Surging interest rates have triggered vastly divergent reactions from European homeowners, with Spaniards rushing to pay off mortgages, while Germans are pulling back.

(Bloomberg) — Surging interest rates have triggered vastly divergent reactions from European homeowners, with Spaniards rushing to pay off mortgages, while Germans are pulling back.

In the first five months of 2023, early repayments jumped 24% in Spain and 23% in Portugal , according to Bloomberg calculations based on data from the European Central Bank.

That compares with a drop of 39% in Europe’s largest economy and 42% in the Netherlands.

Much of the difference is explained by the prevalence of variable interest rates.

Mortgage payments in southern Europe tend to fluctuate with the rates set by the ECB.

The one-year Euribor — the reference rate for most variable-rate Spanish mortgages — has soared above 4% from below zero since the middle of last year, and some borrowers in the region now have to pay three times as much in interest as they did just 12 months ago.

Conditions are similar in Portugal.

In the Spanish town of Granollers, Jaume Escudero is one of many homeowners in southern Europe who took action. The 48-year-old chemical company executive cashed in some investment funds to chop down his €200,000 ($224,500) loan to just €80,000.

The move lowered his home-loan payment to about €800 a month compared with double the amount if he had done nothing.

“Every spare euro I have is now going toward amortizing my mortgage,” said Escudero.

“It’s a great investment.”

For homeowners with floating rates, “it makes total sense financially to pay off a bit of the mortgage if you have some money put away,” said Angel Talavera, head of European economics at Oxford Economics in London.

The situation is different in countries, where fixed rates are more common.

In Germany, for instance, most mortgage holders have locked in interest levels for 10 years or longer. That means ECB rate hikes don’t have an immediate impact, so at a time when budgets are squeezed by surging prices, home-loan concerns can be more easily deferred.

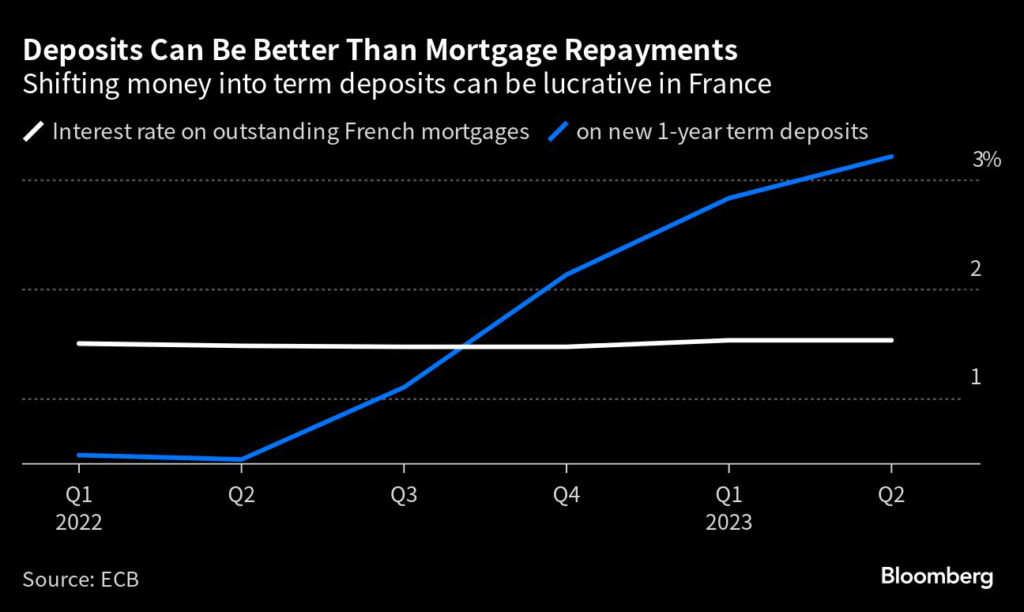

For those with spare cash, putting money into savings rather than paying off cheap loans makes sense. Savers in France earn an average of more than 3% on one-year term bank deposits and 2.6% in Germany.

Those differing incentives have had a major impact.

In the first five months of 2023, mortgage repayments across France, Germany and the Netherlands dropped a combined €59.5 billion compared with the same period a year ago, according to the data. By contrast, they rose by €8.9 billion in Italy, Portugal and Spain.

The figure are an approximation based on subtracting adjusted net lending flows from total loan origination.

“When interest rates rise, people in Germany tend not to repay because they can earn more from a deposit than what they pay for their fixed-rate mortgage,” said Valeriya Dinger, an economics professor specializing in banking at Osnabruck University.

“That’s what we’re seeing now.”

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.