It’s getting harder for the private equity industry to hang on to long-term assets while still raking in the fees they throw off.

(Bloomberg) — It’s getting harder for the private equity industry to hang on to long-term assets while still raking in the fees they throw off.

Institutional investors are souring on so-called continuation funds, which private equity firms deploy when they want to keep managing assets in traditional buyout funds that are about to mature — often to avoid taking portfolio companies public prematurely or being forced to sell them at unfavorable prices.

Demand for such vehicles, which soared during the pandemic, tumbled in the first half of this year after hitting a record $60 billion in 2021, according to a report by Campbell Lutyens & Co., a private markets advisory business.

In addition to providing an off-ramp for investors who want to cash out, continuation funds allow buyout firms — also known as general partners — to keep raking in management fees from existing or new clients.

While the number of proposed continuation funds coming to the secondaries market isn’t necessarily declining, “the percentage of those deals that are closing is certainly down,” Campbell Lutyens partner Gerald Cooper said in an interview.

“Valuation is much more of a concern today than it was 12 months ago,” said Eric Albertson, senior investment director at Abrdn Plc.

“No one wants to invest in a deal and then 6 or 9 months later have a writedown.”

That helps to explain the recent rut.

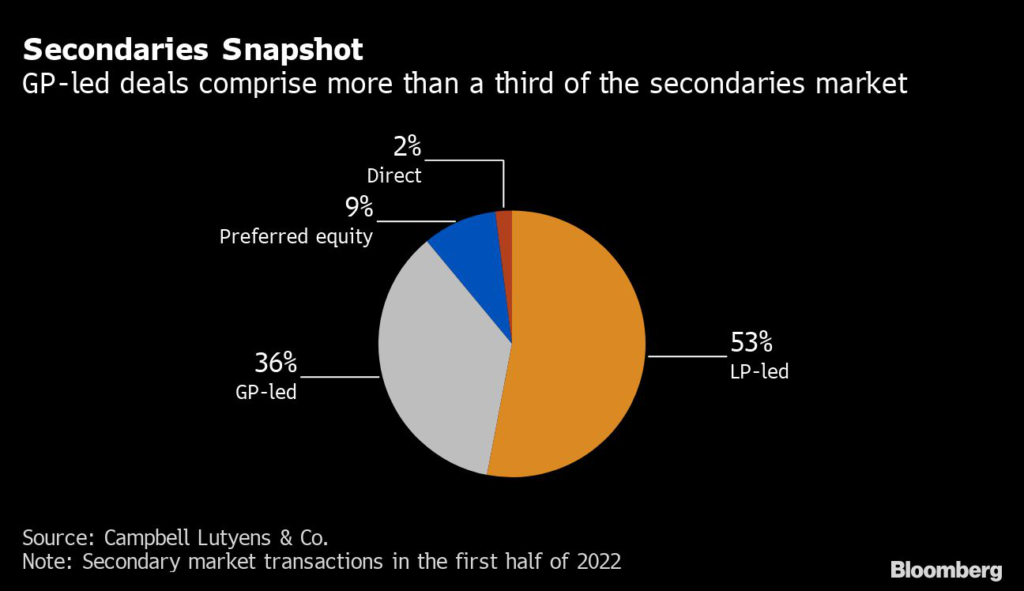

The value of GP-led deals that closed during the first half — the vast majority of them were continuation funds — totaled $19 billion, a 32% drop from the same period a year earlier, Campbell Lutyens said in a report last month.

Private-market pricing lags behind public markets by several quarters, and valuations didn’t dip as much as investors expected in the second quarter, creating a “pause” in the secondary market, said Cooper, adding that there isn’t enough demand to absorb all of the supply.

Because of that lag, the slowdown is expected to continue until the end of the year or early 2023, said Samer Ghaddar, deputy chief investment officer at the Arizona State Retirement System.

“A contraction in valuations is still in its early phase,” he said in an emailed statement.

More broadly, institutional investors including pension funds and university endowments are pulling back from committing fresh capital to private equity because their portfolios are now over-invested in the asset class following a sharp decline in public equities.

Read more: Ivy League Endowments Brace for Losses With PE Values Tumbling

While the Campbell Lutyens report shows that more than three-fifths of GP-led deals were sold between par and a 5% discount, Albertson said he’s aware of transactions in which limited partners sought haircuts of as much as 20% compared with year-end prices.

And several deals put forth last year had to be renegotiated as investors sought better pricing, according to secondaries brokers who asked not to be identified.

Valuations Slide

In January, for example, Banneker Partners sold a minority stake in education-software business LINQ to Welsh Carson Anderson & Stowe.

Banneker recently arranged a continuation fund for the rest of its holding, though the new investors wanted a lower valuation than the one secured months earlier with Welsh Carson.

A Banneker representative declined to comment.

Resilience Capital Partners had planned a $326.1 million continuation fund that included as many as 18 companies from two existing vehicles, according to a presentation seen by Bloomberg.

But the firm recently shelved the offering, according to a person familiar with the matter.

First Ascent Ventures GP, a Toronto-based firm that sought C$120 million ($80 million) for three portfolio companies, paused plans to roll them into a continuation fund because of unfavorable pricing conditions, a person familiar with the matter said.

“I would be surprised if most of the deals that were in market in the first quarter didn’t have some level of renegotiation,” Cooper said.

One of the largest proposed continuation funds so far in 2022 is being arranged by Madison Dearborn Partners, which is seeking as much as $3 billion to extend its ownership of three insurance firms.

Read more: Madison Dearborn Partners Seeks $3 Billion in Secondary Deal

Continuation funds can be controversial because the general partner is on both sides of the deal, raising questions about how it determines the valuation, which sets the basis for the fees it charges.

The Securities and Exchange Commission has proposed rules that would enhance transparency, including that each deal get an outside fairness opinion.

“To attract new investors, GPs tend to offer assets at higher discounts, which is naturally a conflict to existing LPs as they see a markdown in their valuations,” said Ghaddar, of the Arizona retirement system.

Lower management fees and a new carry structure help to ease such conflicts, and “some GPs do address that,” he said.

High Bar

John Beil, the head of private equity and real estate investments at Partners Capital, said his firm evaluates continuation funds on a series of criteria, including whether a fairness opinion accompanies the transaction and if the general partner is re-investing most of its earnings from the “sale” of the asset into the new fund.

“The bar is high to elect to roll our capital,” said Beil, whose firm advises on more than $48 billion for endowments, foundations and pensions.

In most cases, it opts to take a cash payment because higher returns can be found elsewhere, he said.

Limited partners may also demur because of the amount of work required to evaluate continuation funds, which are treated like entirely new investments even though the underlying assets were in previous funds, Beil said.

In some instances, GPs give clients as little as two weeks to decide whether they want in or out, according to investors and advisers.

Hiring external consultants for due diligence on the quality of an asset and its valuation takes time, forcing investors to cash out, they said.

But with about $110 billion of dry powder in the market, according to Prequin data, the slowdown may only to be temporary.

“It’s going to be a tool for years to come,” Kate Ashton, leader of alternative assets transactions at Debevoise & Plimpton.

“Private equity GPs are going to look at some form of continuation fund structure as an alternative exit in many different circumstances to a traditional sale or IPO.”

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.