(Bloomberg) — The U.S. led condemnation of Russia’s actions at the United Nations, after President Vladimir Putin’s decision to officially recognize two self-proclaimed separatist republics in eastern Ukraine escalated tensions with the West.

The U.S. and the U.K. said they would place additional sanctions on Russia in response to the move, which torpedoed European-mediated peace talks and prompted the State Department to temporarily evacuate personnel. The ruble tumbled its most in about two years, while the Biden administration reaffirmed its “unwavering” support for Ukraine.

Putin also ordered the Defense Ministry to send what he called “peacekeeping forces” to the separatist regions. Moscow continues to deny it plans to invade and the question now becomes what the U.S. and its allies would define as an invasion, and what will trigger the bigger sanctions.

Key Developments

- U.S. Orders Personnel Out of Ukraine on Threat From Russia

- Putin Orders Forces to Separatist Areas of Ukraine After Decree

- Stocks to Extend Drop on Deepening Ukraine Tension: Markets Wrap

- U.S. Warns That Russia May Target Multiple Cities in Ukraine

- Explainer: Why Minsk Accords Are Murky Path for Ukraine Peace

- Why Donetsk and Luhansk Matter to Putin and Global Security: Q&A

All times CET:

Blinken Reassures Kuleba in Call (5:40 a.m.)

Secretary of State Antony Blinken spoke with Ukrainian Foreign Minister Dmytro Kuleba by telephone “to reaffirm unwavering U.S. support,” the State Department said in a statement. The two discussed recent U.S. measures taken to punish Russia and additional steps that would be on the way.

Blinken and Kuleba are due to meet in Washington on Tuesday for further talks, it said.

Russia Isolated at UN Security Council (4:35 a.m.)

Russia’s international isolation was made clear at an emergency meeting of the UN Security Council on Monday night in New York. While some countries called for both sides in the dispute to ease tensions, Russia’s move was roundly condemned by nearly all the members of the council.

Putin “wants to demonstrate that through force he can make a farce of the UN,” U.S. Ambassador Linda Thomas-Greenfield said, later adding that the Biden administration plans additional sanctions against Russia on Tuesday. The U.K. ambassador, Barbara Woodward, said Russia has brought us to the brink. We urge Russia to step back.”

Russia’s UN envoy, Vassily Nebenzia, had the dual role of serving as the Security Council’s president, calling on the speakers, and as his nation’s representative. He criticized what he called Ukraine’s poor treatment toward its citizens in the eastern regions where Moscow has said it is now sending troops and said the West had pressed the country to be more aggressive and militaristic.

China Urges Restraint (4:06 a.m.)

China’s ambassador to the UN, Zhang Jun, made only brief remarks to the Security Council, calling on all sides to exercise restraint. “We believe that all countries should solve international disputes by peaceful means in line with the purposes and principles of the UN charter,” Zhang said.

Meanwhile, Chinese Foreign Minister Wang Yi spoke by phone with Secretary of State Antony Blinken, who the State Department said “underscored the need to preserve Ukraine’s sovereignty and territorial integrity.”

U.S. Plans New Russia Sanctions Tuesday (3:38 a.m.)

The U.S. plans to announce new sanctions Tuesday in response to Russian actions on Ukraine, according to a Biden administration official. The U.S. is coordinating with allies and partners on that announcement.

Thomas-Greenfield separately told emergency Security Council meeting that the U.S. would “take further measures to hold Russia accountable for this clear violation of international law.” The U.K. also plans to impose additional measures.

U.S. Diplomats Head to Poland (3:35 a.m.)

Blinken said in a statement that his department’s personnel currently in Lviv would spend the night in Poland, citing safety and security reasons. He said they will regularly return to continue their diplomatic work in Ukraine and provide emergency consular services.

“The fact that we are taking prudent precautions for the sake of the safety of U.S. government personnel and U.S. citizens, as we do regularly worldwide, in no way undermines our support for, or our commitment to, Ukraine,” he said.

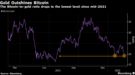

Ruble Sinks as Putin Speaks (3:12 a.m.)

The ruble tumbled the most since March 2020 after Putin recognized the self-declared separatist republics in east Ukraine. The currency weakened beyond 80 per dollar during Putin’s televised address to Russians late Monday and stocks slumped as much as 18% in evening trading.

Ukraine Leader Urges Calm (12:51 a.m.)

Ukraine will stick to a peaceful and diplomatic path. That is the message from president Volodymyr Zelenskiy in his late-night address to the nation. Putin has in practice merely “legalized” troops already present in self-proclaimed republics since 2014, he said.

Zelenskiy praised Ukrainians for their calm stance and assured them that the country’s borders are safely guarded. “There are no reasons for your sleepless night,” Zelenskiy said.

UN Security Council Holds Emergency Meeting (12:15 a.m.)

The decision-making body of the United Nations, the UN Security Council, will hold an emergency meeting on Monday night at 9 p.m. New York time. The session will be open, meaning people will be allowed to listen in on the discussion. Expect a lively debate but not much more.

There are five countries that hold veto power — China, France, Russia, the U.K. and the U.S. — and that has essentially led to gridlock on major geopolitical discussions and meant things like sanctions are non-starters. This month, Russia holds the rotating presidency and that means it chairs meetings and set the agenda.

Congress Chimes In After Putin Nods to Separatists (11:38 p.m.)

Congress’s bipartisan delegation to the Munich Security Conference said lawmakers would work together on any emergency supplemental legislation to support NATO and Ukraine. The group including Senators Lindsey Graham, a South Carolina Republican, and Dick Durbin, an Illinois Democrat, said Putin must be held accountable should Russia invade Ukraine.

House Speaker Nancy Pelosi, leading a separate congressional delegation, met U.K. Prime Minister Boris Johnson on Monday. She said they discussed deterrence strategies including the “threat” of preventing Russian companies from accessing U.S. dollars and the British pound.

Putin Orders Russian Troops to East Ukraine Separatist Zones (11:04 p.m.)

Putin ordered Russian armed forces to carry out “peacekeeping” duties in the separatist regions of Ukraine, according to the text of the decrees he signed on Monday. While Russia will argue Putin’s recognition of the separatist regions gives a legal basis for the presence of its troops, the move will likely fuel U.S. and European concerns that Moscow is moving to take control of territory internationally recognized as part of Ukraine.

The orders potentially move Russian forces closer to direct confrontation with Ukrainian troops at the line of separation with the separatist regions. There was no immediate detail on how many troops might go in, or when.

Macron Calls Putin’s Move a Violation of Commitments (10:25 p.m.)

Macron rebuked Putin’s decree as an encroachment of Ukraine’s sovereignty, his office said in a statement. The French leader is calling for an emergency meeting of the UN Security Council and the adoption of targeted European sanctions.

Macron had engaged in an intense diplomatic marathon to try and solve the crisis, acting as an intermediary between Putin and Biden and seeking to develop a rapport with Putin.

U.K. Set to Impose Sanctions On Russia Tuesday (9:50 p.m.)

The move comes after new rules introduced in London last week that allow ministers to punish Russian businesses and individuals in a wide range of sectors including financial services, chemicals, construction, defense, electronics, energy, mining, transport and communications and digital. There will be further sanctions if an actual incursion into Ukraine happened, Foreign Secretary Liz Truss said.

Truss took to Twitter Monday night to condemn Putin’s recognition of the separatists. “It demonstrates Russia’s decision to choose a path of confrontation over dialog,” she wrote.

Biden Plans Order Barring U.S. Trade With Separatist Regions (9:34 p.m.)

The U.S. President will issue an executive order Monday prohibiting U.S. investment, trade, and financing to separatist regions of Ukraine after Putin’s move to officially recognize the breakaway territories.

The executive order will allow the U.S. to sanction individuals operating in the area, and the U.S. will also “soon” announce additional measures “related to today’s blatant violation of Russia’s international commitments,” White House press secretary Jen Psaki said. Trade and investment has already plummeted since Russian-backed separatists took control of the regions eight years ago.

Secretary of State Antony Blinken made no direct mention of sanctions, but said “appropriate steps” would be taken to “this unprovoked and unacceptable action by Russia.” Blinken said Biden’s actions will only prohibit new — rather than existing — U.S. investment, trade, and financing in the breakaway regions, and that the restrictions would not impact the Ukrainian people, government, or humanitarian organizations.

EU to React With New Sanctions Over Russian Decree (9:20 p.m.)

EU ambassadors will meet Tuesday to discuss a plan for sanctions in response to Putin’s decree, according to multiple diplomats familiar with the talks. Member states are expected to make a swift decision on a package in the following days, the officials said.

EU chiefs Ursula von der Leyen and Charles Michel said earlier in a joint statement that Putin’s move was “a blatant violation of international law as well as of the Minsk agreements,” referring to the agreement where Russia had recognized the two regions as part of Ukraine.

Any sanctions would have to be unanimously adopted and the bloc has yet to agree which specific measures to take in response. Polish Prime Minister Mateusz Morawiecki said the European Council should call an urgent meeting to impose “immediate sanctions” against Russia.

Germany, U.K., Romania Among Those Condemning Putin’s Order (8:58 p.m.)

Scholz condemned the move to recognize the territories, which is in stark contrast to the push by Germany and France to implement the Minsk peace accords aimed at ending a separatist conflict that’s smoldered since 2014. U.K. Prime Minister Boris Johnson called it an “ill omen” and “flagrant violation” of the sovereignty and integrity of Ukraine.

“I don’t know what is in his mind,” Johnson added at a Downing Street press conference. “There’s a chance he could row back from this.”

Czech Defense Minister Jana Cernochova said on Twitter that the world can’t tolerate Putin’s move as it’s “not just Ukraine on Putin’s chessboard, we’re there.’

EU Warns on Russian Cyber Actions in Any Ukraine Attack (7:26 p.m.)

The European Union warned it is highly likely Russia would launch cyberattacks to interfere with electronic payments and online services systems if it launches a military attack against Ukraine.

The EU’s computer emergency response team warned the bloc’s institutions that cyberattacks could also be aimed at damaging critical infrastructure, as well as targeting and manipulating news sources. The aim of the operations would be to hamper financial transactions, impede access to key services and sow divisions among the population.

The internal document seen by Bloomberg said Russia is unlikely to attempt to take down Ukraine’s entire Internet. Moscow has denied it was behind recent cyberattacks on Ukraine.

EU Yet to Agree Potential Sanctions for Separatist Recognition (5:15 p.m.)

Several EU leaders had already called for sanctions should Putin opt to recognize the separatist territories in eastern Ukraine. Still, countries have yet to agree on what sanctions would be imposed in such circumstances, according to diplomats and officials who asked not to be identified discussing confidential matters.

“If there is an annexation, there will be sanctions,” EU foreign policy chief Josep Borrell told reporters after a meeting of foreign ministers in Brussels. “And if there is a recognition, I will put the sanctions on the table and the ministers will decide. I will certainly put on the table the sanctions package that has been prepared if such a thing happens.”

Russia Security Council Members Argue for Separatists (4:43 p.m.)

The televised meeting of the Security Council on Monday showed member after member arguing in favor of recognizing two self-proclaimed republics in eastern Ukraine’s Donbas region. Only a few suggested giving the West more time to address Russia’s security demands.

When Sergei Naryshkin, the head of Russia’s Foreign Intelligence Service, suggested annexing the territories, Putin corrected him and said that wasn’t on the agenda, a sign they could remain frozen conflicts similar to two largely unrecognized Russian protectorates that split from Georgia after a 2008 war.

“We see the threats and blackmail from our Western colleagues, we understand what such a step entails, but we also understand the situation that has developed,” Putin said at the start of the meeting.

The leaders of the so-called Donetsk People’s Republic and Luhansk People’s Republic earlier appealed to Putin to recognize their independence from Ukraine and conclude a treaty on defense.

Ukraine Denies Attack on Russian Forces (3 p.m.)

Foreign minister Dmytro Kuleba denied Russian allegations that Kyiv sent “saboteurs” and armed personal carriers into Russia’s Rostov region early Monday.

Russia Says It Killed 5 ‘Saboteurs’ From Ukraine (2:15 p.m.)

Russian forces killed five “saboteurs” and destroyed two Ukrainian armored personnel carriers that crossed into Russian territory in the Rostov region early Monday, state-run Tass news service reported, citing a statement from the Southern Military District.

The alleged strike comes as tensions have escalated between the Ukrainian army and separatists in the two breakaway republics in the east, with both sides accusing the other of increased shelling in recent days.

Unlike the firing along the contact line between Ukraine and the separatists, Russia alleged this incident took place over the international border.

Ukraine Says Russian-Backed Separatists Shelling Villages (12:48 p.m.)

Vrubivka and Shchastya, in Ukraine’s eastern Luhansk region, are being shelled by Russian-backed separatists, regional government head Serhiy Hayday said on Facebook. Vrubivka has seen electricity and gas supplies cut while Shchastya is without power or water, he said. Meanwhile officials in Kyiv said shelling on Monday by separatists killed two troops and one civilian, and wounded four soldiers.

Separatists in turn accused Ukrainian forces of what they said were massive attacks with artillery and other weapons. Both sides have traded accusations of violence amid a surge in violations along the contact line in Ukraine’s Donbas over the past week.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.