(Bloomberg) — China looks increasingly left to its own devices in a bid to rescue its economy and markets from the Covid crisis as the rest of the world withdraws stimulus to battle surging inflation.

Unlike in 2020, when Beijing was able to limit disruptions to its manufacturing hubs and rely on unprecedented global liquidity to shore up investor confidence, this time it has to go it alone. A strict Covid Zero policy has left it stuck in a repeat of lockdowns while other countries have turned to reopening their economies.

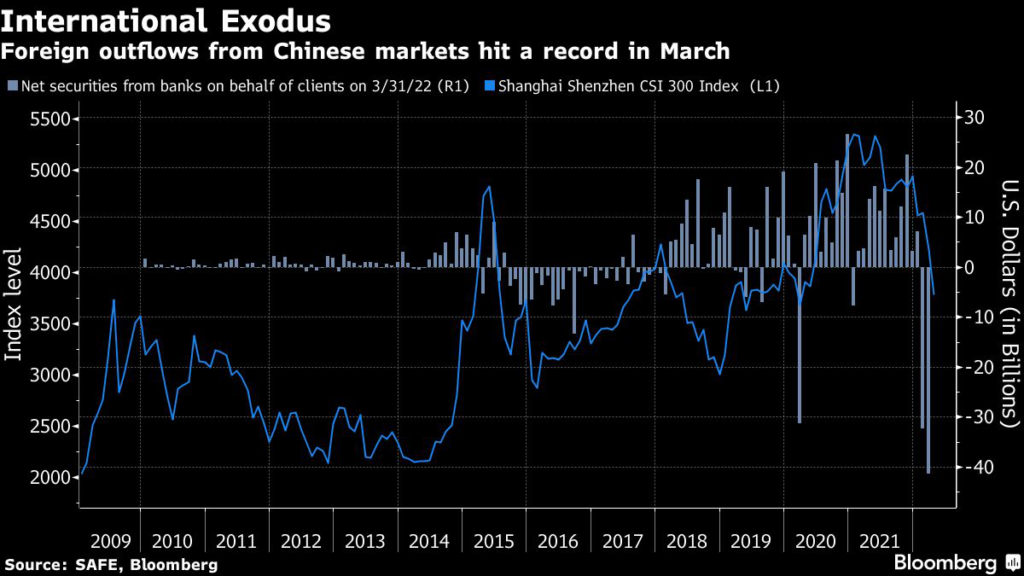

International funds are selling out of Chinese assets, while efforts to encourage domestic money into capital markets aren’t working as protracted restrictions and a slowing property market erode wealth. The People’s Bank of China, which on Tuesday vowed once more to support the economy, seems wary to overstimulate, preferring to limit financial risk, rein in debt and keep inflation under control.

“The PBOC’s struggle reflects the broader predicament Chinese policy makers are facing amid a challenging external environment — how to find balance between contradictive policy goals of zero Covid and a 5.5% economic growth target,” said Seema Shah, chief strategist at Principal Global Investors in London. “This is not the time to go overweight given the uncertainty that lies ahead.”

Investor recognition of the difficulties facing the Communist Party is etched into the performance of China’s lagging assets. Down 23% this year, the benchmark CSI 300 Index remains mired in a bear market. The once-resilient yuan has slumped to near the weakest since November 2020.

Borrowed Stimulus

When Covid first surfaced in Wuhan, China’s ability to put off a widespread outbreak meant it benefited from historic global stimulus without having to provide too much of its own. Foreign investors clamored for mainland stocks and bonds, as one of the few economies that could absorb that kind of money.

The surge in demand for made-in-China goods drove a record trade surplus last year that accounted for about a fifth of the country’s economic expansion, more than offsetting weak domestic consumption. So much capital flowed into China that the yuan was one of the best performing currencies in the first two years of the pandemic.

Such success gave Chinese officials the confidence to get their house in order. While the rest of the world bought into speculative frenzies from meme stocks to cryptocurrencies, Beijing took action to deflate bubbles in its property and credit markets. It ramped up regulation for entire industries like education, gaming and Big Tech, even though the moves sent stocks tumbling in China and Hong Kong.

Omicron Arrives

But the window to pursue many of President Xi Jinping’s ideologies looked to have closed in January with the arrival of the more transmissible omicron variant. That ramped up pressure on financial markets and pushed China’s central bank to cut interest rates for the first time in almost two years.

China has since taken more decisive actions to spur growth and prop up markets, but with little visible success. Just this month, authorities freed up liquidity in the banking system, nudged the country’s social security fund, banks and insurers to boost equity investments and made foreign currency more readily available onshore in a bid to stop the yuan from weakening further.

The PBOC on Tuesday said it will promote the healthy and stable development of markets and provide a good monetary and financial environment. It reiterated that liquidity will remain reasonably ample.

Skeptics Prevail

Given the fluctuations in Chinese shares and the yuan Tuesday, skepticism prevails. Any relaxation in lending conditions will have a limited impact at a time businesses and consumers are unwilling to take on more debt, the thinking goes.

Inflows into mainland markets remain muted. The CSI 300 and yuan are both weaker than where they were when policy makers became even more vocal with pledges of support in mid-March — around the time the Federal Reserve first hiked interest rates.

Of course, there may be other lifelines for China’s financial markets. An approval of foreign-made vaccines on the mainland or the distribution of treatments would suggest Beijing is planning to exit its Covid-Zero strategy. The Fed could turn out less hawkish than anticipated if economic recession becomes a real possibility. Beijing could even start talking about the prospect of reopening its borders.

Global Impact

But it’s difficult to overstate the global significance of what’s happening in China. Beyond the ramifications of a slowdown in the world’s second-largest economy, whack-a-mole lockdowns are worsening a supply chain crisis now entering its third year. The disruption is adding to inflation woes, corporate earnings worries and stagflation concerns for the U.S. and European economies.

For now at least, Xi’s commitment to Covid Zero will cast a shadow over everything else, even China’s relationship with Russia after the invasion of Ukraine. The focus is turning to a Politburo meeting expected to be held this week, where discussion will likely be dominated by the economy.

“The question mark is how are they going to manage the overall economic policy when it’s in conflict with zero Covid, that’s very complicated,” said Zhikai Chen, head of Asian equities at BNP Paribas Asset Management. “We just need a few quarters of no more of this kind of ‘noise’.”

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.