Russia Hits Cities as Kyiv, Moscow to Hold Talks: Ukraine Update

(Bloomberg) — The EU Council sent a request to the European Commission to consider Ukraine’s membership. Russian forces pressed ahead with their offensive, firing missiles at Kyiv overnight and stepping up their campaign to take cities in the coastal south.

With more than a million refugees fleeing to neighboring countries, according to the United Nations, a second round of talks between Russia and Ukraine were due to take place on Thursday. U.S. Secretary of State Antony Blinken is meanwhile traveling to NATO member states neighboring Ukraine.

Russia continued to suffer economic fallout from its invasion, with its rating slashed to junk on the back of a wave of sanctions by the U.S., the European Union and others. The global economy was further roiled with crude oil extending gains.

Key Developments

- Biden’s Tough Sanctions Create Worry That Putin Lacks an Exit

- NATO Faces Reality of Emboldened Russia on Its Doorstep

- Resignation Sets In as Russians Face Their New Economic Reality

- Overwhelming UN Vote Makes China’s Ukraine Balancing Act Harder

- Russian Invasion Pushes Europe Into New Era of Big Spending

- Russian Fleet Approach Has Ukraine’s Port City of Odesa Bracing

All times CET:

EU Expects Membership Requests From Moldova, Georgia (11:13 a.m.)

Georgia and Moldova are expected to send membership requests to the EU imminently, according to an EU official.

The EU is already in the process of moving forward on an application from Ukraine, a topic the 27 leaders will discuss next week at an informal summit in Paris, said the official, who asked not to be identified because the talks are private. Moldova may submit the request Thursday, the official said.

“Ukraine has set a process in motion, and this will be discussed with member states, but right now the focus is on ending the war,” European Commission President Ursula von der Leyen said in Bucharest.

EU Figures Float Special Budget Leeway for Defense Spending (11:01 a.m.)

European Commissioner for Economy Paolo Gentiloni and Hungarian Prime Minister Viktor Orban suggested giving special consideration to defense spending under European Union rules that limit public finance deficits.

Gentiloni told the German Handelsblatt newspaper he was “open to thinking about also giving special consideration in the debt rules to investments in Europe’s autonomy. This can also include certain defense expenditures.” He said a specific proposal hadn’t yet been agreed.

Orban said Russia’s war on Ukraine made clear that “much more” needs to be spent on the continent’s militaries and that shouldn’t be included in the current deficit ceiling of 3% of gross domestic product. The EU has already agreed to finance the supply of 450 million euros in lethal weapons to Ukraine, as well as 50 million euros of non-lethal aid.

Ukraine Calls for Russia’s Suspension From WTO (10:49 a.m.)

Ukraine urged all members of the World Trade Organization to suspend Russia from participating in the Geneva-based trade body in response to its “unprovoked and unjustified” attack, according to a letter seen by Bloomberg.

Ukraine has imposed a “complete economic embargo” on Russia and will no longer apply the WTO’s agreements with regard to Russia, it said.

Zelenskiy Addresses Nation (10:15 a.m.)

Paralympic Committee Boots Russia, Belarus (9:42 a.m.)

The International Paralympic Committee won’t let Russia and Belarus participate in the Beijing Paralympics after athletes from other countries threatened a boycott that could have halted the games.

The decision was an embarrassing about-face for the IPC, which had said less than a day earlier that it would allow Russians and Belarusians to compete at events as neutral athletes.

Gas Prices Surge, Oil Reaches Highest Since 2008 (9:42 a.m.)

European natural gas jumped to a fresh record as the market continues to react to sanctions aimed at Russia. Dutch front-month futures gained as much as 20% to 198 euros a megawatt-hour. The U.K. equivalent gained 17%.

While sanctions aren’t specifically targeting natural resources, traders and shippers are shying away from dealing with Russian suppliers. Oil soared to the highest level since 2008, with WTI rising as much as 5.4% to above $116 a barrel.

Overwhelming UN Vote Puts Pressure on China (9:27 a.m.)

The United Nations passed a resolution condemning Russia’s invasion of Ukraine by an overwhelming vote, casting a spotlight on President Xi Jinping’s reluctance to take a stance against Moscow, after China abstained.

Russia’s Ekho Moskvy Radio Station to Close (9:01 a.m.)

The board of Ekho Moskvy, Russia’s most prominent liberal radio broadcaster, voted to liquidate the station and its website, Editor-in-Chief Alexei Venediktov said.

Earlier this week, the Russian Prosecutor General’s office ordered the broadcaster off the air in a move criticized by the Committee to Protect Journalists.

Ekho Moskvy was founded in the waning days of the Soviet Union and managed to retain its editorial independence for over three decades even as the state brought most broadcast media under its control.

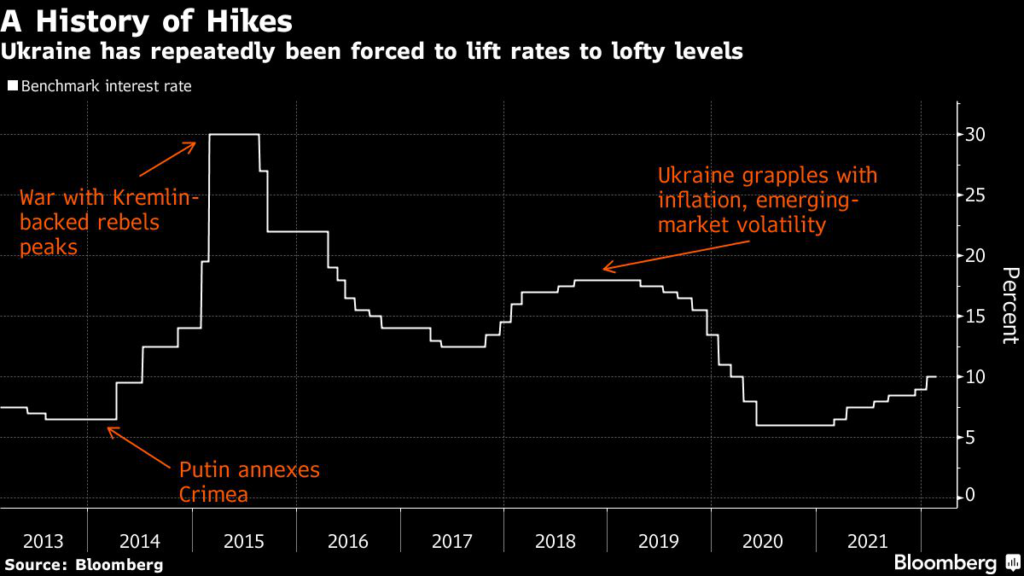

Ukraine to Hike Interest Rates in Face of War (8:50 a.m.)

As Russian troops bear down on Kyiv, Ukraine’s central bank is poised hike its key interest rate on Thursday in a bid to stabilize the economy. But the fog of war leaves economists struggling to predict how much it will tighten monetary policy. The base rate is currently 10%.

EU to Offer Residence, Job Rights to Ukrainians (8:42 a.m.)

Ukrainians fleeing to the European Union will be granted full access to the bloc and receive residence permits as well as access to education and jobs as part of a plan expected to be implemented as soon as Thursday.

European member states will consider activating the so-called temporary protection directive that will allow Ukrainians to stay in the EU beyond 90 days, a move expected to be overwhelmingly adopted, according to a senior official at the European Commission.

Switzerland is also weighing offering temporary residence in the country to Ukrainians.

More Than 1 Million People Have Fled Ukraine: UNHCR (8:36 a.m.)

Russia’s invasion has forced 1,002,860 people to flee Ukraine to neighboring countries, the UN refugee agency said Thursday, in what is poised to become the biggest humanitarian crisis in Europe since World War II.

It said more than half a million people had fled to Poland, while 139,686 had gone to Hungary, 97,827 to Moldova and 72,200 to Slovakia. Romania had taken in 51,261 the UNHCR said, while 47,800 people had departed for Russia.

Russian-Backed Forces Threaten Strikes on Mariupol (8:03 a.m.)

A spokesman for Russian-backed separatists threatened strikes on Mariupol to demoralize the Ukrainian army and said an evacuation corridor for civilians wasn’t working, in comments broadcast on Rossiya 24. A Pentagon official said earlier that Russian forces appear to be preparing to assault the encircled port city.

Ukraine’s military headquarters said that Russia is sending four amphibious assault ships to land troops near Odesa’s seaport and seize the city.

National police in Kyiv said that there were explosions in the capital overnight, but that they were the result of Ukraine’s anti-missile systems hitting Russian targets.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.