For all the dour dot plots and hawkish hike forecasts in the Federal Reserve’s statement on rate policy and the economy, Jerome Powell barely laid a glove on stock and bond markets Wednesday.

(Bloomberg) — For all the dour dot plots and hawkish hike forecasts in the Federal Reserve’s statement on rate policy and the economy, Jerome Powell barely laid a glove on stock and bond markets Wednesday.

Big losses shrank to little ones in equities and bond yields ended lower, leaving rallies largely intact for both asset classes since the last Federal Open Market Committee meeting in November.

The outcome surprised many investors who expected more emphatic words of warning to markets whose buoyancy is seen as working against the Fed chair’s goal of subduing the worst inflation in 40 years.

“I don’t often criticize the Fed, but today has been a lesson in how not to communicate with markets.

So many mixed messages that I’ve lost count,” said Win Thin, global head of currency strategy at Brown Brothers Harriman & Co. “The Fed needed to get across one simple message today, and I think it failed.”

Not that Powell didn’t have opportunities to send a sterner message.

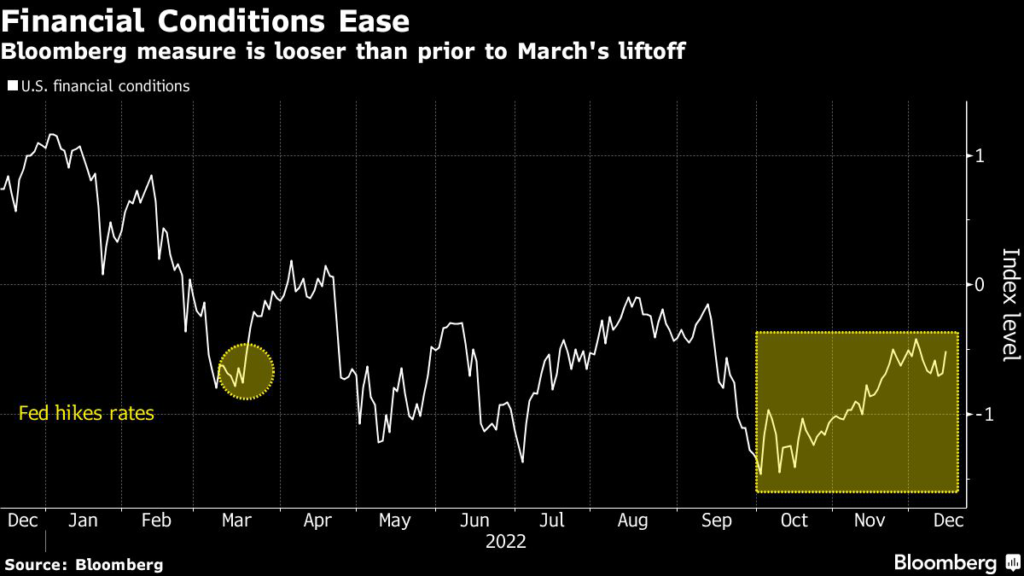

The first question he faced at Wednesday’s news conference was if rallying stocks and bonds posed a problem for policy makers by keeping one of their key levers — financial conditions — too loose.

The S&P 500 jumped after Powell responded that financial conditions had in fact tightened over the course of the year, and in any case the central bank doesn’t worry much about short-term moves.

It was just enough to energize bulls on a day otherwise awash in hawkish messaging.

Earlier in his conference Powell said the Fed isn’t close to ending its campaign of interest-rate increases as officials signaled borrowing costs will head higher than investors expect next year. His Federal Open Market Committee raised its benchmark rate by 50 basis points to a 4.25% to 4.5% target range and policy makers predicted rates would end next year at 5.1%, a higher level than previously indicated.

To be sure, Powell faces a difficult task in communicating any shift in his approach to combating inflation, and volatility in asset markets ran high during his press conference and its aftermath.

The S&P 500 was twice down by as much as 1.3% and twice came close to erasing the decline. Still, for bulls who bid up stocks by almost 7% since the last meeting and were bracing for a sterner bashing, the closing print — down 0.6% — was a victory.

“This is a market that is cherry-picking what it wants to hear,” said Michael Contopoulos, director of fixed income at Richard Bernstein Advisors.

“He basically said buyer beware. ‘We’re hiking more than was generally anticipated. We’re going to stay there for longer than you think. And if you want to buy risk knowing that, that’s fine, but do so at your own peril.’”

A two-month rally in stocks, combined with falling Treasury yields and tightening credit spreads, has loosened financial conditions — a measure of strains across asset classes — to levels just as easy as when the Fed kicked off its hikes in March, threatening to bedevil policy makers’ efforts.

Though Powell stressed that policy makers aren’t concerned with “short-term moves,” the Fed chief acknowledged that financial conditions are the mechanism through which their policy choices touch the economy.

“If markets keep easing financial conditions, the restrictive policy loses its bite,” former Fed Vice Chair Richard Clarida said on Bloomberg Television before the decision.

Wednesday’s decision also delivered Fed official’s latest economic forecasts, which saw 2023’s median growth forecast downgraded to just 0.5% while the unemployment rate next year is seen rising to 4.6% from its current 3.7% level.

Meanwhile, the projection for the Fed’s so-called terminal rate climbed to 5.1% at the end of next year, according to the median forecast, before being cut to 4.1% in 2024.

But the net effect could be that the Fed is forced to raise rates higher than expected and hold them there if the risk-asset rally rolls on, said Wells Fargo Investment Institute’s Sameer Samana.

Powell said as much, warning that he can’t confidently say that the Fed’s peak-rate estimates won’t move higher.

“Another possible read-through could also be that the Fed has to go higher and stay there longer, because of market-based easing of financial conditions,” said Samana, the firm’s senior global market strategist.

“It just seems like markets, after saying for years to not fight the Fed, have decided that it’s now OK, and I just can’t see it ending well.”

–With assistance from Emily Graffeo and Isabelle Lee.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.