The UK government sank deeper into debt in December as rising debt-interest payments and the cost of insulating consumers and businesses from the energy-price shock strained the public finances.

(Bloomberg) — The UK government sank deeper into debt in December as rising debt-interest payments and the cost of insulating consumers and businesses from the energy-price shock strained the public finances.

The budget deficit stood at £27.4 billion ($34 billion), a record for the month and almost triple the £10.7 billion shortfall a year earlier, the Office for National Statistics said Tuesday. Economists had forecast a reading of £17.3 billion.

The figures underscore risks to the UK economy as Prime Minister Rishi Sunak struggles to contain inflation near a four-decade high and strikes crippling the public services. A recession likely this year is expected to further dry up tax revenue and expand the deficit.

“Today’s worse-than-expected public finances figures will only embolden the Chancellor in the budget on 15th March to keep a tight grip on the public finances,” Ruth Gregory at Capital Economics wrote in a note to clients. It means he’ll “waits until closer to the next general election, perhaps in 2024, before announcing any significant tax cuts.”

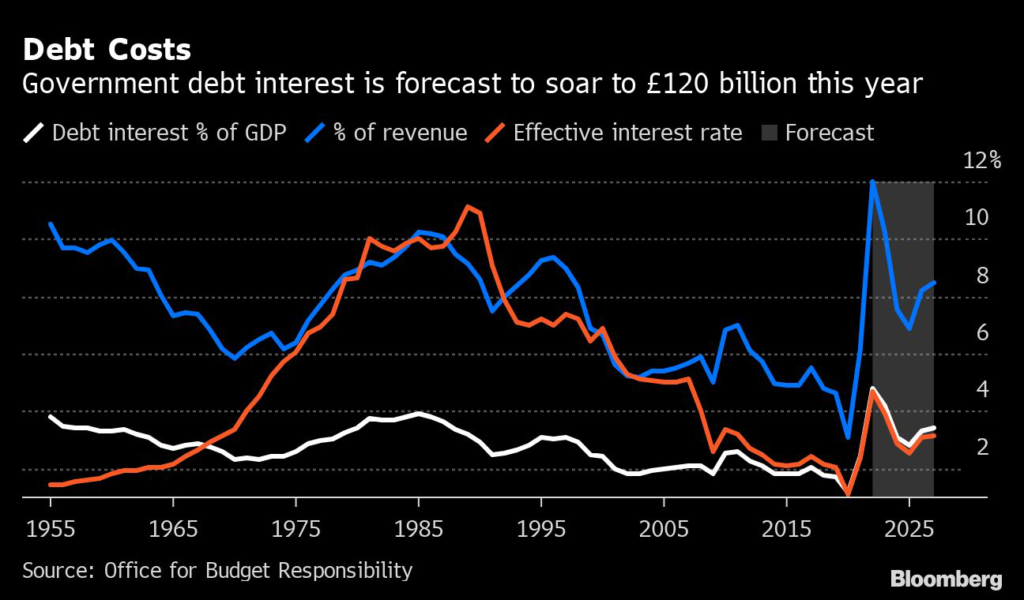

The massive cost of helping Britain through the living-standards crisis has dashed hopes that borrowing was on a downward path. Less than a year ago, the deficit was projected by the Office for Budget Responsibility to fall below £100 billion in 2022-23.

Now the cost of energy subsidies and other support, along with soaring interest rates means the Treasury has little leeway to spend on creaking public services or on placating workers who are striking because their pay is falling behind inflation.

Read more: Britain’s Health Care Black Hole Is Devouring the Entire Country

The deficit in the first nine months of the year was £128.1 billion — up £5 billion from a year earlier — and officials expect tens of billions to be added in the final three months of 2022-23.

Double-digit increases in receipts from VAT and income tax helped to partially offset a £33.4 billion surge in debt interest costs in the first nine months of the year. The tax take is being bolstered by high inflation and a strong labor market as total receipts leaped 11% to £658 billion in the financial year to December.

Public sector debt was £2.2 trillion, or around 88% of gross domestic product. The deficit was driven by £17.3 billion pounds of debt interest costs, the second-highest monthly figure on record.

About a quarter of all UK government bonds are linked to the retail price index of inflation, which has surged to its highest level in decades. Almost £14 billion of those payments went directly to index-linked debt.

Inflation affects debt costs with a two-month lag, meaning December bore the brunt of a surge in the RPI in October to a peak of 14.2%.

The cost of subsidizing gas and electricity is also taking a toll, amounting to £7 billion in December alone.

Of that, £1.9 billion was a direct cost-of-living transfer to households and £5 billion was the money spent on an energy price-cap for households and businesses. The OBR expects the latter to cost more than £40 billion by the end of the fiscal year.

“We are helping millions of families with the cost of living, but we must also ensure that our level of debt is fair for future generations,” Chancellor of the Exchequer Jeremy Hunt said in a statement. “We have already taken some tough decisions to get debt falling, and it is vital that we stick to this plan.”

The ONS said that the Bank of England’s gilt portfolio, bought under quantitative easing, was carrying a mark-to-market loss of £107 billion in December. The £833 billion portfolio has been a drain on the public finances since September due to higher interest rates. Last month alone it cost the taxpayer £1 billion.

Measures Hunt announced in October to calm a panic in gilt markets will ease the strain on the public purse in the months ahead. Those led to a drop of interest rates in financial markets and a decline in expectations for how high the Bank of England will lift its key rate.

“The lower path for Bank Rate and the recent fall in gilt yields suggests that debt interest payments in 2023/24 will be about £10 billion lower than the OBR forecast in November,” said Samuel Tombs, chief UK economist at Pantheon Macroeconomics.

The overshoot in the deficit relative to forecasts last month — the OBR was predicting £17.6 billion — was largely due to assumptions the fiscal watchdog made about student loans. The ONS said it will record the full impact of the changes to student-loan arrangements when more definite estimates become available.

–With assistance from Andrew Atkinson and Joel Rinneby.

(Updates with details on tax take and comment from the fourth paragraph.)

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.