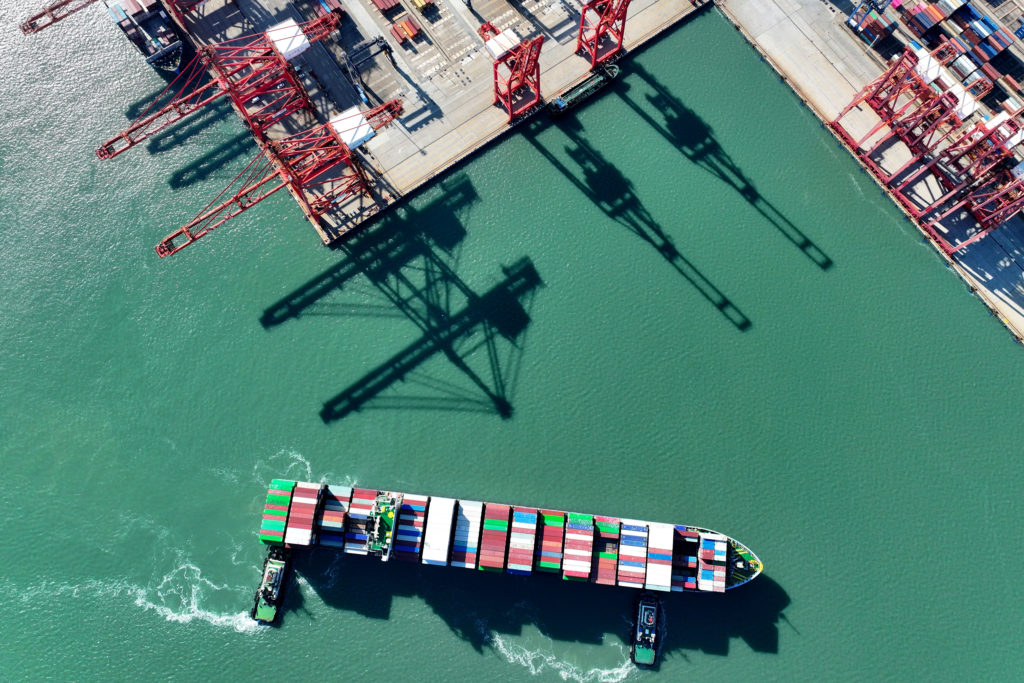

China’s economy grows 5.2% on trade war truce

China’s economy expanded more than five percent in the second quarter of the year, official data showed on Tuesday, after analysts predicted strong exports would provide crucial support despite trade war pressures.The country’s leadership is fighting a multi-front battle to sustain growth, a challenge made more difficult by Donald Trump’s tariff campaign.The US president has …