(Bloomberg) — Once seen as misguided and unworkable, the US-conceived price cap on Russian crude oil exports is showing signs of success — for now — since it was implemented late last year.

(Bloomberg) — Once seen as misguided and unworkable, the US-conceived price cap on Russian crude oil exports is showing signs of success — for now — since it was implemented late last year.

Moscow’s budget deficit widened to a record amid the slump in prices, with Russian grades falling faster than global prices as supply hasn’t been severely disrupted, the two key aims of the idea that was hatched by the US Treasury Department last year as part of the global response to President Vladimir Putin’s invasion of Ukraine.

“If the goal of Western powers was to have their cake and eat it too, then the cap is presently working as planned,” said Raad Alkadiri, managing director for energy, climate and resources at Eurasia Group in Washington.

“Russian flows have been diverted but not disrupted for the most part, and prices have not risen.”

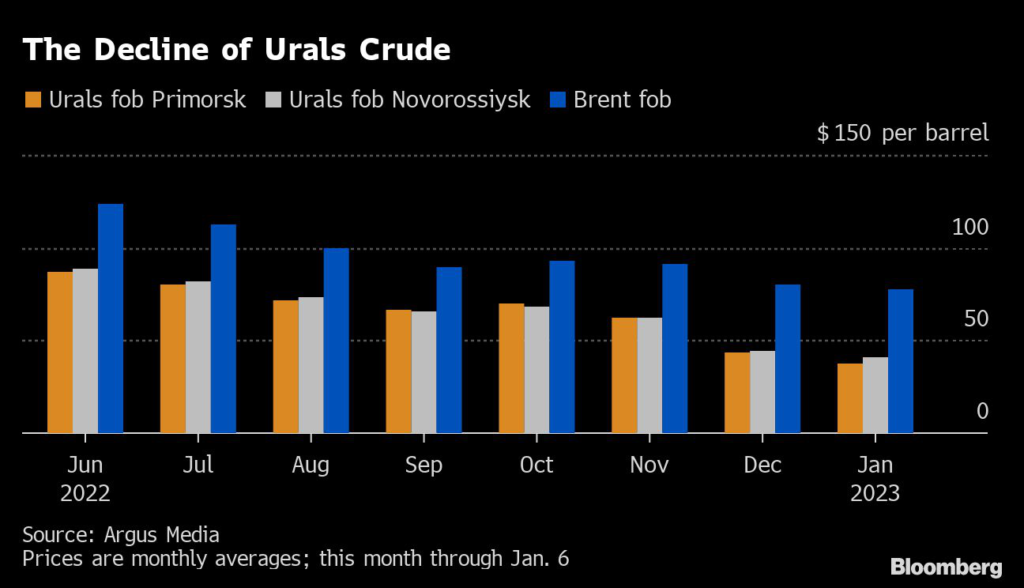

Crude shipments out of two major western Russian ports averaged just under $40 a barrel during the first days of January, according to data from Argus Media, which gathers prices in the physical market.

That’s down more than 35% from the November average and roughly 50% from June.

Over those same periods, Brent crude, a global benchmark, fell about 15% and 37%, respectively. That suggests weaker demand from a slowing global economy can’t fully account for the drop in Russian prices, and its export volume hasn’t slipped enough that lower supply is pushing international prices back the other way.

The US Treasury’s deputy secretary, Wally Adeyemo, said he and his colleagues were pleased with the results, but reacted cautiously when asked if the plan could be declared a success.

“Until the invasion of Ukraine is done, we’re not going to declare anything,” he said in an interview.

The European Union’s decision last June to stop importing almost all seaborne Russian oil from Dec.

5 forced Moscow to look elsewhere to sell about 2 million barrels a day. While it found outlets in China, India and Turkey, that concentrated group of buyers seized upon their leverage to secure deep discounts.

On top of that, Russia has been forced to absorb the extra costs for the longer shipping distances.

“What has hurt Russia is having to swing cargoes from Europe to Asia and be forced to accept the discount,” said Paul Horsnell, head of commodities research at Standard Chartered Bank in London.

“Lack of access to Europe is what has mattered, not the price cap.”

The cap was designed as a way to partly undercut EU sanctions, which the US feared might backfire by cutting supply. In addition to the embargo on Russian oil, the EU and UK barred their companies from offering key services to any shipper carrying Russian oil anywhere in the world, which included insurers who dominate the global market for underwriting oil tankers.

That set off alarm bells in Washington, where US Treasury officials feared the sanctions might trap 2 million to 3 million barrels a day inside Russia, sending global prices spiking well above $100 a barrel.

Officials even worried that higher prices on lower output could end up benefiting Russia while driving the rest of the world into recession.

Against that worst-case scenario, the cap was conceived as a release valve to allow Russia continued access to EU and UK shipping services so long as cargoes were priced under an agreed cap, which was ultimately set at $60.

The US had to charm, plead and bully Group of Seven governments and then the EU into backing the scheme just in time for the Dec.

5 deadline.

To be sure, Russian export volumes fell in the weeks following Dec. 5, but bad weather, port maintenance and a shift by Russia to exporting refined products may explain much of that.

The cap advocates also got lucky.

A cooling global economic outlook combined with the leverage already applied by Russia’s few buyers meant that Moscow was already selling much of its crude below the $60 cap before it even came into effect.

For shipments priced over the cap, mostly coming from Russia’s eastern ports, Russia and its buyers have apparently been able to line up shipping and service providers from outside the EU and UK.

Still, the US and its allies must navigate an uncertain path forward for the cap, beginning with a review of the crude price, which begins in January, and related caps for refined fuels that must be agreed by Feb.

5. Some EU members are already clamoring to tighten the screws on Moscow by lowering the crude cap, but squeezing too hard risks pushing Putin to cut production in an attempt to provoke a price spike the US has always sought to avoid.

Any change to the cap would require a unanimous vote by the EU’s 27 member governments, according to an EU official.

Adeyemo wouldn’t comment on whether the US will want to adjust the cap.

While one aim of the cap, he said, is to reduce Moscow’s revenue, the US also wants to make sure Russia has a continued incentive to export its oil.

“We feel at the moment the $60 amount that we’ve set is accomplishing our two goals,” he said.

–With assistance from Grant Smith, Alex Longley, Alaric Nightingale and Kevin Whitelaw.

(Updates with EU procedure for adjusting price cap from 17th paragraph.)

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.