If the Bank of Japan sticks with its yield-curve control policy and liquidity continues to worsen, AllianceBernstein Holding LP says it may be time to consider stopping investing in the country’s government bonds altogether.

(Bloomberg) — If the Bank of Japan sticks with its yield-curve control policy and liquidity continues to worsen, AllianceBernstein Holding LP says it may be time to consider stopping investing in the country’s government bonds altogether.

Traders are positioning before the BOJ’s two-day meeting ends on Wednesday and Yusuke Hashimoto, a Tokyo-based fixed-income portfolio manager, is mulling the future for Japanese sovereign-debt investments should policy makers show signs of digging in with continued bond buying and a cap on yields.

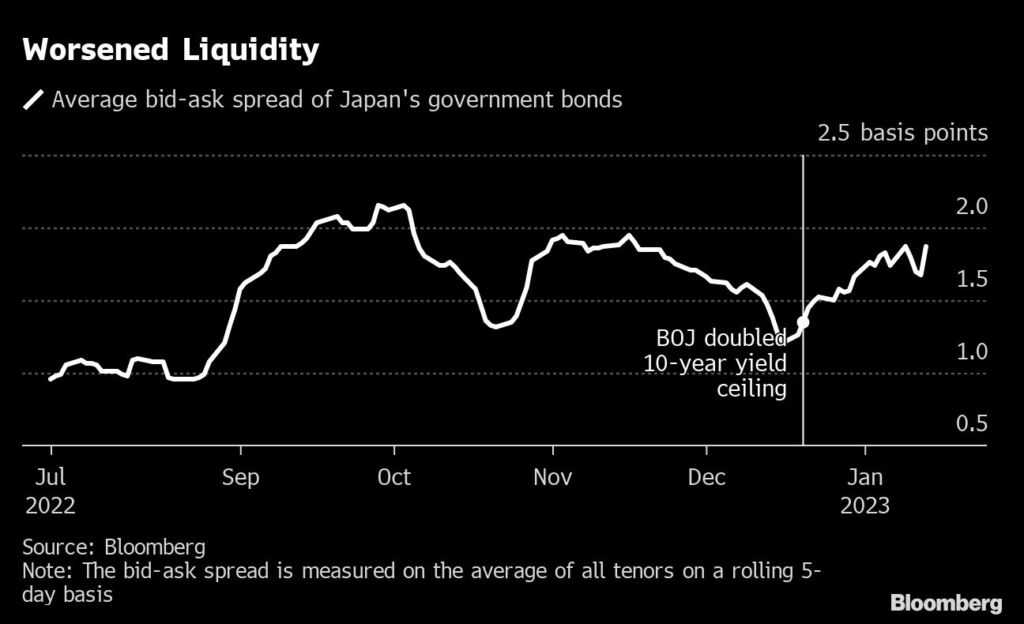

“A significant decrease in liquidity in the world’s second-largest government bond market raises the question as to whether it will remain a market that justifies exposure for investors,” Hashimoto said in an interview.

“We may have to exclude Japanese government bonds from our investment in the future,” if liquidity declines further.

Investors are increasingly betting the central bank will abandon its stimulus framework as soon as this week after inflation in Tokyo hit the fastest pace in four decades and the BOJ’s shock move last month to raise its ceiling yield movements failed to breath life into Japan’s dysfunctional debt market.

While almost all economists surveyed by Bloomberg expect no change in policy at the meeting, an unusually high number of BOJ watchers say they can’t rule out the possibility of another adjustment in the central bank’s yield curve control program.

Traders’ bets on another policy shift drove the Japanese 10-year bond yield above the central bank’s 0.5% ceiling on Tuesday.

BOJ Meets Amid Intense Speculation Over More Tweaks: Day Guide

For now, Hashimoto says he’s able to trade as normal.

Policy makers have two options this week, he said — either they abolish yield-curve control and allow the market to normalize, or they extend the term of zero-interest loans to five years from two years so that banks will be encouraged to buy intermediate government debt.

That would help ease selling pressure on government debt at least until the regulator’s March meeting.

BOJ Opens ‘Pandora’s Box’ for Traders on Alert for Another Shock

When the yield policy is finally scrapped, Hashimoto sees the yield on 10-year government debt surging to 0.9% from its current cap of 0.5%.

That would make it more attractive for Japanese investors to remain in their home market, and possibly prompt them to repatriate funds from as far away as Sydney, he said.

“We’re mindful” of a negative impact on Australia’s government bonds from any change in the BOJ’s policy, he said.

“A rise in local yields will negate the need for Japanese investors to take risks and buy foreign bonds.”

–With assistance from Matthew Burgess and Masaki Kondo.

(Adds line on JGB yields in sixth paragraph.)

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.