The London Metal Exchange will enter 2023 with the smallest available warehouse stockpiles in at least 25 years, setting the stage for future squeezes and spikes if demand turns out stronger than expected.

(Bloomberg) — The London Metal Exchange will enter 2023 with the smallest available warehouse stockpiles in at least 25 years, setting the stage for future squeezes and spikes if demand turns out stronger than expected.

Available inventories of the six main metals traded on the LME plunged by two-thirds in 2022, with aluminum’s 72% decline accounting for the bulk of the drop, while zinc shrank by 90%.

Collectively, inventories not already marked for withdrawal hit the lowest level in data going back to 1997 on Thursday, and finished the year only fractionally higher.

While most of the world’s metal never sees the inside of an LME warehouse, exchange inventory levels are important because every short seller who holds a contract to expiry must deliver physical metal registered in an LME warehouse.

The LME has introduced new rules to allow deferral to prevent future squeezes, but the exemptions come with costly fees.

The tight stockpiles also reflect a tension that has gripped metals markets for much of this year, between constrained supplies on the one hand, and worries about weakening demand due to recessionary threats in the world’s key economies on the other.

For traders on the LME, the dwindling inventories represent another in a litany of headaches following one of the most dramatic years in the exchange’s 145-year history.

The LME is facing regulatory probes and lawsuits over its actions during a runaway short squeeze in the nickel market in March that pushed several LME dealers to the brink of default, and is due to soon publish the results of an independent review into the crisis.

Heading into 2023, a key debate across metals markets is whether a worldwide downturn in industrial activity and rebounding supply will help to replenish the industry’s threadbare reserves, while China’s recent reopening from Covid lockdowns adds further uncertainty.

The debate over the outlook for metals supply and demand is particularly contentious in copper, where some analysts are predicting ongoing deficits while others see the market swinging into a rare and historic period of oversupply.

That’s feeding into a sharp divergence over the outlook for prices, with analysts at Goldman Sachs Group Inc.

predicting copper will hit a record high of $11,000 a ton within 12 months, while BNP Paribas says prices will drop to $6,465 a ton by the middle of next year as the market swings into a huge surplus.

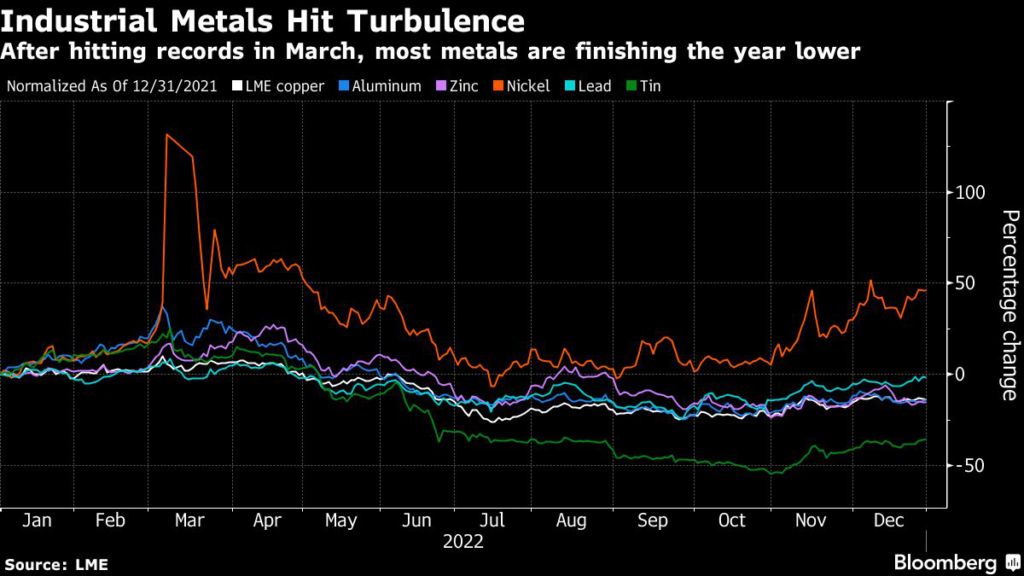

Copper prices fell 0.5% to settle at $8,372 at 5:51 p.m. local time on the LME on Friday, capping the year with a 14% loss, the worst since 2018.

As the year draws to a close, only nickel is trading in positive territory.

The market remains hamstrung by low liquidity since the crisis, with regular sharp swings.

The impact of the historic nickel squeeze has cooled trading activity in other metals, as well, as investors grow concerned about a similar squeeze elsewhere.

As the LME wades through the fallout of this year’s nickel crisis, its American rival is gaining ground.

Chicago-based CME Group Inc. has successful copper and precious-metals contracts but has never managed to challenge the LME’s dominance in other industrial metals. This year, it’s recorded strong growth in its aluminum contracts: aggregate open interest in CME’s Comex aluminum futures contract is up more than 400% since the start of 2022.

Aluminum and zinc on the LME both have their worst year since 2018, with prices down 15% and 16%, respectively.

Tin is the worst performer— prices plunged by more than a third and registered the biggest annual decline since at least 1990.

(Adds nickel details, chart starting in 10th paragraph.)

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.