(Bloomberg) — Russian forces have occupied the site of Europe’s largest nuclear power plant, Ukraine said, after an overnight fire that the government in Kyiv accused Vladimir Putin’s military of causing by shelling the area.

Ukraine’s nuclear regulator said Zaporizhzhia plant personnel were monitoring the state of power units to ensure safety protocols were maintained. The brief fire in a training complex at the plant was out, local emergency services said.

Russian troops are concentrating on encircling the capital, Kyiv while continuing attempts to advance on the port city of Mariupol in the south, the general staff of the Ukrainian army said in a statement. It added that preparations continued for the landing of Russian assault troops near Odesa.

Both houses of Russia’s parliament will be sitting on Friday, with a specially convened meeting of the Federation Council.

Key Developments

- Ukrainians Down Tools and Ditch Trucks to Head Home to Fight

- Putin’s Financial Isolation Is a Cautionary Tale for Xi Jinping

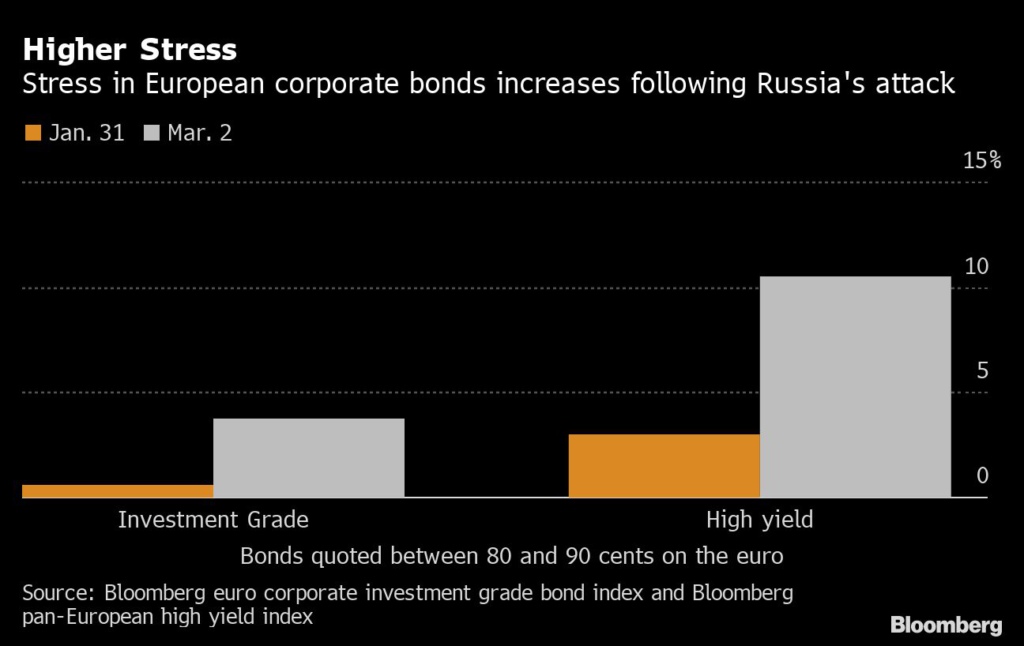

- Oil Extends Wild Week’s Gain as Ukraine Invasion Rattles Markets

- U.S. Sanctions Usmanov, Prigozhin, Tokarev, Other Russian Elites

- Invasion Fallout Frays Supply Chains Anew in Inflation Shock

All times CET:

Czech Republic Allows Volunteers to Fight in Ukraine (8:05 a.m.)

The Czech Republic, where signing up for foreign armies is forbidden by law, will allow its citizens to join Ukrainian forces, Prime Minister Petr Fiala said.

President Milos Zeman, who until last week was a staunch supporter of Putin, will grant pardons to all Czechs fighting for Ukraine. About 300 people have contacted Zeman’s office with requests so far, the CTK newswire reported.

Fire at Nuclear Plant is Extinguished (5:46 a.m.)

The blaze in a training complex at Zaporizhzhia was contained to an area of about 2,000 square meters (20,000 square feet) and is now out, local emergency services said on Facebook. Three floors of a training complex at the site were involved in the fire.

The U.S. did not detect any elevated radiation readings near the facility. U.S. President Joe Biden urged Russia to halt fighting near Zaporizhzhia after speaking with Ukrainian President Volodymyr Zelenskiy about the incident.

“If there is an explosion, it is the end of Europe,” Zelenskiy said in a video message. He’s appealed to Putin to meet, saying it’s the only way to stop the war.

Missile Hit Plant, Energy Minister Says (5:44 a.m.)

A missile hit the nuclear plant’s unit no. 1 and the government was seeking more clarity on any damage, Ukraine Energy Minister Herman Halushchenko said in an interview on Bloomberg TV. He called for outside support to help close air space over the country’s reactors.

NATO has previously made clear it would not set up a no-fly zone over Ukraine as it would bring the alliance’s aircraft into direct confrontation with Russia.

Markets Adjust After Fall (5:10)

Knee-jerk losses in equity markets moderated as traders assessed the severity of the situation at the facility. S&P 500 Index futures were trading 0.9% lower, after earlier falling 1.7%. Gold pared earlier gains as demand for haven assets eased.

Access Curtailed in Russia of Social Media (5:01 a.m.)

Facebook, Twitter and several media websites appear to be fully or partially inaccessible in Russia on Friday, as authorities cracked down on what they call “disinformation” about the war in Ukraine.

Bloomberg journalists in Moscow weren’t able to access Facebook or Twitter. The Meduza news website, an independent Russian-language outlet based in Riga, Latvia, issued a statement saying it had been blocked in Russia. According to GlobalCheck, a service that studies Internet blocks in Russia and other former Soviet states, the BBC and Deutsche Welle websites are also currently unavailable to IP addresses in Russia.

Stocks Fall Amid Fire at Nuclear Plant (3:35 a.m.)

Stocks and equity futures fell and havens including sovereign bonds rose after a fire broke out at major nuclear power plant in Ukraine.

An initial spasm of worry lopped 3% off European equity futures but the panic eased a little as investors weighed the incident. European contracts pared the drop to about 2%, while those for the U.S. shed less than 1%.

Gains in gold and the dollar moderated, while the euro pared a decline. Oil was near $110 a barrel, trimming a jump of as much as 4.8%.

Biden Briefed on Nuclear Plant Danger (3:27 a.m.)

Biden received an update on the nuclear plant attack from Zelenskiy, the White House said in a readout of their call. Both leaders urged “Russia to cease its military activities in the area and allow firefighters and emergency responders to access the site,” the White House said.

The Zaporizhzhia power plant in the city of Enerhodar is home to six Soviet-designed 950-megawatt reactors built between 1984 and 1995 with capacity of 5.7 gigawatts, enough to power more than 4 million homes. The site accounts for about 20% of the country’s electricity, according to its website.

Fire Didn’t Affect Essential Equipment, IAEA Says (3:20 a.m.)

Ukrainian Foreign Minister Dmytro Kuleba said a fire had broken out at the Zaporizhzhia plant and called on Russia’s military to immediately halt firing. Ukraine told the IAEA the fire “has not affected ‘essential’ equipment” and plant personnel were taking “mitigatory actions.”

Plant’s Radiation Levels Unchanged (2:48 a.m.)

The American Nuclear Society said in statement there were no signs that damage caused from the attack posed an additional threat to the public. “Both Russia and Ukraine should understand the importance of ensuring the safety of nuclear power plants and their staff,” the La Grange Park, Illinois non-profit group said.

Nuclear Plant Under Attack, Reports Say (1:16 a.m.)

The Zaporizhzhia nuclear power plant has come under attack by Russian forces, the Associated Press cited Ukrainian officials as saying.

“We demand that they stop the heavy weapons fire,” Andriy Tuz, spokesperson for the plant in Enerhodar, said in a video posted on Telegram. “There is a real threat of nuclear danger in the biggest atomic energy station in Europe.” Telephone calls to the power plant didn’t connect, and the plant didn’t immediately respond to an email seeking comment on the situation.

U.S. Set to Give Protected Status to Ukrainians (11 p.m.)

The Department of Homeland Security will soon begin giving Temporary Protected Status to Ukrainians who are in the U.S.

The move by Homeland Security Secretary Alejandro Mayorkas would be effective as of March 1, meaning that Ukrainian nationals would have to had been in the U.S. by then to be eligible. Members of Congress from both parties have pushed the Biden administration to grant the status, which would allow Ukrainians already in the country to remain for now.

U.S. Immigration and Customs Enforcement has halted deportation flights to Ukraine.

Russian Military Nears Nuclear Power Plant (10:20 p.m.)

The International Atomic Energy Agency confirmed that the Russian military is battling now outside the gates of Europe’s and Ukraine’s biggest nuclear power plant.

In an urgent letter to the IAEA, the Ukraine regulatory authority said Russian infantry were moving directly toward the Zaporizhzhia Nuclear Power Plant and called the situation “critical.”

The IAEA called for an immediate halt to the use of force at Enerhodar and called on the military forces operating there to refrain from combat near the nuclear power plant.

Scholz Tells German Ex-Leader to Cut Russian Ties (9:58 p.m.)

German Chancellor Olaf Scholz called on former leader Gerhard Schroeder to give up board seats on Russian energy companies. Schroeder, chairman of state-owned Russian oil giant Rosneft PJSC and of the shareholder committee of Nord Stream AG, has supported a Russia-to-Germany natural-gas pipeline that Scholz halted last month.

Russia’s invasion of Ukraine has prompted Germany to realign its military and economic stance toward Moscow and Putin. Schroeder, who was German chancellor from 1998 to 2005, has kept up friendly ties with Putin after retiring from politics.

Pentagon Sets Up Emergency Channel to Russian Military (9:09 p.m.)

The U.S. military has established an emergency channel with the Russian military for rapid communications, according to a Pentagon statement.

“The United States retains a number of channels to discuss critical security issues with the Russians during a contingency or emergency,” the Pentagon said.

The Pentagon on March 1 set up what it calls the “deconfliction line” with the Russian Ministry of Defense to prevent the possibility of a misunderstanding that could escalate. The Pentagon said its first offer of such a channel was rejected.

Sanctioned Russians Have No Way Off List (8:57 p.m.)

There is currently nothing Russian oligarchs or officials could do to convince U.S. and European countries to remove them from the sanctions list, two senior officials said Thursday.

Instead, U.S. and EU task forces are hunting down the assets that belong to the tycoons and their families already announced for sanctions. The business leaders and others on the list are a part of the Russian regime and play an important role in the Russian state, a senior EU official said.

Putin’s Spokesman Sanctioned Along With Wealthy Russians (8:04 p.m.)

Dmitry Peskov, Putin’s press secretary, was among those sanctioned by the Biden administration Thursday, as the U.S. and its allies seek to raise pressure on the elites around the Russian president.

The other sanctioned Russians include: Nikolay Tokarev and his wife and daughter; Boris Rotenberg and his wife and sons; Arkady Rotenberg and his sons and daughter; Sergey Chemezov and his wife, son and stepdaughter; Igor Shuvalov and his wife, son, daughter and companies connected to them; Yevgeny Prigozhin and his wife, daughter and son; and Alisher Usmanov, as well as his superyacht and private plane..

Italy’s Generali Winds Down Russian Business (7:54 p.m.)

Italian insurer Assicurazioni Generali SpA is winding down its Europ Assistance operations in Russia, quitting the board of Ingosstrakh Insurance Co. and closing its Moscow representative office.

Generali owns a 38.5% stake in Ingosstrakh, a Russian-based insurer that has billionaire Oleg Deripaska as a shareholder. The insurer provides life and non-life products as well as mortgage loans and savings and retirement plans.

White House Rebuffs Call to Ban Russian Oil (7:36 p.m.)

The White House again rebuffed a call to ban Russian oil from the U.S., this time from House Speaker Nancy Pelosi, one of President Joe Biden’s closest allies.

“We don’t have a strategic interest in reducing the global supply of energy, and that would raise prices at the gas pump for the American people around the world, because it would reduce the supply available,” White House Press Secretary Jen Psaki told reporters at a briefing Thursday. “That is certainly a big factor for the president.”

Russian oil made up only about 3% of all crude imports in the U.S. last year. “Ban it. Ban the oil coming from Russia,” Pelosi told reporters earlier Thursday, making her the highest-ranking Democrat to endorse the move.

Nike Pauses Operations in Russia; Halts Online Sales, Stores (7:32 p.m.)

Nike Inc. will pause operations in Russia, including halting e-commerce sales and temporarily closing company-owned and operated shops in the country. Store employees will continue to receive their paychecks during the closures.

“We are deeply troubled by the devastating crisis in Ukraine and our thoughts are with all those impacted, including our employees, partners and their families in the region,” Nike said in a statement, adding that it will donate $1 million to humanitarian relief efforts.

Russian-Ukrainian Progress Seen on Humanitarian Corridors (7:20 p.m.)

Russian and Ukrainian negotiators agreed to hold a third round of talks after suggesting they made some progress on establishing humanitarian corridors to evacuate civilians.

Russian negotiator Leonid Slutsky said the third round of talks will take place “in the nearest future,” while Mykhailo Podolyak, an adviser to President Zelenskiy’s chief of staff, lamented in a posting on Twitter that “we did not yet get the results that we hoped for.”

Slutsky said more meetings are necessary – and a deal may be ratified at the highest level. The two teams met at a location in the Bialowieza Forest on the Poland-Belarus border.

U.S. Says Quad Promises Humanitarian Aid (6:54 p.m.)

Biden spoke with the other three leaders of the Quad — Australia, India and Japan — and agreed to set up a new line of communication to deliver humanitarian help to Ukraine, according to a White House statement.

Garland Vows ‘No Stone Unturned’ on Crimes Against Ukraine (6:50 p.m.)

U.S. Attorney General Merrick Garland said the Justice Department and international allies “will leave no stone unturned in our efforts to investigate, arrest and prosecute those whose criminal acts enable the Russian government to continue its unjust war against Ukraine.”

A veteran prosecutor for the U.S. attorney’s office in Manhattan, Andrew Adams, has been tapped to lead a new task force targeting the assets of wealthy Russians who violate U.S. sanctions, Garland said in a speech before a lawyer’s conference on Thursday.

Putin Says Ukraine Operation ‘Is Going Strictly on Schedule’ (6:30 p.m.)

“All the goals that have been set are being attained,” Putin told top officials in televised comments to a meeting of his Security Council. Reiterating his view that Russians and Ukrainians are “one people,” Putin claimed his forces are fighting “neo-Nazis” and forces from outside Ukraine.

Ukraine, which has committed its army to the battle, and its allies have charged Russia with targeting cities and civilians.

Zelenskiy said Thursday he feared Putin had broader goals than Ukraine. If “God forbid, Russia takes Ukraine,” then next will be Latvia, Lithuania, Estonia, Moldova, Georgia, and Poland, he told foreign reporters in Kyiv. “And they won’t stop until they reach Berlin,” he said.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.