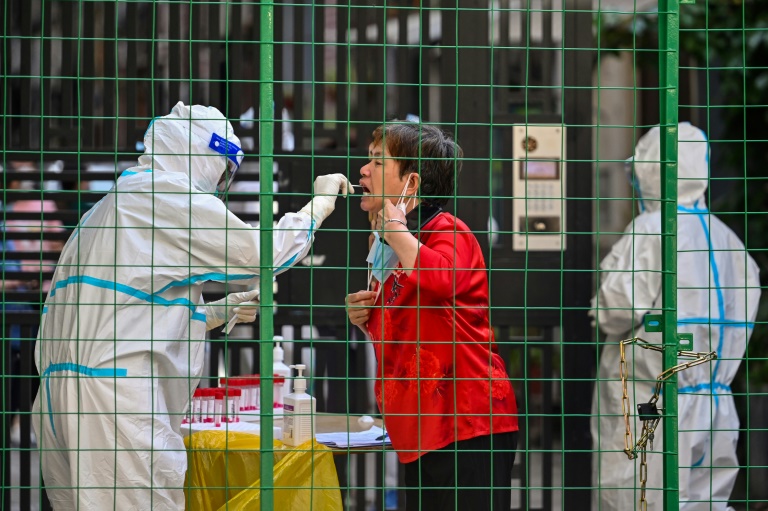

Stock markets climbed Tuesday and oil prices rallied further as China slashed the quarantine time for visitors, fuelling hopes of recovery for the world’s second largest economy.

The news came as Beijing and Shanghai appeared to have contained a Covid outbreak that had forced officials to impose lockdowns that compounded global supply chain snarls, further pushing up inflation.

Authorities said inbound travellers would have to quarantine for only 10 days instead of three weeks.

The news boosted share prices, already striving to rebound from recent sharp losses triggered by fears of a global recession.

“The Covid crisis appears to be rapidly retreating in China,” noted Susannah Streeter, senior investment and markets analyst at Hargreaves Lansdown.

“The prospects of rapid recovery for the world’s second largest economy is helping lift miners, as metals prices rise in expectation of a surge in demand in the commodity-hungry economy.”

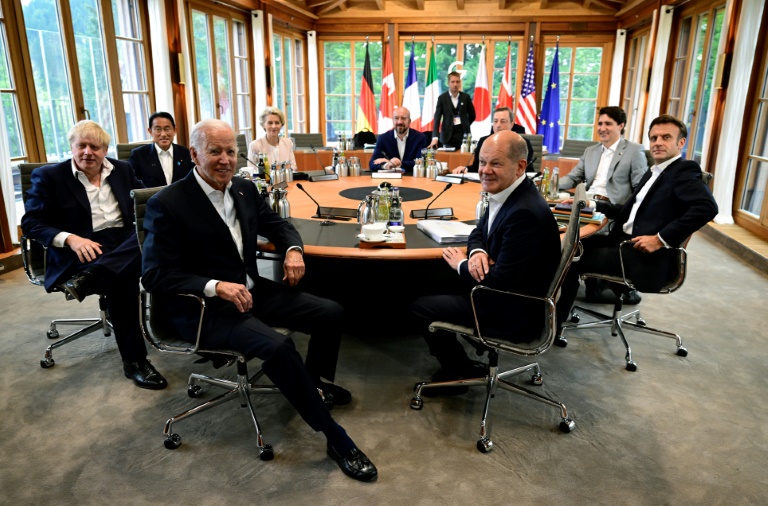

At the same time, G7 leaders meeting in Germany condemned China’s “non-transparent and market-distorting” international trade practices in an end-of-summit statement that hit out directly at Beijing for the first time.

Traders also digested comments from European Central Bank President Christine Lagarde, who said the ECB would go “as far as necessary” to fight inflation that is set to remain “undesirably high”.

Ben Laidler, a global markets strategist at online trading platform eToro, said current economic weakness had been largely factored in by dealers.

“Much is already discounted by markets, which may be in ‘bad news is good news’ mode, as a slowdown cools inflation and interest rate fears,” he said.

Global equity markets are recovering ground as investors believe central banks could decide to raise interest rates by more modest amounts than previously thought.

The US Federal Reserve and its peers are hiking borrowing costs in an attempt to cool inflation, which has soared around the world to the highest levels in decades.

However, such action has increased the prospect of a global recession, causing economists to think that future rate hikes could be less steep than in recent months.

“Wall Street seems to be close to figuring out how high central banks may take rates over in the short-term and that is supportive for long-term investors to scale into positions,” said market analyst Edward Moya at OANDA trading platform.

Wall Street stocks opened higher, with the Dow adding 0.6 percent.

Europe’s main indices were higher in afternoon trading, with London and Paris both rising 1.1 percent, while Frankfurt added 0.8 percent.

Asian markets closed higher.

– Oil jumps as G7 targets Russia –

Oil prices, a major driver of the soaring inflation, rose on fears of further supply tightening, in addition to prospects for higher Chinese demand.

This comes after G7 leaders agreed to work on a price cap for Russian oil, a US official said Tuesday, as part of efforts to cut the Kremlin’s revenues.

International sanctions placed on Russia following its invasion of Ukraine are taking their toll.

Moody’s ratings agency has confirmed that Russia defaulted on its foreign debt for the first time in a century, after bond holders did not receive $100 million in interest payments.

– Key figures at around 1330 GMT –

London – FTSE 100: UP 1.1 percent at 7,336.93 points

Frankfurt – DAX: UP 0.8 percent at 13,292.26

Paris – CAC 40: UP 1.1 percent at 6,115.94

EURO STOXX 50: UP 0.6 percent at 3,519.16

New York – Dow: UP 0.6 percent at 31,636.49

Tokyo – Nikkei 225: UP 0.7 percent at 27,049.47 (close)

Hong Kong – Hang Seng Index: UP 0.9 percent at 22,418.97 (close)

Shanghai – Composite: UP 0.9 percent at 3,409.21 (close)

Brent North Sea crude: UP 1.4 percent at $112.57 per barrel

West Texas Intermediate: UP 1.1 percent at $110.77 per barrel

Euro/dollar: DOWN at $1.0533 from $1.0583 Monday

Pound/dollar: DOWN at $1.2219 from $1.2268

Euro/pound: DOWN at 86.20 pence from 86.24 pence

Dollar/yen: UP at 136.19 yen from 135.48 yen

burs-rl/lth