Investors are intensifying their focus on just when the US government might run up against its statutory borrowing cap as the protracted fight over the House of Representatives speakership raises the risk that lawmakers will fail to agree on how to avoid breaching the ceiling this year.

(Bloomberg) — Investors are intensifying their focus on just when the US government might run up against its statutory borrowing cap as the protracted fight over the House of Representatives speakership raises the risk that lawmakers will fail to agree on how to avoid breaching the ceiling this year.

A failure to lift or suspend the debt ceiling in time could trigger a technical default by the US or encourage credit assessors to downgrade the country’s rating — something Standard & Poor’s did in the wake of a previous debt-cap standoff in 2011.

Given the potential for those kinds of events to upset global financial markets, traders are analyzing when that key date might be.

It’s not a simple calculation, but a number of analysts estimate the drop-dead date, as it’s known, will be some time in the third quarter of 2023.

In an environment where political leaders can reach an actionable agreement, that should leave plenty of time. But the failure of the House to even elect a speaker suggests any accord will be hard-fought.

The current deadlock in the House “almost completely eliminates any chance of it being handled smoothly, which was already pretty low,” said Jefferies LLC economist Thomas Simons.

The debt ceiling already roils markets, particularly the very front end of the fixed-income markets since the short maturities make securities in that part of the curve more susceptible to default.

While Treasury bills show no concerns about the debt limit at the moment, eventually investors will start to avoid the most vulnerable maturities.

That’s because if the US runs out of borrowing capacity, debt maturing immediately afterward might not be repaid on time.

Investors in those securities tend to demand compensation for the risk in the form of higher bill yields. Longer-term bills normally pay higher rates than shorter ones, and that’s still the case for now, though that could change once the market starts to coalesce around the date when the government is likely to exhaust its borrowing authority.

The outgoing Congress, in which the Democratic Party had control of both chambers, opted not to tackle the issue during its lame duck session — the period between the November election of new members and the seating of them in January.

It was instead focused on other legislative priorities for that limited timeframe.

The majority of the new House, meanwhile, is from the Republican Party, which stands in opposition to President Joe Biden.

Analysts had already anticipated that finding a resolution on the debt limit might be difficult under those circumstances. But now they’re girding for a messier outcome amid upheaval that’s seen the GOP’s Kevin McCarthy fail to secure enough votes for the speakership through numerous ballots.

Lawmakers entered a fourth day of voting on Friday.

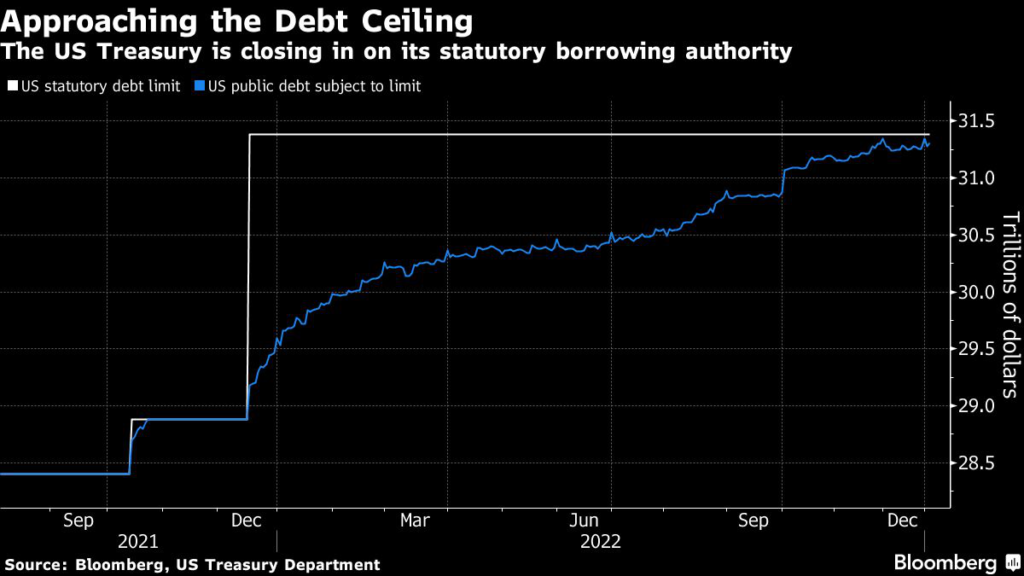

Officially, the government is $78 billion away from reaching the $31.4 trillion statutory limit. But the Treasury has historically employed various extraordinary measures to avoid exceeding the cap as soon as it might otherwise.

These include slashing the amount of Treasury bills it issues, spending down cash it keeps parked at the central bank and suspending payments to government trusts.

Cutoff Date

When and how these measures are enacted — and exactly which ones the Treasury chooses to use — will help determine the final cutoff date.

So too will the flow of government outlays and receipts. The influx of tax money in April is likely to provide a cushion, though with the economic situation and asset values having deteriorated, flows are not expected to be as bountiful last year.

On the flipside, tax refund payments have the potential to accelerate outflows.

The size of bill auctions is another swing factor. The Treasury started shrinking these in late 2022, further delaying the use of its accounting gimmicks to prolong its borrowing authority.

But it’s not a straight path and there is a limit to how low the sale sizes can go, as the Treasury still needs to roll over existing debts and fund government payments.

Strategists from Bank of America Corp., UBS Securities and Wrightson ICAP have identified a drop-dead date some time in the third quarter.

The 2011 Fight

The closest the US has come to the precipice before was in 2011.

Back then, a standoff between the Democratic administration of Barack Obama and the Republican leadership ultimately led S&P to strip the US of its top credit rating. The tradeoff then — and in some subsequent episodes — has been for the ceiling to be raised in exchange for future spending cuts, and there’s a chance that’s how it plays out again.

But this time has the potential to be different.

Many of the same Republican Party holdouts who are currently keeping the speaker’s gavel out of McCarthy’s reach are also spoiling for a fight over the debt limit, demanding party leaders use the threat of default as leverage to force deep spending cuts.

And there’s a risk that concessions McCarthy makes in the effort to become speaker end up circumscribing his ability to push through debt-cap legislation.

An emerging deal that McCarthy is discussing to make him speaker would propose a roughly $75 billion cut in defense and part of the agreement would be to cap spending across government at 2022 levels, according to people familiar with the discussions.

Biden and other Democratic leaders, meanwhile, have adamantly rejected giving in to what they disparage as “hostage taking” with the US economy.

Amid the standstill, California Democrat Brad Sherman on Wednesday floated a potential deal that would trade Democratic votes to make McCarthy the speaker in return for rules aimed at preventing a US government shutdown or a debt-limit crisis.

Yet no matter which way this particular deadlock is resolved, the fact that the chamber is so fractured and so many are potentially hostile to lifting the cap, means the battle is likely to be tough.

“My view in November was this is going to be a mess with GOP in power in the House,” said Blake Gwinn, head of US interest rate strategy at RBC Capital Markets.

“My view now is this is going to be a mess with GOP in power in the House.”

(Updates with news on speakership battle.)

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.