(Bloomberg) — At the once-every-five-year Communist Party congress this month, where President Xi Jinping is set to secure rule until at least 2027, policies on the table will help determine how quickly China surpasses the US economy, or whether it ever will.

Bloomberg Economics has sketched out four scenarios for China’s economy over the decades ahead, with a base case of 4.6% growth on average over the next decade. Their model suggests a growth rate above 5% over that time period — as predicted pre-pandemic — is now out of reach, due to the lasting impact of Covid Zero policies, a faster decline in fertility than previously expected and lower investment due to a gradually shrinking real estate sector.

If the property downturn is deeper than expected and Covid Zero restrictions remain beyond 2023, GDP growth may average below 4% over the next decade, meaning China likely wouldn’t overtake the US until the mid-2030s, and any lead may be reversed as demographics become a drag a decade later.

If China can shake off those twin constraints, continues to invest in manufacturing, and its educated workforce boosts productivity, an expansion rate above 5% becomes achievable once more, leading to a swifter ascent to No. 1.

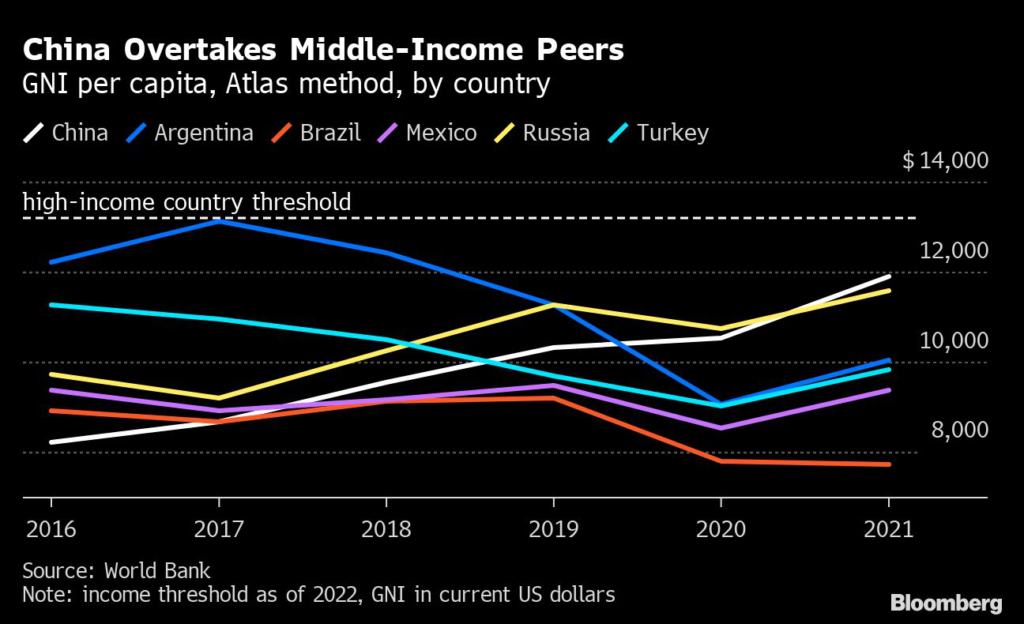

Judging by Xi’s longer-term record, it would be risky to bet he can’t pull it off. The size of China’s economy has more than doubled since 2010. When Xi took over in 2012, economists were discussing if China could be stuck in the “middle income trap.” But China’s per capita income has overtaken middle-income peers like Argentina and Russia since then, reaching the cusp of what the World Bank defines as “high income” status.

The reforms won’t be easy. Xi will need to push up the retirement age, increase taxes on the wealthy to fund better education and healthcare, and overcome resistance from local governments who don’t want to provide public services to migrants from other parts of China. The vast financial sector needs a shake up to ensure funds go to the most productive firms, and private companies, which employ most of the country’s workers, need to be allowed to compete more evenly with state-owned rivals.

Drawing on analysis from Bloomberg Economics’s Chang Shu and Eric Zhu, here’s a look at four scenarios for China’s economic growth over the decade ahead.Base case: A decade of growth between 4 and 5%

The Covid Zero policy is hammering China’s economy, leading some economists to lower GDP forecasts for this year to below 3%. So long as the policy continues, there’s little chance of significant improvement.

Government experts in China have said the policy can be relaxed when there are enough medical tools including treatments and second-generation vaccines available. Bloomberg Economics’ base case assumes gradual loosening from the second quarter of 2023.

China’s demographic challenge is also a constraint, with the population decline happening earlier than previously forecast. But it’s workforce size that matters for economic output, and the population is living longer — life expectancy now exceeds the US — so they can work longer too.

While China’s retirement age is currently 50 to 60 depending on gender and profession, if that is raised gradually to 65 over the next decade, the workforce can remain roughly stable at around 760 million workers over that period.

As countries get richer, workers skills — or “human capital” — becomes key to their productivity, offering China an economic offset to the looming population decline. New entrants to the workforce are far more educated than their predecessors: China will produce more than 10 million college graduates this year, nearly double the number a decade ago.

“There is an education tsunami coming to China,” says Bert Hofman, former China country director at the World Bank and now head of the East Asian Institute in Singapore.

It’s not all about universities. The share of 25 to 60-year-olds with a high-school education has risen to 37% and is on track to reach at least 50% by the end of this decade — moving closer to levels seen in countries like Portugal — if Beijing can continue to boost education spending.

There’s still considerable growth to be had from investment. China invests a higher proportion of GDP than any major country in recent history, and while much of that doesn’t produce high returns, the overall return on investment — whether in housing, infrastructure or manufacturing — remains in positive territory, while the return on assets in China’s industrial sector is still about 6% on average. One example: Electric vehicle plants backed by governments and built by companies such as BYD and Nio have made China a world leader in that emerging industry.“Even if you waste some of it, you still get growth from capital,” says Hofman. He calculates that even with a bare minimum of economic reforms, China could grow 3% annually through to 2035 just from its physical investment.

To achieve that, China will need to maintain its current high household savings rate, but allocate those funds more to manufacturing and service companies than real estate firms.

The property market’s ongoing malaise has been the other major brake on growth. The base case scenario sees an ongoing gradual decline in real estate investment — which is needed to align supply with demand — but no collapse. The real estate slowdown frees up resources to be invested in more productive areas.

And even though China’s unprecedented home building boom is now in the past, there’s still fundamental demand for housing. China’s urbanization rate — currently comparable to where the US was in the 1950s — still has room to grow, with an estimated 10 million people set to move to cities each year through to 2025. That process in turn boosts productivity, as workers in cities find it easier to match their skills with other workers.

China’s economy is now too large for foreign demand to drive it via export growth. Beijing needs reforms to ensure that Chinese companies can take advantage of a huge domestic market and consumer spending continues to grow. That’s where Xi’s signature policies “ dual circulation” and “ common prosperity” come in. The first is about breaking down economic barriers between China’s provinces. The second is about making sure more investment goes to poorer regions and making provision of healthcare more equal — likely requiring higher taxes on the wealthy.

In Bloomberg Economics’ model, the biggest contributor to growth over the next decade is total factor productivity, referring to changes which allow labor and physical investment to be used more effectively. One of those things is the adoption of new technology.

It’s hard to make predictions about that, but proxies such as spending on research and development, scientific publications, and patents have all shown strong growth. China now spends more of its GDP on R&D than many European countries.

Another boost will come as workers shift from jobs producing lower-value to higher-value goods and services. One area for upside: The share of workers in agriculture still has room to fall from around 25% today to somewhere closer to the 3% average in advanced economies. Companies like TikTok owner ByteDance Ltd. have helped farmers become live streamers.

There have also been big changes in market institutions under Xi, reducing barriers on how people can sell their labor, ownership in companies, as well as goods and services they produce. To take two examples: Since 2020, Chinese people have become entitled to buy housing and claim government benefits in any city with a population below 3 million — with the policy now gradually extending to larger cities. The amount private firms raised on Chinese stock markets has soared in recent years. The base case expects such reforms to continue.

Beijing’s regulatory crackdown on the likes of Alibaba and Tencent over recent years shows it’s wary of private firms which grow too large. Still, Xi wants a vibrant private sector, with the government rolling out policies to make it easier for small and medium-sized companies to receive loans, cutting business taxes and reducing red-tape. Beijing is supporting thousands of “little giant” start ups with funds and tax breaks, tilted toward firms that file patents outside of China.

“The key unknown is whether the party’s efforts to support its favored parts of the private sector can spur enough growth to outweigh the negative effects of its crackdown on other, less favored areas,” says Chang-Tai Hsieh, an economist at the University of Chicago.

China’s private-sector companies are generally more productive than their state-owned rivals due to the large number of poorly performing local government-owned enterprises, and Beijing’s reliance on the state sector to support growth during the pandemic has made the playing field “less even,” according to Margit Molnar, head of the Organisation for Economic Co-operation and Development’s China desk. But while Xi supports SOEs in sectors he sees as strategic for the economy, he’s also allowed locally owned state firms in non-strategic sectors to go bankrupt at unprecedented rates.

Eliminating majority state-ownership in non-strategic sectors such as hotels, catering, retail and wholesale would boost long-term GDP per capita by 1.3%, according to the OECD. “There are so many areas where reforms could bring about a boost to productivity,” says Molnar.

Bloomberg Economics’ base case incorporates a gradual decoupling from the US, with links never returning to their pre-pandemic levels. But politicians in both Europe and East Asia stress that decoupling from China is not their goal, meaning ongoing exchanges with advanced economies across the globe will remain as a growth driver.

As GDP levels are compared in US dollar terms, China’s race to number one status will be influenced by what happens to exchange rates. If China continues to open up its vast financial markets to overseas investors, a strengthening in its currency will help propel its rise.

Bear case: Slower than 4%

China’s leadership has been vague on when the Covid Zero policy will end. In a downside scenario, it isn’t relaxed until 2024, meaning at least another year of very low growth, with a long-term impact on productivity as unemployed workers miss chances to accumulate skills.

Pushback to pension reforms (even authoritarian governments like Russia’s have had to U-turn over raising the pension age) could mean the process isn’t finished until 2040, and the working-age population declines markedly over the decade as a result.

The property market slowdown — if mishandled — could lead to an even sharper slowdown in investment. In a nightmare scenario for Beijing, the drop in investment might take place rapidly, shrinking by 20% over 2022-2024. Another scenario is that the government overstimulates and as the policy support is withdrawn, a worse downturn occurs, turbo-charged by an even larger overhang of housing supply.

Any sudden decoupling from the US, if it imposes anything close to Russia-type sanctions on China, would be disastrous for China’s growth. While the blowback for the world would probably be too great for Washington to go that far, more aggressive decoupling — for example, Huawei-like curbs on all of China’s tech firms — would hit growth further.

The nightmare scenario: Sub 3% growth

Xi’s top priority over the past five years has been an effort to reduce the chance of a financial crisis by choking off shadow banking and slowing debt growth. But there are still many non-performing loans in the banking system, and if housing prices crash and too many banks or local governments need bailouts, growth could slow even more.

Things could get even worse if US allies join in on decoupling efforts. China’s output could be up to 8% smaller by 2030 if there’s strong decoupling from OECD economies versus a no decoupling scenario, according to International Monetary Fund analysis.

Another pandemic or climate change-related extreme weather could damage the economy severely. And a clash over Taiwan would also be disastrous.

An article by an anonymous analyst that was viewed more than 100,000 times on Chinese social media assessed China’s growth prospects to 2030, and highlighted Taiwan declaring independence and triggering an invasion by mainland forces as the “biggest external risk in the next decade.” The article circulated earlier this year, in the wake of Russia’s invasion of Ukraine.

The bull case: Above 5% growth

China’s official goal is to double GDP from 2020 levels by 2035, implying growth above 5% for most of this decade. That would need a faster reopening from Covid leading to a quicker resumption in reforms, such as raising the pension age by 2025 and relaxing big city residency restrictions, according to Bloomberg Economics’ model.

Longer term, efforts to boost fertility by providing cheaper childcare and more benefits to parents could pay off, though the impact won’t be clear until those kids enter the workforce in the 2040s.

Then there’s the boost as workers shift from producing less complex goods and services to more valuable ones — something that is easier for China because it has the world’s largest manufacturing base. One way of tracking that is through the Economic Complexity Index compiled by the Growth Lab at Harvard University, which looks at the range of products a country exports. China has risen to 17th from 24th place a decade ago.

The idea is that producing a range of products makes it easier to move up the ladder to more complex products. According to the lab, China’s complexity sets it up to be among the fastest growing economies to 2030 — it predicts growth above 5.8% over the next decade.

Some examples of growing complexity: China now has dozens of globally competitive biotech companies like BeiGene, which was unheard of a decade ago, while video game companies like Tencent and video app TikTok have had success on the global stage for the first time. Chinese companies lead the world in solar power, one of this decade’s clear growth sectors.

Many more success stories will be needed to fuel China’s long-term prospects, but in the short term it all comes down to two key challenges.

“Policy can make a difference to the pace of the growth slowdown: Moving away from the Covid Zero orientation and stabilizing the property market could go a long way to boost short-term growth,” according to Chang and Zhu of Bloomberg Economics. “More importantly, combined with a renewed momentum in structural reforms aiming to boost productivity and labor, these can give the best hope of getting long-term growth back on pre-pandemic paths.”

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.