(Bloomberg) — Ukraine’s central bank delayed a scheduled rate decision until conditions normalize. Volkswagen and Ikea became the latest companies to suspend business in Russia as Kremlin forces pressed ahead with their offensive, firing missiles at Kyiv overnight and stepping up their campaign to take key cities in the coastal south, on the Black Sea.

With more than a million refugees fleeing to neighboring countries, according to the United Nations, a second round of talks between Russia and Ukraine were due to take place on Thursday. U.S. Secretary of State Antony Blinken will travel over the weekend to NATO member states neighboring Ukraine.

The economic fallout for Russia continued to grow. Its central bank banned transferring coupon payments for sovereign debt temporarily, raising the risk for investors that the Kremlin could default. Crude oil hovered at multi-year highs.

Key Developments

- Biden’s Tough Sanctions Create Worry That Putin Lacks an Exit

- Russian Assault Shows No Letup as Putin’s War Enters Second Week

- The Default Question Hangs Over Russia’s Frozen Bond Market

- Overwhelming UN Vote Makes China’s Ukraine Balancing Act Harder

- Russian Invasion Pushes Europe Into New Era of Big Spending

- Russian Fleet Approach Has Ukraine’s Port City of Odesa Bracing

All times CET:

Poland Plans to Raise Defense Spending to 3% of GDP (2:26 p.m.)

Poland wants to raise its defense spending to 3% of economic output in 2023 and will start a “very expensive” program to expand and re-arm its military over the next five years, the country’s de facto leader Jaroslaw Kaczynski told parliament in Warsaw.

The nation’s $600 billion economy is already spending more on defense than the NATO’s target of 2% of GDP. The program will include the creation of a voluntary military force that would increase army personnel to about 300,000, Kaczynski said.

Russia Seeks to Weaken Ukraine Morale: Intelligence Report (2:26 p.m.)

Moscow has drawn up plans for ways to break morale in order to discourage Ukrainian from fighting back as and when cities fall under the Kremlin’s control, a European intelligence official said.

That strategy includes crackdowns on protests, detention of opponents, and potentially carrying out public executions, the official said on the condition of anonymity. So far civilians in Ukraine as well as its military have put up strong resistance, including arming themselves as volunteer forces.

Oil, Gas Prices Swing Wildly; Aluminum, Wheat Soar (2:10 p.m.)

Oil extended a period of extreme volatility, with international Brent nearing $120 a barrel at one point, while European natural gas retreated after hitting a record high. Aluminum powered through to unprecedented levels and wheat extended its rally to the highest since 2008.

Russia’s growing isolation is choking a major global source of energy, metals and crops, sparking fears of prolonged shortages and sharper global inflation. While there are no sanctions on energy, traders and shippers are increasingly reluctant to deal with Russian supply or with its companies.

Sanctioned Billionaire Says ‘Iron Curtain’ Has Fallen (2:05 p.m.)

An “Iron Curtain” has fallen on Russia and the country faces a severe crisis for at least three years, billionaire Oleg Deripaska said at the Krasnoyarsk Economic Forum on Thursday.

Deripaska, who’s been sanctioned by the U.S. since 2018, said the first step to getting out of the current crisis is peace.

Russia’s economic outlook has grown increasingly dire in the last week, as the ruble crashed, inflation and interest rates jumped and foreign companies vowed to stop doing business in the country.

Second Round of Ukrainian-Russian Talks Starting Soon (1:35 p.m.)

A second round of talks between Russian and Ukrainian negotiators is set to get under way as soon as 3 p.m. CET. Mykhailo Podolyak, an adviser to President Volodymyr Zelenskiy’s chief of staff, was shown in a tweet strapped into a helicopter with a party ally.

The discussions are planned at a location in the Bialowieza Forest on the Poland-Belarus border. A first round of talks, where the Russians laid out their demands for Ukrainian “neutrality,” bore little fruit.

Biden Asks Congress for $10 Billion in Ukraine Funding (1:20 p.m.)

The White House asked Congress for about $10 billion in emergency funding for Ukraine, to be used to address the mounting humanitarian crisis as well as assist its defense against Russia. Of that, $4.8 billion would go to the Pentagon and $5 billion to the State Department.

The funds were part of a $32.5 billion funding request; the balance would be for domestic coronavirus efforts. Negotiations continue on how to operate the federal government past March 11, when current funding is set to lapse.

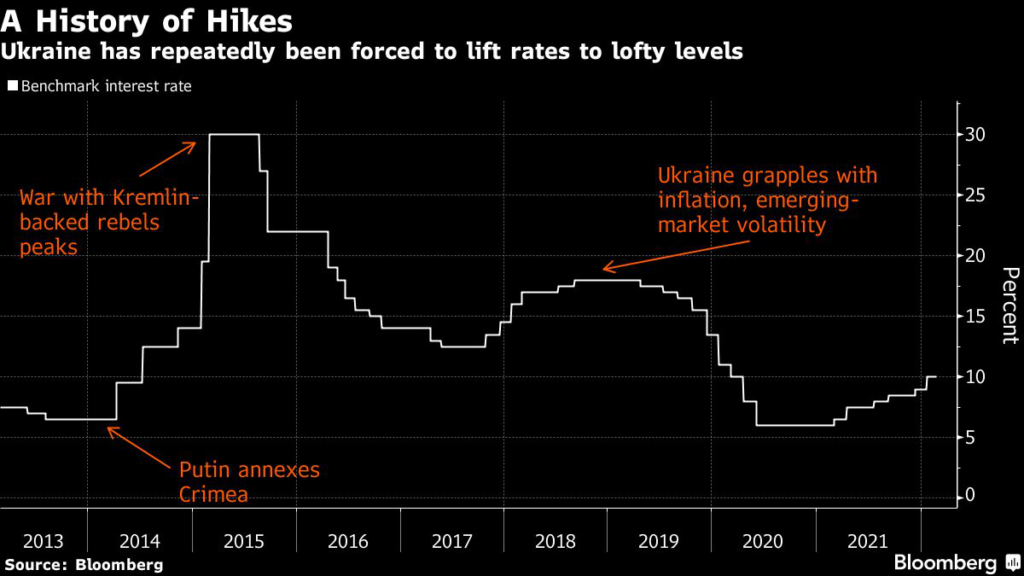

Ukraine Central Bank Delays Decision as Attack Continues (1:02 p.m.)

Ukraine’s central bank delayed a scheduled decision on borrowing costs, with the key rate staying at 10% for now.

The National Bank of Ukraine said it remains committed to inflation targeting and it will resume regular monetary policy meetings once the economy normalizes.

Macron Speaks Again With Putin, Zelenskiy (12:41 p.m.)

Emmanuel Macron spoke with Vladimir Putin for an hour and a half on Thursday, according to the Elysee palace, which said the French president has also talked with Ukrainian counterpart Volodymyr Zelenskiy.

In a televised speech Wednesday, Macron said he’ll stay in contact with Putin “for as long as I can and as long as it is needed” to convince him to stop the attacks against Ukraine.

Japan to Freeze Oligarchs’ Assets (12:31 p.m.)

Prime Minister Fumio Kishida said Japan would freeze the assets of oligarchs in his country as Tokyo stepped up its penalties on Russia. The premier said it was “outrageous” for Vladimir Putin to order Russia’s strategic nuclear forces to be put on higher alert, adding that the use, or even the threat, of using nuclear weapons was unforgivable.

Finnish President Niinisto to Meet Biden on Friday (12:15 p.m.)

Finnish President Sauli Niinisto will visit President Joe Biden and U.S. lawmakers in Washington on Friday, just as the debate on joining NATO has intensified in the Nordic country after its neighbor Russia invaded Ukraine.

The attack has prompted a historic shift in Finns’ attitudes on joining the North Atlantic Treaty Organization, with a majority now supporting the idea. Niinisto and Biden are scheduled to discuss the invasion and its impact on European security.

VW Stops Making Cars in Russia (11:47 a.m.)

Volkswagen AG said it would stop producing vehicles in Russia and exporting to that market until further notice because of the invasion of Ukraine.

The German carmaker joins an exodus of companies from Russia, reversing three decades of investment by Western and other foreign businesses there following the collapse of the Soviet Union in 1991.

Firms ranging from energy giants Exxon Mobil and Shell to fashion retailers Burberry and H&M have announced they are curtailing operations or leaving entirely.

Ikea said Thursday it would pause all operations in Russia and Belarus, affecting about 15,000 employees.

French Customs Takes Yacht Owned by Rosneft CEO (11:25 a.m.)

French customs officials have taken control of a giant yacht owned by Rosneft Chief Executive Officer Igor Sechin as part of EU sanctions against Russia, French Finance Minister Bruno Le Maire said.

The Amore Vero was confiscated overnight in the Mediterranean port of La Ciotat, near Marseille, on the French Cote d’Azur as it was preparing an urgent departure, the ministry said.

EU Expects Membership Requests From Moldova, Georgia (11:13 a.m.)

Georgia and Moldova are expected to send membership requests to the EU imminently, according to an EU official.

The EU is already in the process of moving forward on an application from Ukraine, a topic the 27 leaders will discuss next week at an informal summit in Paris, said the official, who asked not to be identified because the talks are private. Moldova may submit the request Thursday, the official said.

“Ukraine has set a process in motion, and this will be discussed with member states, but right now the focus is on ending the war,” European Commission President Ursula von der Leyen said in Bucharest.

EU Figures Float Special Budget Leeway for Defense Spending (11:01 a.m.)

European Commissioner for Economy Paolo Gentiloni and Hungarian Prime Minister Viktor Orban suggested giving special consideration to defense spending under European Union rules that limit public finance deficits.

Gentiloni told the German Handelsblatt newspaper he was “open to thinking about also giving special consideration in the debt rules to investments in Europe’s autonomy. This can also include certain defense expenditures.” He said a specific proposal hadn’t yet been agreed.

Orban said Russia’s war on Ukraine made clear that “much more” needs to be spent on the continent’s militaries and that shouldn’t be included in the current deficit ceiling of 3% of gross domestic product. The EU has already agreed to finance the supply of 450 million euros in lethal weapons to Ukraine, as well as 50 million euros of non-lethal aid.

Ukraine Calls for Russia’s Suspension From WTO (10:49 a.m.)

Ukraine urged all members of the World Trade Organization to suspend Russia from participating in the Geneva-based trade body in response to its “unprovoked and unjustified” attack, according to a letter seen by Bloomberg.

Ukraine has imposed a “complete economic embargo” on Russia and will no longer apply the WTO’s agreements with regard to Russia, it said.

Zelenskiy Addresses Nation (10:15 a.m.)

Paralympic Committee Boots Russia, Belarus (9:42 a.m.)

The International Paralympic Committee won’t let Russia and Belarus participate in the Beijing Paralympics after athletes from other countries threatened a boycott that could have halted the games.

The decision was an embarrassing about-face for the IPC, which had said less than a day earlier that it would allow Russians and Belarusians to compete at events as neutral athletes.

Overwhelming UN Vote Puts Pressure on China (9:27 a.m.)

The United Nations passed a resolution condemning Russia’s invasion of Ukraine by an overwhelming vote, casting a spotlight on President Xi Jinping’s reluctance to take a stance against Moscow, after China abstained.

Russia’s Ekho Moskvy Radio Station to Close (9:01 a.m.)

The board of Ekho Moskvy, Russia’s most prominent liberal radio broadcaster, voted to liquidate the station and its website, Editor-in-Chief Alexei Venediktov said.

Earlier this week, the Russian Prosecutor General’s office ordered the broadcaster off the air in a move criticized by the Committee to Protect Journalists.

Ekho Moskvy was founded in the waning days of the Soviet Union and managed to retain its editorial independence for over three decades even as the state brought most broadcast media under its control.

EU to Offer Residence, Job Rights to Ukrainians (8:42 a.m.)

Ukrainians fleeing to the European Union will be granted full access to the bloc and receive residence permits as well as access to education and jobs as part of a plan expected to be implemented as soon as Thursday.

European member states will consider activating the so-called temporary protection directive that will allow Ukrainians to stay in the EU beyond 90 days, a move expected to be overwhelmingly adopted, according to a senior official at the European Commission.

Switzerland is also weighing offering temporary residence in the country to Ukrainians.

More Than 1 Million People Have Fled Ukraine: UNHCR (8:36 a.m.)

Russia’s invasion has forced 1,002,860 people to flee Ukraine to neighboring countries, the UN refugee agency said Thursday, in what is poised to become the biggest humanitarian crisis in Europe since World War II.

It said more than half a million people had fled to Poland, while 139,686 had gone to Hungary, 97,827 to Moldova and 72,200 to Slovakia. Romania had taken in 51,261 the UNHCR said, while 47,800 people had departed for Russia.

Russian-Backed Forces Threaten Strikes on Mariupol (8:03 a.m.)

A spokesman for Russian-backed separatists threatened strikes on Mariupol to demoralize the Ukrainian army and said an evacuation corridor for civilians wasn’t working, in comments broadcast on Rossiya 24. A Pentagon official said earlier that Russian forces appear to be preparing to assault the encircled port city.

Ukraine’s military headquarters said that Russia is sending four amphibious assault ships to land troops near Odesa’s seaport and seize the city.

National police in Kyiv said that there were explosions in the capital overnight, but that they were the result of Ukraine’s anti-missile systems hitting Russian targets.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.