(Bloomberg) — A debt crisis in China’s property industry has sparked a record wave of defaults and dragged more developer bonds down to distressed levels.

Risks are now spreading to even higher-rated borrowers.

A property firm long considered among the nation’s most resilient, Greenland Holdings Corp., shocked investors last week with a proposed dollar-bond payment delay. Earlier this month, China’s fourth-largest developer, Sunac China Holdings Ltd., became one of the biggest to default.

That suggested most private Chinese developers face the risk of a missed payment if they can’t access fresh financing, according to some analysts.

Refinancing in global debt markets is out of the question for many firms after average yields on their junk dollar notes jumped above 20%.

Covid lockdowns in Shanghai and elsewhere have added to pressure on home sales, amid a sector cash crunch sparked by a crackdown on excessive leverage. Goldman Sachs Group Inc. analysts recently raised their projected 2022 default rate for high-yield Chinese developers to 31.6% from a previous forecast of 19%.

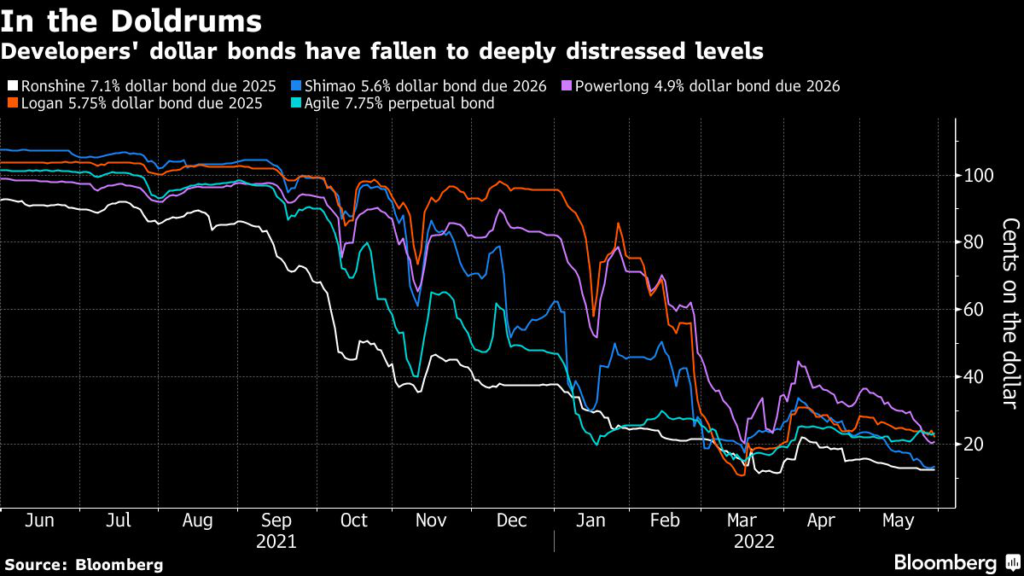

The following is a list of the five developers in a Bloomberg index of Chinese high-yield dollar bonds that have at least one such security indicated below 25 cents on the dollar, and that each have at least $600 million of onshore and offshore note payments due the rest of this year.

The firms didn’t immediately have a comment when contacted by Bloomberg. Debt figures mentioned below are based on data compiled by Bloomberg. The developer rankings cited are by sales and are from China Real Estate Information Corp.

Shimao Group Holdings Ltd.

The luxury builder was previously considered among China’s healthier property firms.

But its status as one the sector’s biggest bond issuers left investors concerned about its liquidity as the broader industry crisis deepened, and the company lost its investment-grade ratings. This month, Shimao’s key onshore unit for the first time sought to delay repayment on a public onshore note.

The country’s 20th-largest developer this year by contracted sales has $2.1 billion of bond payments to make the rest of 2022, including a $1 billion dollar note maturing July 3.

Meanwhile, trading of its shares in Hong Kong has been suspended since the start of April because it hasn’t released 2021 results.

Agile Group Holdings Ltd.

Investor views are split between the immediate and the longer term risks when it comes to Agile, which develops villa apartments and high-rise homes set amid landscaped gardens.

Its bonds due in August jumped above 80 cents on the dollar after some recent loan payments. But the firm’s other offshore notes range from 23 cents to 39 cents, highlighting longer-term concerns.

Agile, China’s 28th-biggest builder, has $1.16 billion of bond obligations due through year-end, including $600 million of principal on the August notes and a 1.5 billion yuan ($225 million) security due in July.

Its shares earlier this month hit a 13-year low.

Ronshine China Holdings Ltd.

China’s 23rd biggest builder garnered attention in February, when its dollar securities fell amid a slump at Zhenro Properties Group Ltd.

That firm’s founder is a brother of Ronshine Chairman Ou Zonghong. But unlike Zhenro it’s avoided having to seek debt exchanges and hasn’t missed any note payments.

Ronshine has $937 million of bond payments yet to make this year, with the lion’s share being a $688 million note due in October.

Ronshine was among developers whose auditor resigned during the recent earnings season, and its 2021 report is slated to be released by Tuesday.

Logan Group Co.

Worries about the possible scale of builders’ undisclosed leverage has kept Logan in the spotlight.

Two major credit rating firms withdrew their grades on the builder in the past two months, part of a wave of such actions in the sector this year. The company earlier this month asked its auditor to resign, saying a timetable to complete the 2021 audit couldn’t be reached.

Logan has a scheduled $1 billion of note payments the rest of this year that include a $279 million bond in August.

The company, China’s 22nd-largest builder, has had its shares halted since May 12 amid the lack of audited results.

Powerlong Real Estate Holdings Ltd.

The Shanghai-based developer’s notes have been among May’s worst performers after the city’s Covid lockdowns.

Powerlong, which also builds commercial projects and is a shopping-mall owner, ranks 43rd this year by contracted home sales. It has $694 million of onshore and offshore bond payments due the rest of this year, including a $200 million note maturing July 25.

The firm conducted repurchases and redemptions earlier this year.

But market prices have signaled continued concern recently, with July’s offshore note back at 50 cents on the dollar and most others below 30 cents. A Powerlong unit said Friday it won’t redeem a 500 million yuan perpetual note, which would increase the bond’s coupon by three percentage points.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.