The pound rallied and UK bonds surged amid expectations that more of Prime Minister Liz Truss’s package of unfunded tax cuts will be reversed. Stocks rose, with investors preparing for a number of key earnings reports this week.

(Bloomberg) — The pound rallied and UK bonds surged amid expectations that more of Prime Minister Liz Truss’s package of unfunded tax cuts will be reversed.

Stocks rose, with investors preparing for a number of key earnings reports this week.

Chancellor Jeremy Hunt is expected to make a statement at 11 a.m. London time on measures to support fiscal sustainability, a UK official said.

It’s the start of what may be a particularly torrid week for UK assets, with the beleaguered Truss battling to rescue her premiership after the Bank of England ended its emergency bond-buying program on Friday and as mutinous backbenchers plot to oust her.

US equity contracts gained as investors turned their focus to earnings — including from Bank of America Corp., Goldman Sachs Group Inc.

and Tesla Inc. US-listed Chinese shares rose in premarket trading, while Chinese stocks erased declines as President Xi Jinping reiterated that economic development is the party’s top priority and offered support for the tech sector in a speech, but disappointed investors hoping for signs of a shift away from Covid Zero.

Utilities and insurance stocks led gains in Europe.

The yield on 10-year gilts fell 28 basis points to 4.05% and the pound traded 0.8% higher at $1.1264. Treasury yields and the dollar eased against its Group-of-10 counterparts, providing a touch of respite to harried currency markets.

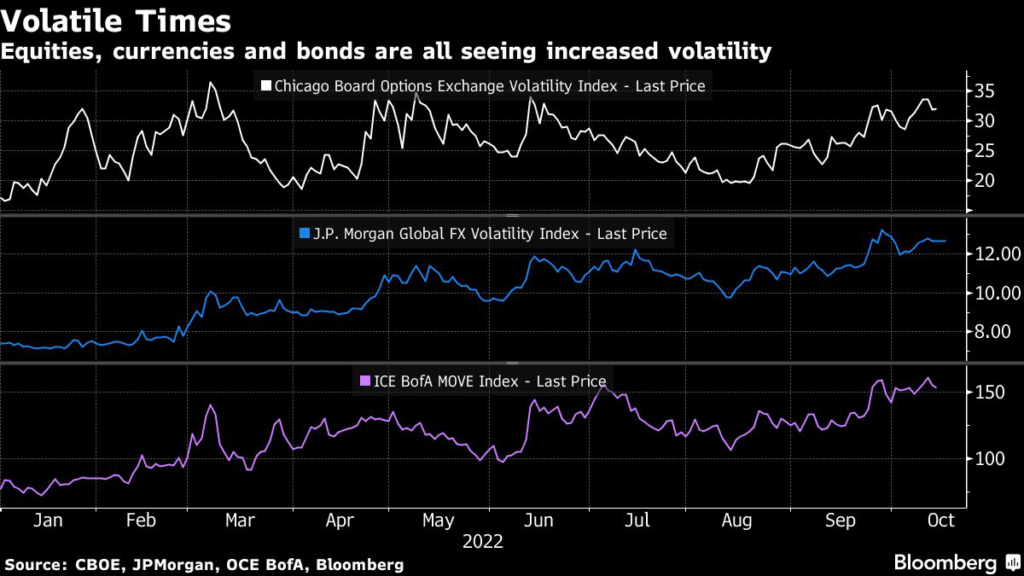

“I think we’re in for a period where UK credibility is continually questioned and UK assets remain incredibly volatile for a significant period of time,” Benjamin Jones, Invesco Director of Macro Research, said on Bloomberg Television.

“Watching the gilt market will be absolutely key in understanding if the market does believe Hunt to be more stable and if he will be able to push these policies through.”

Hunt will also speak to the House of Commons at 3:30 p.m.

London time and Truss is due to host a reception for the Cabinet at 10 Downing Street on Monday evening. While early gains for the pound suggested confidence in Hunt’s alternative approach, economists still warn there is a budget hole ranging from £28 billion to £50 billion to fill, depending on the pace of debt falling.

Meanwhile, the outlook for consumer prices in the US continues to fuel bets that the Federal Reserve may make jumbo rate hikes at its next two meetings, weighing broadly on the outlook for global economic growth and markets.

Fed officials in their latest comments suggested they were ready to hike rates higher than previously planned.

Kansas City Fed President Esther George said the terminal rate may need to be higher to cool prices. San Francisco Fed’s Mary Daly said she’s “very supportive” of raising to restrictive levels and to between 4.5% and 5% “is the most likely outcome.”

Morgan Stanley strategist Michael J.

Wilson, a long-time equities bear, said US stocks are ripe for a short-term rally in the absence of an earnings capitulation or an official recession. A 25% slump in the S&P 500 this year has left it testing a “serious floor of support” at its 200-week moving average, which could lead to a technical recovery, he wrote in a note on Monday.

Elsewhere in markets, oil fluctuated after a weekly slump as fears over an economic slowdown continue to weigh on the outlook for demand.

Gold rose on weakness in the US dollar and as rising fears of a global economic slowdown boost the precious metal’s haven status.

Key events this week:

- Earnings this week will provide clues on the strength of a swathe of companies, including Bank of America Corp., China Telecom Corp., Contemporary Amperex Technology Co., Hindustan Unilever Ltd, Hong Kong Exchanges & Clearing Ltd., Goldman Sachs Group Inc., Johnson & Johnson, Netflix Inc., Tesla Inc.

and United Airlines Holdings Inc.

- US empire manufacturing, Monday

- ECB Vice President Luis de Guindos speaks, Monday

- China retail sales, industrial production, GDP, surveyed jobless, Tuesday

- US industrial production, NAHB housing market index, Tuesday

- Fed’s Neel Kashkari speaks, Tuesday

- Euro area CPI, Wednesday

- UK CPI, PPI, retail price index, Wednesday

- US MBA mortgage applications, building permits, housing starts; Fed Beige Book, Wednesday

- Fed’s Neel Kashkari, Charles Evans, James Bullard speak Wednesday

- US existing home sales, initial jobless claims, Conference Board leading index, Thursday

Some of the main moves in markets:

Stocks

- The Stoxx Europe 600 rose 0.5% as of 9:55 a.m.

London time

- Futures on the S&P 500 rose 1%

- Futures on the Nasdaq 100 rose 1.2%

- Futures on the Dow Jones Industrial Average rose 0.8%

- The MSCI Asia Pacific Index rose 1.5%

- The MSCI Emerging Markets Index rose 1%

Currencies

- The Bloomberg Dollar Spot Index fell 0.2%

- The euro rose 0.2% to $0.9737

- The Japanese yen was little changed at 148.71 per dollar

- The offshore yuan was little changed at 7.2152 per dollar

- The British pound rose 0.8% to $1.1264

Cryptocurrencies

- Bitcoin fell 0.4% to $19,264.42

- Ether fell 0.1% to $1,309.29

Bonds

- The yield on 10-year Treasuries declined six basis points to 3.96%

- Germany’s 10-year yield declined 10 basis points to 2.24%

- Britain’s 10-year yield declined 28 basis points to 4.05%

Commodities

- Brent crude fell 0.3% to $91.39 a barrel

- Spot gold rose 0.6% to $1,654.91 an ounce

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.