Trump says new tariff deadline ‘not 100 percent firm’

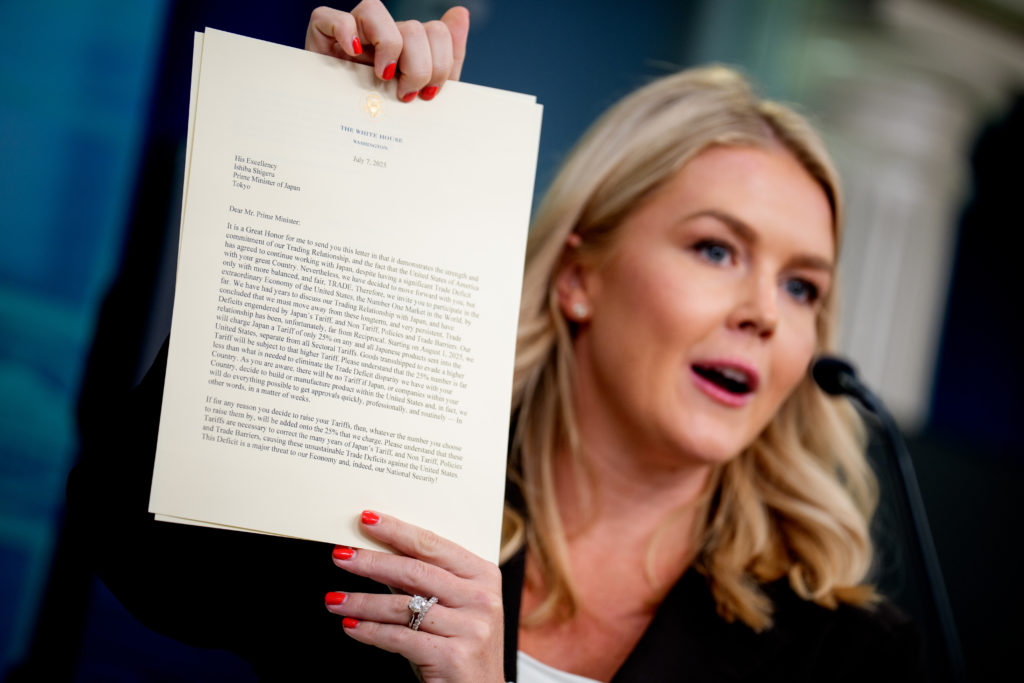

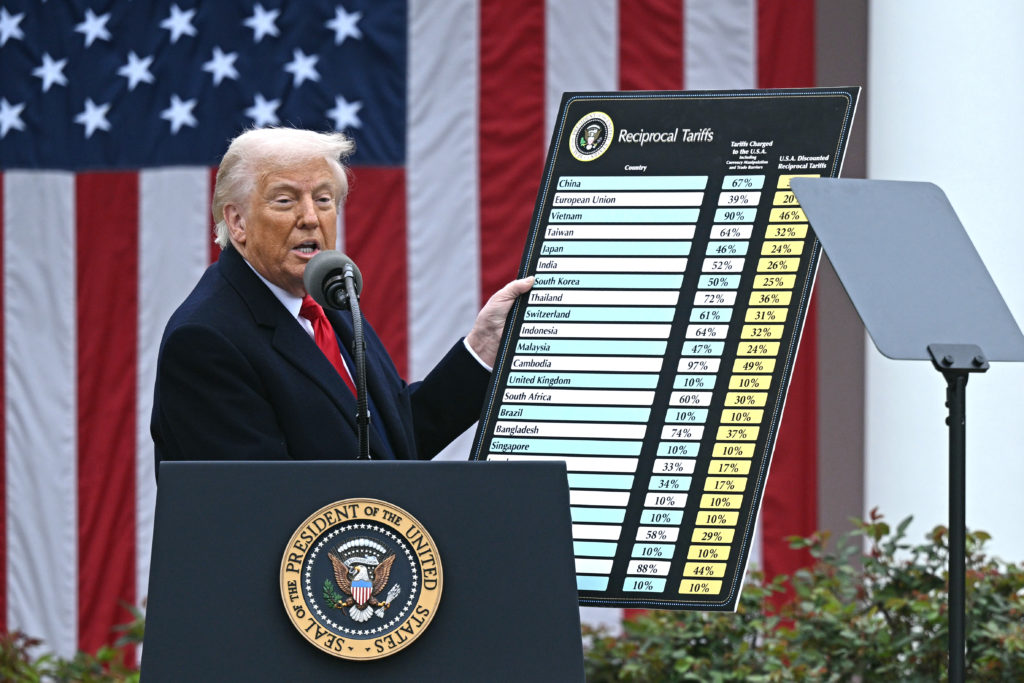

US President Donald Trump reignited his trade war by threatening more than a dozen countries with higher tariffs Monday — but then said he may be flexible on his new August deadline to reach deals.Trump sent letters to trading partners including key US allies Japan and South Korea, announcing that duties he had suspended in …

Trump says new tariff deadline ‘not 100 percent firm’ Read More »