US stocks ended January with a gain, as investors cheered signs of labor costs easing and inflation cooling as they gear up for Wednesday’s Federal Reserve decision.

Traders continued to grapple with earnings after the stock market closed.

(Bloomberg) — US stocks ended January with a gain, as investors cheered signs of labor costs easing and inflation cooling as they gear up for Wednesday’s Federal Reserve decision.

Traders continued to grapple with earnings after the stock market closed.

The Invesco QQQ Trust, a $153.6 billion exchange-traded fund tracking the tech-heavy Nasdaq 100, dropped in postmarket trading after Electronic Arts Inc.

gave a forecast for net bookings that fell short of analysts’ estimates. Snap Inc. also fell after forecasting its first-ever quarterly revenue decline.

However, Advanced Micro Devices Inc.’s better-than-expected sales forecast for the first quarter could still buoy tech shares, as investors brace for reports from Meta Platforms Inc.

and Apple Inc. this week.

The S&P 500 still had its best month since October, as traders expect the Fed to slow its pace of interest-rate hikes. The Nasdaq 100 rallied the most this month since July.

Treasuries gained, with the 10-year yield sliding to around 3.51%. It fell more than 30 basis points during January, the most since November. A dollar index dropped.

Investors are grappling with a flurry of economic data, earnings and rate decisions this week.

Data on Tuesday showed prices in US housing market continued to cool, while another report highlighted consumer confidence unexpectedly falling. Hanging over everything is Wednesday’s Fed decision, with the central bank widely expected to raise rates by a quarter percentage point.

While Tuesday’s data from the Labor Department added to evidence that wage growth is slowing, it may still not be enough to sway the Fed.

Investors will be watching for the tone officials set for future meetings. While Fed Chair Jerome Powell has repeatedly pushed back against hopes of rate cuts later this year, central bank officials could consider pausing rate hikes after their March meeting.

But the recent rally in stocks and bonds does not help the Fed’s bid to tighten financial conditions, said Jeff Muhlenkamp, portfolio manager at Muhlenkamp & Co.

Speaking about Powell’s presser Wednesday, he said “I expect that he will continue to try to talk the market into doing something that it is not currently doing.”

Investors also assessed a bevy of earnings reports on Tuesday.

Shares of McDonald’s Corp. declined and those of Caterpillar Inc. fell the most since Sept. 23 after earnings misses. Meanwhile, General Motors Co. rose after posting upbeat forecasts. Exxon Mobil Corp.’s fourth quarter earnings per share beat estimates and the firm posted full-year profit that was the highest on record.

Now that investors have had a chance to parse a slew of economic reports and earnings results to start the year — with much of it coming in as expected — they’re focusing on what the Fed might do in the latter half of 2023, says Shawn Cruz, head trading strategist at TD Ameritrade.

“So I think we know where our baseline is now and what’s driving markets is Fed policy going into the second half of this year,” he said in an interview.

Key events this week:

- Eurozone Manufacturing PMI, CPI, unemployment, Wednesday

- US construction spending, ISM Manufacturing, light vehicle sales, Wednesday

- FOMC rate decision, Fed Chair Jerome Powell press conference, Wednesday

- Earnings Wednesday include: Meta Platforms and Peloton Interactive

- Eurozone ECB rate decision, President Christine Lagarde press conference, Thursday

- UK BOE rate decision, Thursday

- US factory orders, initial jobless claims, US durable goods, Thursday

- Earnings Thursday include: Alphabet, Apple, Amazon, Qualcomm and Deutsche Bank and Santander

- Eurozone S&P Global Eurozone Services PMI, PPI, Friday

- US unemployment, nonfarm payrolls, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 rose 1.5% as of 4 p.m.

New York time

- The Nasdaq 100 rose 1.6%

- The Dow Jones Industrial Average rose 1.1%

- The MSCI World index fell 0.9%

Currencies

- The Bloomberg Dollar Spot Index fell 0.2%

- The euro rose 0.2% to $1.0872

- The British pound fell 0.2% to $1.2328

- The Japanese yen rose 0.2% to 130.16 per dollar

Cryptocurrencies

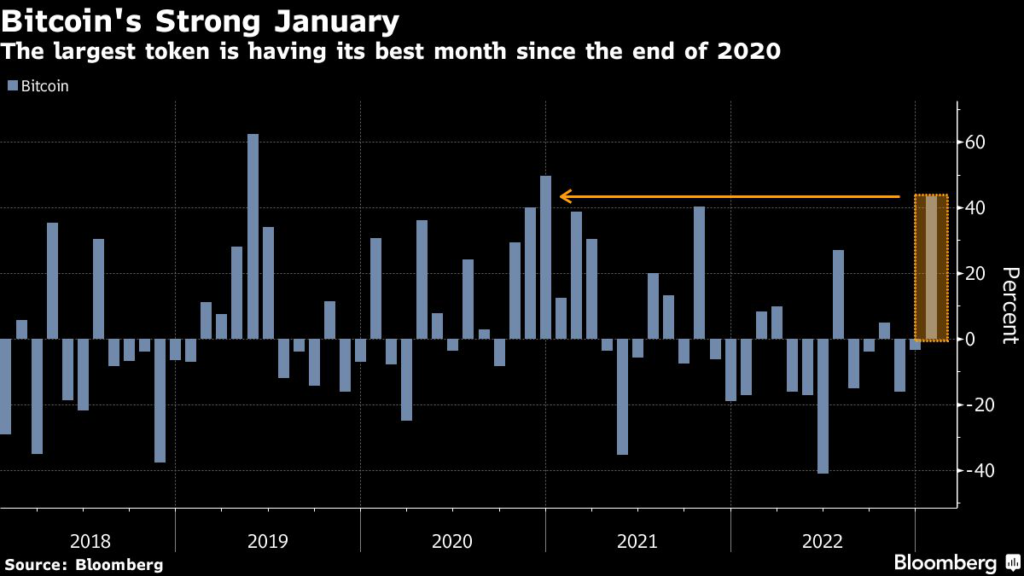

- Bitcoin rose 1.5% to $23,090.48

- Ether rose 1.9% to $1,586.45

Bonds

- The yield on 10-year Treasuries declined five basis points to 3.49%

- Germany’s 10-year yield declined three basis points to 2.29%

- Britain’s 10-year yield was little changed at 3.33%

Commodities

- West Texas Intermediate crude rose 1.5% to $79.03 a barrel

- Gold futures rose 0.2% to $1,943.10 an ounce

This story was produced with the assistance of Bloomberg Automation.

–With assistance from Isabelle Lee, Cristin Flanagan and Alyce Andres.

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.