China ramped up its support for a nascent economic recovery, seeking to nip a squeeze in bank borrowing costs in the bud by injecting a record amount of cash to its financial system.

(Bloomberg) — China ramped up its support for a nascent economic recovery, seeking to nip a squeeze in bank borrowing costs in the bud by injecting a record amount of cash to its financial system.

The People’s Bank of China offered the short-term cash boost to lenders on Friday, having just pumped one-year money into the system earlier this week.

The operations came after a gauge of interbank funding costs soared to the highest in two years last week and stayed elevated since.

Supporting growth became China’s top priority after policymakers abruptly dismantled Covid restrictions late last year, as sporadic lockdowns and a property slump sank the economy.

But as the end to Covid-Zero lifts consumption and demand for loans, it’s also creating a liquidity shortage that could hinder a sustained recovery.

That’s putting the PBOC in a bind. While it has to ease policy to replenish cash in the banking system, it cannot do it in an aggressive manner that places China too far apart from hawkish global peers.

A major policy divergence could weaken the yuan and reignite foreign capital outflows — which were the worst ever in the bond market last year.

“The move is a reflection of the PBOC’s unswerving stance to keep liquidity ample,” said Chen Kang, an analyst at Northeast Securities.

“Funding in the money market turned tighter yesterday, and we see the net injection as a immediate and efficient response.”

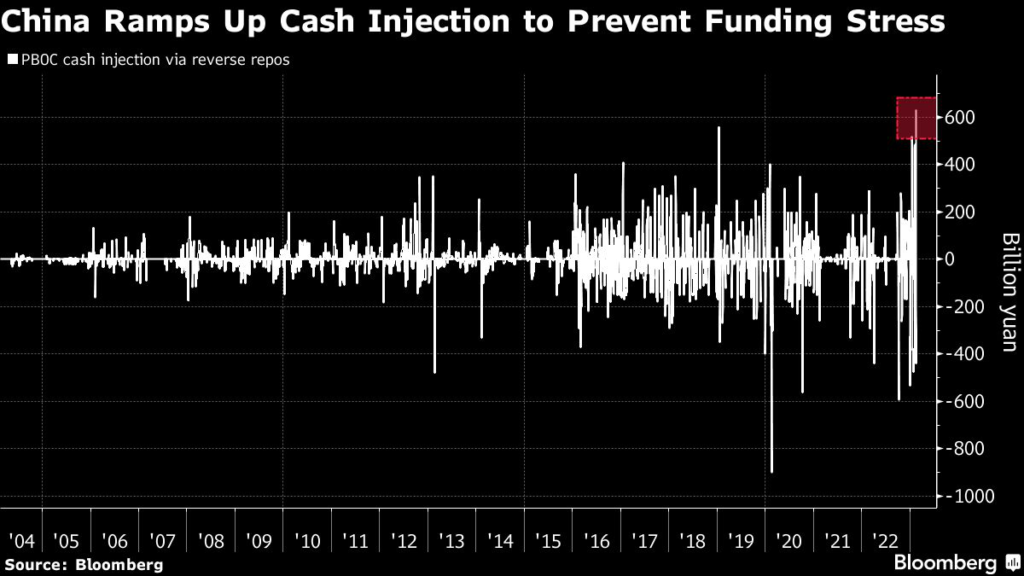

The PBOC offered 835 billion yuan ($121 billion) of cash via seven-day reverse repurchase contracts on Friday, resulting in an injection of 632 billion yuan on a net basis.

That’s the largest one-day addition on record in data going back to 2004.

Liquidity conditions have tightened of late amid a recovery in loan demand and economic activity. Chinese banks made 4.9 trillion yuan of new loans in January, the highest on record, according to official data last week.

Making the situation more complicated, there is a record maturity wall of interbank debt known as non-negotiable certificates of deposit looming, which needs to be refinanced.

Some 5.9 trillion yuan of the notes are due by the end of March, an all-time high on a quarterly basis, according to data compiled by Bloomberg.

Despite Friday’s cash infusion, the overnight repo rate — an indicator of interbank funding costs — rose for a fourth straight day to 2.1%.

Stock benchmarks in China and Hong Kong were lower in early trading, but fared better than the decline in the regional equities gauge.

The onshore yuan fell 0.3%, while 10-year government bond yields were little changed.

This week the PBOC injected 199 billion yuan of one-year funding via its medium-term lending facility, though it refrained from slashing the interest rate on the policy tool.

But a more aggressive easing move — such as cutting the reserve ratio or policy rate — cannot be ruled out in the coming months, analysts said.

China’s property sector is still struggling and exports have weakened, while the strength of the consumption rebound is uncertain.

“If the PBOC refrains from applying more permanent liquidity tools such as cutting the required reserve ratio, it may have to engage in frequent open market operations of large amounts going forward,” said Yang Yewei, analyst at Guosheng Securities.

The central bank has vowed to implement “targeted and forceful” monetary policy this year, with a focus on boosting domestic demand.

“Today’s liquidity injection reflects that the PBOC is supportive of liquidity in view of market demand,” said Frances Cheung, a rates strategist at Oversea-Chinese Banking Corp.

in Singapore. “Liquidity demand may stay on the high side in the coming weeks on heavy NCD maturities, potentially additional inflows in yuan assets and recovery in loan demand.”

–With assistance from Chester Yung and Shikhar Balwani.

(Updates Throughout.)

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.