Canada’s economy was supposed to be stalling by now. It’s still charging ahead, creating a challenge for the central bank as it prepares to hold its policy rate at 4.5% for a second straight decision.

(Bloomberg) — Canada’s economy was supposed to be stalling by now.

It’s still charging ahead, creating a challenge for the central bank as it prepares to hold its policy rate at 4.5% for a second straight decision.

Bank of Canada officials have said they’re confident higher borrowing costs are working to slow demand.

Economic data, though, keep surprising to the upside. The jobs market is running hot, and there are abundant vacancies. Wage pressures remain strong. Home prices, after a yearlong slump, may have found a bottom.

In January, when policymakers led by Governor Tiff Macklem first declared their intention to pause rate hikes, they forecast the economy would grow at just a 0.5% annualized pace in the first quarter.

Early indicators show growth coming in around 2.8%, defying predictions of a stall and potential recession.

The resilience has thrown into doubt the view that Canada is more sensitive to higher rates than its peers due to its highly indebted households and richly-valued housing market.

And that means the bank may state again that it’s still worried about inflation and is prepared to resume lifting rates if necessary.

“Macklem is in a tough spot, and must navigate global banking stress while acknowledging sticky price pressures and a hotter-than-expected domestic economy,” Dominique Lapointe, director of macro strategy at Manulife Investment Management, said by email.

“The Bank of Canada will hold again, but recent data will keep them hawkish.”

Citigroup Inc. economist Veronica Clark agrees the bank will stay biased toward tightening; she’s even not ruling out a surprise increase in Wednesday’s decision, due at 10 a.m.

in Ottawa.

A hike would shock the markets, and is unlikely. There are a few reasons why Macklem wants to hold the policy rate where it is — at least for now.

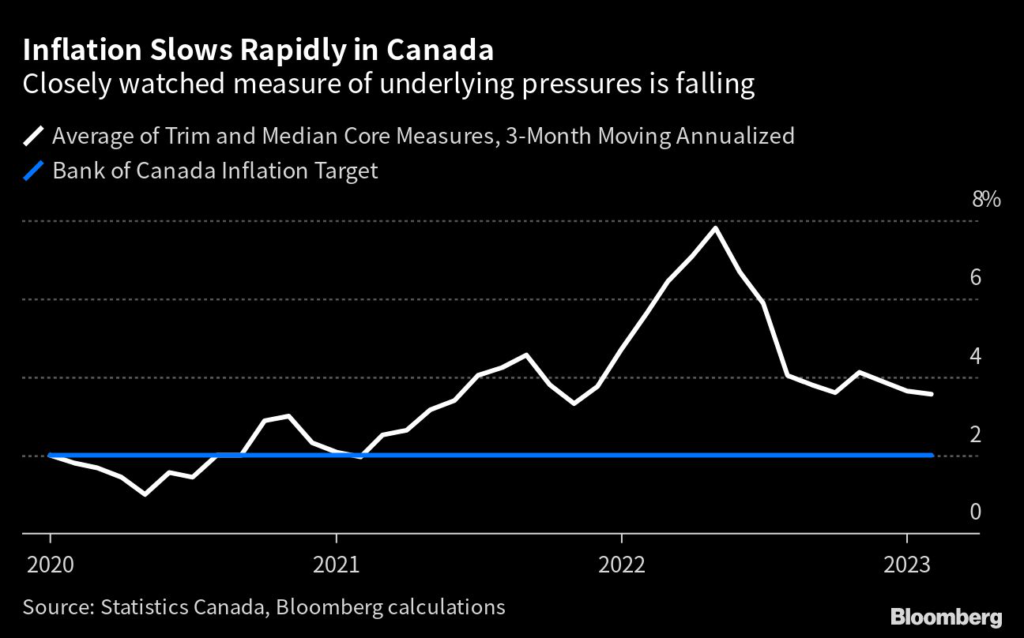

The most important is that inflation, while still far above the bank’s 2% target, is cooling and appears to be on a path to be closer to 3% by midyear, in line with forecasts.

After peaking at 8.1% last June, the yearly change in the consumer price index slowed to 5.2% in February, thanks largely to base effects and falling energy prices.

Core inflation is around 5% annualized, but a shorter-term core measure — one that officials say they’re closely watching — has eased to 3.5%.

That’s in line with falling price pressures in the US and elsewhere, with March data due from the Bureau of Labor Statistics an hour and a half before Macklem’s decision.

This week’s Bank of Canada release will include updated forecasts in a new monetary policy report that will factor in expanded fiscal support from Prime Minister Justin Trudeau’s government, which laid out its spending plans last month.

It’s also an opportunity for officials to try to address the impact of weaknesses in the global banking system.

The last rate decision came just two days before the collapse of Silicon Valley Bank, which was soon followed by an emergency sale of Credit Suisse to UBS.

The financial turmoil has stirred talk of global slowdown and changed expectations for how much further the Federal Reserve will lift rates, taking some pressure off the Macklem and his governing council.

The events helped reverse the Canadian dollar’s descent — the loonie has gained 2.7% versus the US dollar in the past month.

As the first among its peers to stop raising rates, the Bank of Canada can make good on its pledge to hold borrowing costs steady while it assesses how the economy is evolving — and in this case, how much damage the US and European banking problems will cause.

In effect, Macklem can point to international concerns as a reason to stay on the sidelines, even though the domestic economy looks stronger than expected.

Wage growth is running at a 5% yearly pace, a level the bank says is inconsistent with a return to the inflation target in the absence of productivity growth.

With some of Canada’s largest unions poised for strike action, there’s upside risk to sustained pressure to incomes. And while economic growth did pause in the fourth quarter, household consumption rebounded, in part due to generous government spending.

Canada’s population growth is one of the highest in the OECD, which pushes up economic growth and price pressures in the short-run — including housing costs — while adding a new workers who can help alleviate supply constraints in the long run.

That could mean the economy could be running at a less inflationary pace than officials previously guessed.

Given “the surge in population growth over the past year, we could see the Bank of Canada revising up its potential growth estimate for 2022,” Benjamin Reitzes, macro strategist with Bank of Montreal, said by email.

“That, in turn, would likely mean less excess demand, and support policymakers’ move to the sidelines.”

Macklem and Senior Deputy Governor Carolyn Rogers will field questions from reporters at 11 a.m.

on Wednesday, an hour after the public release of the rate statement and forecasts.

(Updates with pending US inflation release.)

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.