(Bloomberg) — Crypto mining giant Marathon Digital Holdings Inc. had its best weekly gain since February 2021, leading a rally in digital-asset shares as the crypto market enjoyed a respite from recent steep declines.

The stock’s gains, while impressive, were nowhere near enough to erase losses incurred this year.

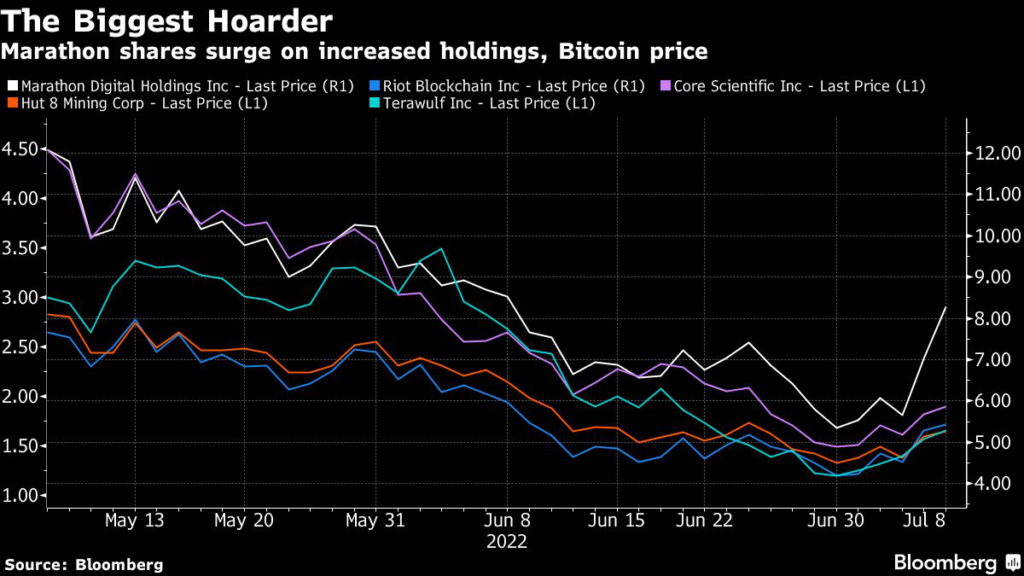

Marathon surged 54% in a holiday-shortened week to close at $8.51 in Nasdaq trading, with Bitcoin on track for its biggest weekly gain since March.

Other top public miners also rose: Riot Blockchain and Core Scientific each advanced more than 30%. Even after the gains, Marathon is down almost 75% so far in 2022, while the broader NYSE FactSet Global Blockchain Technologies Index is down 65%, reflecting a tumble in cryptocurrencies that wiped out some $2 trillion in market value since last fall.

Las Vegas-based Marathon outpaced its rivals after announcing Thursday that it added 4,769 Bitcoin back to its balance sheet following a decision to unwind an investment in New York Digital Investment Group.

That brings its total holdings to 10,055 coins, or about $200 million worth. Marathon is one of the few miners that have held on to all of their mined coins in the prolonged “crypto winter.” Others have been forced to sell part of their holdings to cover operational costs and repay debt as digital-asset price declines squeeze their profit margins.

Core Scientific sold nearly 80% of its Bitcoin holdings, while Riot increased its sale in June compared to previous months.

Marathon also reported a better-than-expected cash position, according to D.A.

Davidson analyst Chris Brendler. And unlike other major miners, Marathon uses third-party operators to run its machines rather than building its own facilities, which requires hefty overhead costs and more debt.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.