(Bloomberg) — After a brutal 12 months for Chinese equities, Wednesday’s session was looking like a tepid bounce off multi-year lows until the headlines started rolling from Beijing. Then greed quickly replaced the panicked selling of the past few days.

In a brief statement carried by state media, China’s top financial policy body vowed to ensure stability in capital markets, support overseas stock listings, resolve risks around property developers and complete the crackdown on Big Tech “as soon as possible.” Yi Gang, governor of the People’s Bank of China, followed with a statement saying the central bank would help implement the policies, as did the banking watchdog.

While the pledges from President Xi Jinping’s government offered little clarity over what authorities may do to achieve their goals, it was the first time China publicly addressed investors’ top concerns in one coordinated swoop.

The move underscored Xi’s focus on ensuring economic and financial stability before a Communist Party congress at which he’s expected to secure at least another five years in power.

By the time trading ended just after 4 p.m.

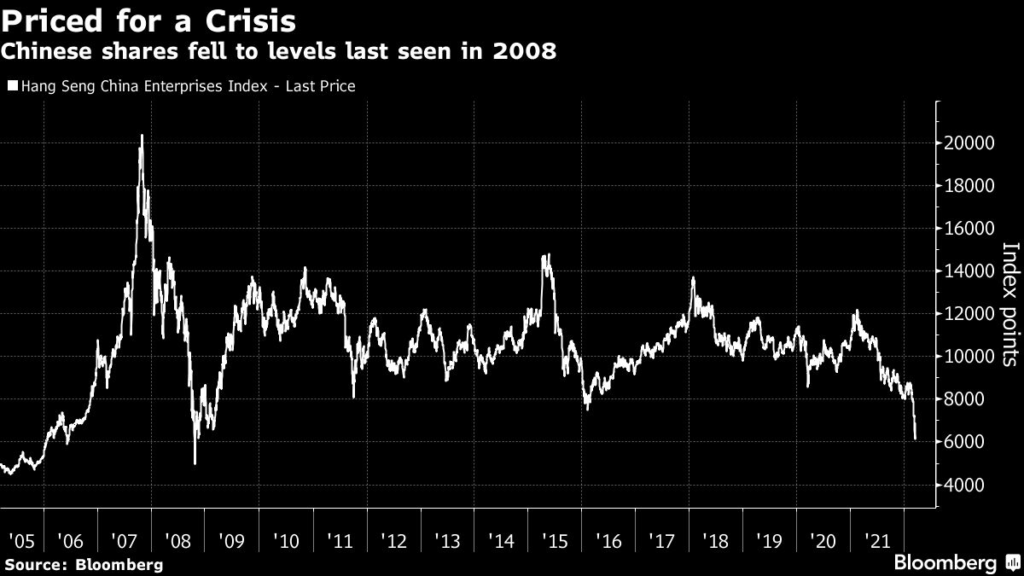

local time on Wednesday, the Hang Seng China Enterprises Index was up 12.5% in its best session since October 2008. Alibaba Group Holding Ltd. surged 27%, while JD.com Inc. jumped 36%. Property stocks rallied the most in more than a decade.

“It’s the end of capitulation,” said Peter Garnry, head of equity and quantitative strategy at Saxo Bank.

“This confirms that the Chinese government sees healthy and strong equity markets as key for the country going forward. The equity market is totally sentiment driven right now and everyone is looking for an excuse to buy, though the headwinds for Chinese equities are still enormous.”

The need for the government to act has been growing more urgent.

Global confidence in Chinese financial markets was by some metrics the weakest since the financial crisis in 2008, with stocks cratering, credit plunging and record outflows from government bonds undermining the currency’s strength.

Xi also faced more political pressure to bolster the economy, with rising Covid cases spurring lockdowns that threaten to hinder growth and disrupt life for millions of people.

The State Council statement made a veiled reference to his political imperatives, calling on all parties “to deeply understand the significance of the “‘two establishes’” in keeping the economy and markets stable — jargon that affirms Xi’s position as the Communist Party’s most important figure.

Government departments should “actively introduce policies that benefit markets,” according to a meeting of the Financial Stability and Development Committee, led by Vice Premier Liu He, who’s in charge of overall economic policy.

China also supports firms listing overseas and has achieved positive progress in discussions with Washington over Chinese stocks on U.S.

exchanges, Xinhua’s report of the meeting said, adding that both sides are working to formulate a detailed cooperation plan. Concern that companies like Alibaba might need to delist from overseas markets had been a major driver of the selloff in recent days.

The equity slump began last year in large part because of policies introduced by Beijing, including crackdowns on tech firms and property developers.

More recently investors had started to brace for worst-case scenarios like sanctions against China for its perceived support of Russia. It all came at a time of increased market turmoil globally with Russia on the brink of a default and the Federal Reserve set to raise interest rates.

The pace of selling has been savage.

The Hang Seng China gauge plunged 24% this month through Tuesday. Even after Wednesday’s surge, the index is down about 40% in the past year, the worst performance globally. Chinese stocks in the U.S.

have lost 75% from their 2021 peak, while the yield on Chinese junk dollar debt has surged above 27% for the first time.

The yuan has also started to look vulnerable. Selling momentum in the offshore Chinese currency on Monday reached an intensity only seen a handful of times in the past five years.

The yuan suffered the biggest real-money net outflows among all global emerging-market currencies last week, according to Citigroup Inc. calculations based on client trades.

For Wednesday’s rally to continue, China’s policy makers will need to follow through with actions.

Promises to keep markets stable were vocalized in January by the securities regulator, which has made no known intervention since. Assurances of dialog with the U.S. regarding the auditing Chinese ADRs have been made before.

The easing of funding rules for property firms have so far been incremental.

The high-level meeting also didn’t mention Russia’s invasion of Ukraine, which has fueled an oil price spike and concern among investors that Chinese companies might be subject to sanctions.

There are additional risks to markets outside Beijing’s control, including the spread of the highly contagious omicron variant across major Chinese cities, the Fed’s tightening path and the derisking of portfolios globally — with money managers the most pessimistic about the international economy since 2008.

A short squeeze may have exacerbated the gains.

Short selling comprised about a quarter of Hong Kong’s total daily turnover on Monday and Tuesday. Such speculators traded more than 10 million Tencent shares on Monday, the most in more than a year.

The rally’s staying power will depend in part on the reaction of foreign investors, whose role in Chinese markets has never been so important.

Between the start of 2019 and the end of 2021, overseas holdings of local stocks increased by more than 242% to 3.9 trillion yuan ($613 billion). Inflows into the nation’s bond market rose by 129% to 4.1 trillion yuan.

China has taken forceful measures to shore up its financial markets before, to mixed success.

Two years ago, the central bank and regulators across industries issued more than 30 supportive measures to counter the impact of the coronavirus outbreak.

Regulators also banned mutual funds and proprietary traders at brokerages from selling more stocks than they buy. While the domestic CSI 300 Index sank as much as 9.1% as trading opened after an extended break, the benchmark ended the year up 27%.

A heavy-handed approach to managing market swings can backfire, like it did for China after a stock bubble burst in 2015, when botched interventions helped accelerate selling.

The CSI 300 didn’t recover its 2015 high until five years later.

“I do not believe this is a turning point — we are in a very turbulent period,” said Sean Debow, chief executive officer of Eurizon Capital Asia.

“In order to catch a falling knife you have to have very very strong conviction, and we don’t have that yet.”

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.