have been finding ways to exclude Euroclear and Clearstream, a process that could leave them exposed to ownership disputes, according to Alexander Geda, counsel at Moscow-based law firm Rybalkin, Gortsunyan, Dyakin and Partners, who advised Magnitogorsk Iron & Steel Works on its consent solicitation.

Lukoil, for instance, announced its buyback offer in a press release without publicly disclosing the terms.

Investors who expressed interest were contacted by brokers based in Cyprus, who would then buy their debt in over-the-counter transactions, according to several people with knowledge of the matter. Lukoil didn’t respond to phone calls and emailed questions.

Spokespeople for the European Commission, the US Treasury’s Office of Foreign Assets Control and the UK’s Office of Financial Sanctions Implementation declined to comment on whether buybacks of Russian corporate bonds in general — and in Lukoil’s case in particular — are in breach of their sanctions.

The Russian oil giant is not subject to sanctions imposed by the US, the EU or the UK following Russia’s invasion of Ukraine. Still, central depositories haven’t been processing corporate actions by Russian companies.

Read More: Aurelius, Silver Point Win Sweetener in Lukoil Bond Buyback Deal

Gazprom Plans

Gazprom plans to convert all domestic holdings of its eurobonds into equivalent domestic replacement bonds settled in rubles, Chief Financial Officer Famil Sadygov said by phone.

Holdings of 10 of the bonds have already been replaced and another 12 will be swapped by the end of March, he said. Four of those are due to be swapped this week.

Replacement bonds are “the most reliable way” to service debt given the restrictions on financial infrastructure, Sadygov said.

Eurobonds received in the exchange are canceled and the overall number in circulation is reduced accordingly, he said, adding that once the exchange is done, Gazprom pays coupons on both the substitute Russian bonds and the remaining international bonds.

Meanwhile some companies are pivoting east, with United Co.

Rusal International PJSC and others borrowing 52.7 billion yuan ($7.7 billion) of debt denominated in the Chinese offshore currency in recent months. But that debt still only makes up an “insignificant” 2.9% of the total Russian corporate debt market, according to a review of financial market risks published by the Bank of Russia on Jan.

19.

The ruble’s 11% rally over the past 12 months on the back of capital restrictions and high energy prices has helped create attractive conditions for buybacks, according to Alexey Kuprianov, director at Russian investment bank Aspring Capital, who advised Moscow’s Domodedovo airport on its consent solicitation and social network VK on its restructuring.

Those trends may change, he said.

“We may see a deterioration of the currency and the Russian economy, so it’s likely companies have less capability to buy back bonds,” Kuprianov said.

–With assistance from Tasos Vossos.

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.