A US services gauge unexpectedly shrank at the end of 2022, with steep declines in measures of business activity and orders that, if sustained, risk heightening concerns about the demand outlook.

(Bloomberg) — A US services gauge unexpectedly shrank at the end of 2022, with steep declines in measures of business activity and orders that, if sustained, risk heightening concerns about the demand outlook.

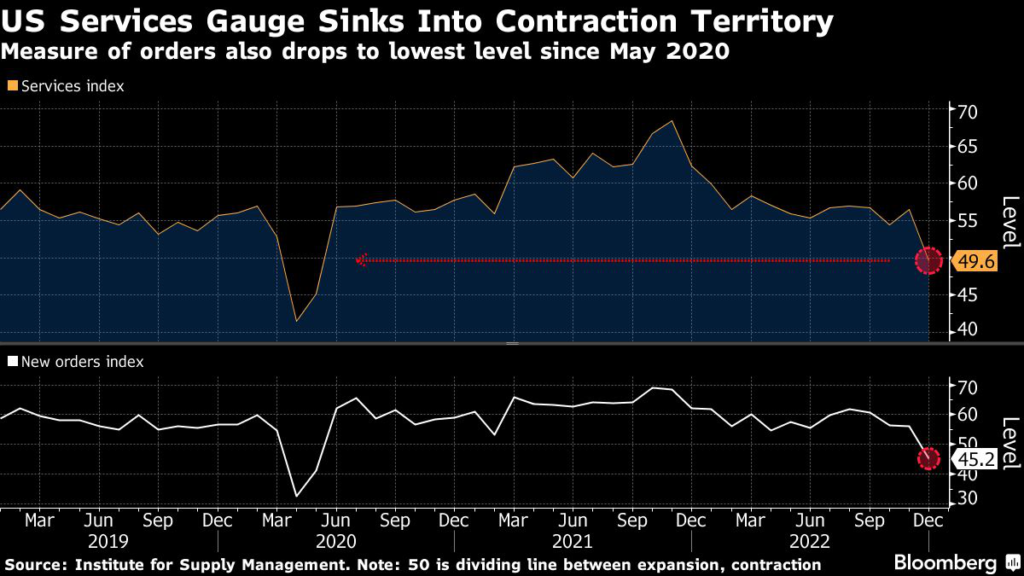

The Institute for Supply Management’s index of services dropped to 49.6 last month, the lowest since May 2020, from 56.5 in November, data released Friday showed.

The figure was below all projections in a Bloomberg survey of economists. Readings below 50 signal contraction.

The nearly 7-point decline from the prior month was the largest since the immediate aftermath of the pandemic.

It may have been impacted by severe winter weather that threw holiday travel into chaos and caused widespread power outages.

While the storm struck at the end of the month, any sustained weakness in the measures would suggest a lack of forward momentum in the economy.

Six industries contracted in December, led by real estate and wholesale trade, the ISM data showed.

The group’s gauge of business activity, which parallels the ISM’s factory output index, slumped 10 points to 54.7 last month.

The orders measure slid even more. Both declines were the largest since April 2020.

The disappointing services reading brings the overall gauge more in line with ISM’s manufacturing data, which showed earlier this week that factory activity contracted for a second month in December.

However, while the factory report showed customer inventories were close to appropriate, the services data suggested that firms viewed their stockpiles as too high.

The inventory sentiment gauge soared nearly 12 points to 55.9, the highest since June 2020. These figures can be volatile on a month-to-month basis.

A measure of prices paid by service providers declined for a second month, to 67.6.

While that’s the lowest in nearly two years, it’s still higher than the long-term average.

Meantime, delivery times improved dramatically. The purchasing managers group’s gauge hit 48.5 in December.

Readings below 50 indicate faster delivery times and last month’s figure was the lowest in seven years, suggesting both a pullback in demand and improving logistics.

Select Industry Comments

“Residential new construction continues to be hindered by higher interest rates, slowing sales dramatically.” – Construction

“We’re dealing with inflation, increasing labor costs, longer lead times and the higher education sector struggling to retain employees.” – Educational Services

“Business conditions for year-end 2022 are good, but not great.

Preparing for a possible recession in 2023, but with some optimism in the overall economy.” Finance & Insurance

“Seeing continual slowing of orders, along with a more receptive supply base.” – Professional, Scientific & Technical Services

“We are optimistic, although concerned, about continued inflation pressures, lead times that remain well above typical and supply chain issues that just won’t go away.

Increasing interest rates are dampening the residential housing construction market, which only adds to the concerns.” – Real Estate, Rental & Leasing

“We are in the busiest season of the year in our business, and inflation is definitely putting the squeeze on our margins.” – Wholesale Trade

The ISM index of services employment dropped below 50 for the second time in the last three months, indicating some industries were reporting a decline in payrolls.

The report highlighted both difficulty backfilling positions and hiring restraint amid ongoing economic uncertainty.

–With assistance from Kristy Scheuble.

(Adds graphic)

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.