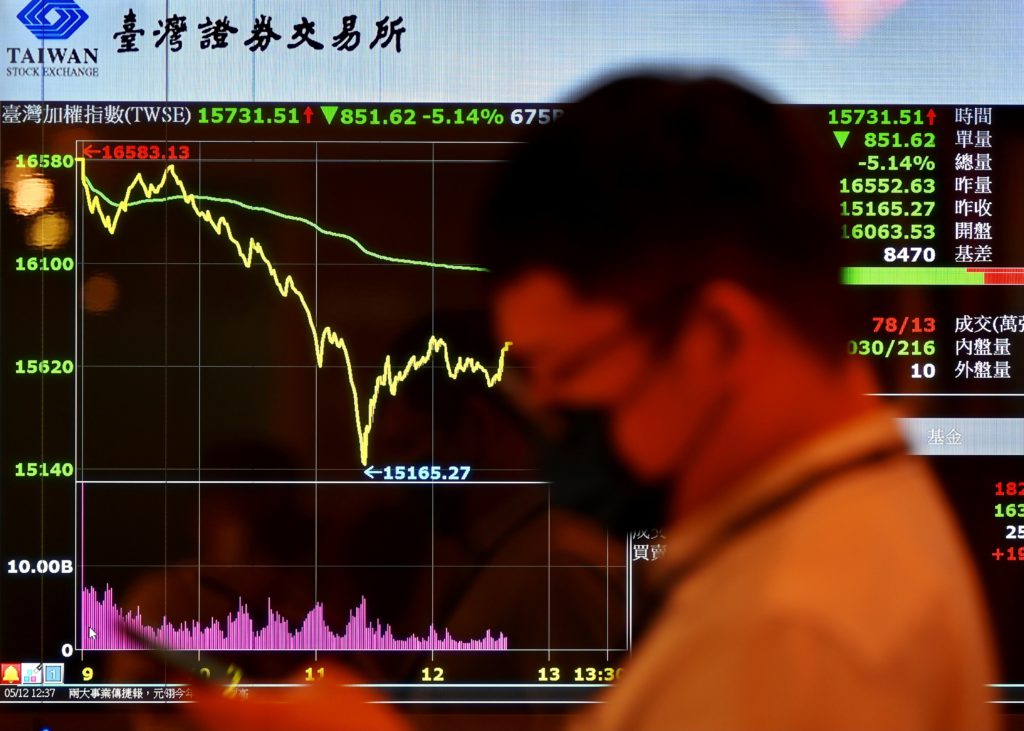

Asian markets stage mild rebound but Trump tariff uncertainty reigns

Asian markets battled Tuesday to recover from the previous day’s tariff-fuelled collapse, though Donald Trump’s warning of more measures against China and Beijing’s vow to fight “to the end” raised concerns the trade war could worsen.Equities across the world have been hammered since the US president unveiled sweeping levies against friend and foe, upending trading …

Asian markets stage mild rebound but Trump tariff uncertainty reigns Read More »