Most markets rose Monday on hopes the Federal Reserve would soon slow its pace of interest rate hikes, though the mood was darkened by worries over the China outlook after President Xi Jinping tightened his grip on power.

The yen weakened against the dollar after a short rally as speculation swirled that Japanese authorities had stepped into forex markets again to support their currency for a second time in as many sessions.

Tokyo, Sydney, Seoul and Taipei led gains after a strong performance in New York that was sparked by a report the Fed could begin to take its foot off the pedal in its rate hike campaign.

The Wall Street Journal said some officials were keen to discuss a slowdown when they meet next month.

Markets have been hammered this year by fears that moves by the Fed and other central banks to fight decades-high inflation will spark a recession.

Officials had been expected to lift rates 75 basis points for a fourth successive time next month, while bets were increasing on another such move in December.

“The mere suggestion of the Fed stepping down from 75 basis points to a 50 basis point incremental rate hike in December produced a fierce rally in US equities, partial reversal of the recent surge in US Treasury yields and smart about-turn in the US dollar,” said National Australia Bank’s Ray Attrill.

But while most equity markets across the region were well up, Chinese markets were hammered by the reshuffle at the top of government. Hong Kong fell more than six percent and Shanghai was two percent down.

– Zero-Covid worries –

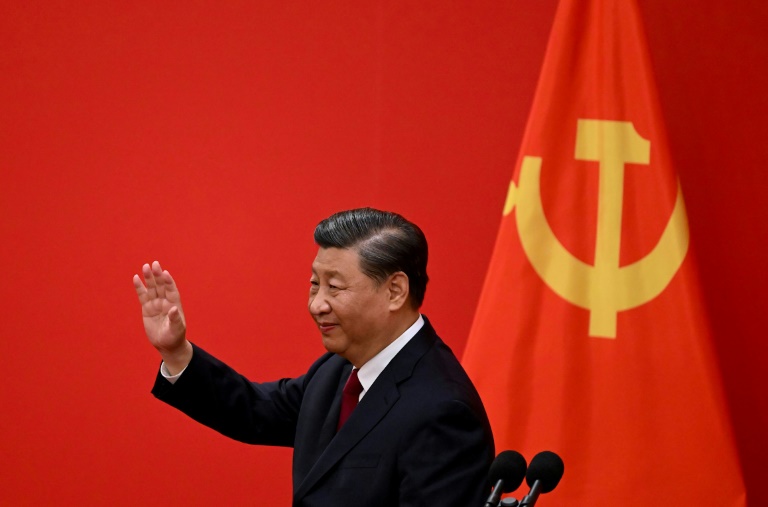

Xi, who was at the weekend given a third five-year term as leader, handed key positions to loyalists who back his strategy of fighting Covid outbreaks with lockdowns and other strict measures.

The policy has been blamed for the sharp drop in growth in the world’s number two economy, and while data showed Monday that it expanded more than forecast in the third quarter, traders remain on edge.

In a speech to close the Congress on Saturday, Xi insisted his zero-Covid policy had been a success.

And he promoted Li Qiang, the architect of a two-month lockdown in Shanghai that crippled the financial hub’s economy, to the second most powerful post in the Communist Party.

“The market is concerned that with so many Xi supporters elected, Xi’s unfettered ability to enact policies that are not market friendly is now cemented,” Justin Tang of United First Partners said.

Tech firms were among the worst hit in the Hong Kong selloff, hammered in recent years by Xi’s crackdown on the sector that has scythed firms’ profits and wiped billions off their valuations.

E-commerce giants Alibaba and JD.com each saw double-digit losses, as did Tencent. The Hang Seng tech index was close to 10 percent down.

The onshore yuan dipped as much as 0.4 percent to 7.2552 to the dollar — its weakest since January 2008.

Investor worries about China also weighed on oil markets with both main contracts in retreat as the prospect of more possible lockdowns hitting demand expectations.

On currency markets, the yen was hovering just above 149 to the dollar, having strengthened to 145.65 earlier amid talk that authorities had intervened to support the unit.

Observers said officials likely stepped in on Friday after the dollar soared to a fresh 32-year high of 151.93 yen. That came after warnings from the finance ministry that it was keeping tabs on movements, and follows a similar move last month.

“Whilst the (finance ministry) has since declined to comment on whether they intervened, such action has not come without multiple warnings from officials,” said Matt Simpson at City Index.

“The MoF last week said they will deal with speculators ‘severely’ and the strong price reaction on Friday suggests they did just that.

“Price action has also been erratic in Monday’s Asian session, which points to another probable intervention.”

The pound rose after former UK prime minister Boris Johnson said he would not stand for the Conservative leadership again, after the resignation of Liz Truss last week.

His decision leaves his former finance minister Rishi Sunak the favourite to take the reins and become the country’s third premier this year.

The choice of the less-controversial Sunak could provide a little stability in Westminster after weeks of turmoil sparked by Truss’s debt-fuelled mini-budget that hammered the pound and sent shivers through markets.

London slipped in the morning, though Paris and Frankfurt rose even as data showed further weakness in the eurozone economy.

– Key figures around 0810 GMT –

Tokyo – Nikkei 225: UP 0.3 percent at 26,974.90 (close)

Hong Kong – Hang Seng Index: DOWN 6.4 percent at 15,180.69 (close)

Shanghai – Composite: DOWN 2.0 percent at 2,977.56 (close)

London – FTSE 100: DOWN 0.3 percent at 6,946.36

Pound/dollar: UP at $1.1330 from $1.1258 on Friday

Dollar/yen: UP at 149.15 yen from 147.65 yen

Euro/dollar: DOWN at $0.9841 from $0.9863

Euro/pound: DOWN at 86.88 pence from 87.26 pence

West Texas Intermediate: DOWN 1.5 percent at $83.81 per barrel

Brent North Sea crude: DOWN 1.3 percent at $92.27 per barrel

New York – Dow: UP 2.5 percent at 31,082.56 (close)