(Bloomberg) — Almost exactly a year after China’s property-market debt squeeze sparked the first in a wave of defaults by developers, the industry is fighting for survival.

Home sales continue to plunge and elevated borrowing costs mean offshore refinancing is off the table for many developers.

Global agencies are pulling their ratings on property bonds, while a string of auditor resignations is adding to doubts over financial transparency only weeks before earnings season. An 81% stock plunge in Zhenro Properties Group Ltd.

highlighted the risks of margin calls as companies struggle to repay debt.

Yu Liang, chairman of China Vanke Co. — one of the country’s largest developers — urged staff to prepare for a battle that could make or break the firm, according to the South China Morning Post, which cited an internal document from last month.

“We are on our last legs, which means there are no other options,” he said.

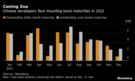

A Bloomberg index of Chinese junk dollar debt fell every day this week through Thursday, driving yields above 20%.

A gauge of Chinese property shares is down 3.4% this week, taking its losses over the past 12 months to 28%, even after rallying on Friday.

As the cash crunch for developers worsens, so does the housing slowdown that’s become one of the biggest drags on China’s economy.

Attempting to deflate a speculative market is a risky strategy that — if uncontrolled — could threaten Beijing’s pledge to prioritize economic stability this year. Regulators have quietly tweaked some rules to engineer a soft landing for the property industry, such as encouraging mergers and acquisitions, but so far officials have refrained from any substantive easing of curbs.

“While the government has become more supportive, measures have remained marginal and have not solved the liquidity crisis,” said Paul Lukaszewski, head of corporate debt for Asia Pacific at abrdn Plc in Singapore, which has portfolios with exposure to developers.

“The market turmoil and ongoing uncertainty have pushed traditional investors to the sidelines.”

China Fortune Land Development Co. failed to repay a $530 million dollar bond due Feb. 28., 2021, becoming the nation’s first real estate firm to default since Beijing drafted new financing limits for the sector in 2020.

Since then, at least 11 developers defaulted, according to a Feb. 3 report by Standard Chartered Plc.

More may follow. Property firms have to find almost $100 billion to repay debt this year, even as their income streams shrink.

Sales at China’s 100 biggest developers fell about 40% in January from a year earlier, compared with a 35% decline in December, according to preliminary data by China Real Estate Information Corp.

Developers are selling more onshore bonds to fund project construction, but not enough to cover maturing debt.

Onshore issuance by Chinese developers fell 53% in January to 23 billion yuan ($3.6 billion), while dollar note sales were down 90% from a year earlier to just $1.6 billion, according to China International Capital Corp.

Net financing, which subtracts maturities from issuance, was a negative $7.3 billion, CICC analysts led by Eric Yu Zhang wrote in a Friday note.

Investors also need to worry about off-balance sheet debt.

Fallen angel Shimao Group Holdings Ltd. recently proposed delaying repayment of about 6 billion yuan of high-yield trust products due between this month and August, people with the matter said this week.

Its bonds sank on concern the company will prioritize these liabilities over money owed to offshore creditors.

Auditor resignations are sowing further doubt about the financial health of property firms.

Auditors for Hopson Development Holdings Ltd. and China Aoyuan Group Ltd. resigned in late January, citing insufficient information and a disagreement over fees, respectively. Shimao’s onshore unit changed its auditor for the first time in 27 years.

Failure to publish results before the Hong Kong stock exchange’s March 31 deadline may lead to long trading halts.

“Changing accounting firms just ahead of year-end results raises questions about the quality of a firm’s governance,” S&P Global Ratings analysts wrote in a Feb.

16 report.

Investor distrust of management is becoming entrenched. Rumors about Zhenro’s ability to repay a perpetual bond sent the note from near par to drop below 23 cents in a matter of days, while its shares sank amid reports holder Ou Zongrong had been forced to liquidate.

The stock didn’t recover even as the company said such speculation was “untrue and fictitious.”

Zhenro said late Friday it may be unable to repay debt due in March, including its perpetual bond.

The company had earlier pledged to redeem the securities.

Authorities are taking steps to ease funding restrictions for the sector, although these measures are largely targeted and incremental, rather than broad-based.

The government recently issued rules to standardize the use of presale funding, banks extended more loans to the sector and some lenders in several cities have cut mortgage downpayments, according to multiple local media reports in the past week.

A Bloomberg Intelligence index of Chinese property stocks rose as much as 3% on Friday following the mortgage report, while high-yield dollar bonds halted their decline.

Even so, credit stress remains “acute” and funding channels aren’t showing much of an improvement, according to Goldman Sachs Group Inc.

analysts.

That means defaults are likely to pile up for developers that struggle to sell assets fast enough. State-owned companies have emerged as potential buyers, though the pace of deals so far has been slow.

Any distressed-debt investor buying defaulted bonds now is likely to face a lengthy wait before recovery.

Among the past year’s defaulters, only Fortune Land has released a preliminary restructuring framework for its debt. An estimated $48.9 billion is outstanding pending debt resolution, according to Standard Chartered.

While Chinese authorities have told state-owned bad-debt managers to participate in the restructuring of weak developers, it’s unclear what such support might mean for bondholders.

In China’s property sector, court-led restructurings are rare, data compiled by Bloomberg show. Since 2018, 27 firms have failed to honor their bonds, and only two entered such a process.

“Price volatility in the sector is unlikely to subside,” wrote Citigroup Inc.

strategists including Dirk Willer in a Friday note. “Even the recent rebound in new real estate loans did not provide much relief to the deteriorating sentiment.”

(Updates to add Zhenro statement on likely non-payment in 14th paragraph.)

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.