(Bloomberg) — FTX Trading Ltd. and about 100 affiliated companies are starting a strategic review of global assets as a part of the Chapter 11 bankruptcy process.

That comes after FTX said it fired three top deputies of former Chief Executive Officer Sam Bankman-Fried, the Wall Street Journal reported.

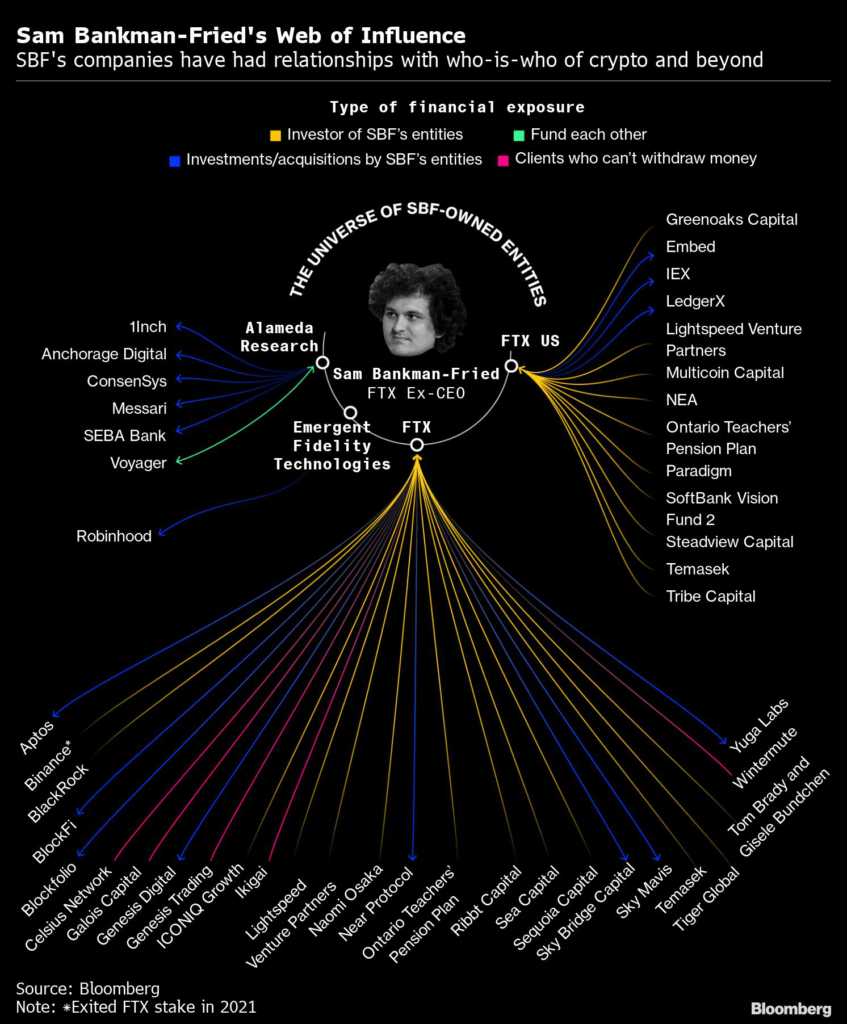

The collapse of the crypto empire is being transformed into a new political battlefront as Republicans highlight links between Democrats and their one-time benefactor Bankman-Fried.

Missouri Republican Senator Josh Hawley on Friday sent a broad request for correspondence between federal agencies and Democrats, including the Biden administration and the House and Senate Democrats’ campaign committees, regarding FTX and trading house Alameda Research. Hawley said he’s trying to determine whether Bankman-Fried’s more than $37 million in political donations to Democrats may have created pressure on regulators to be lenient with the former crypto executive.

Meanwhile, the chair of a House panel is asking FTX to turn over documents and information by Dec. 1 as part of its investigation into the collapse of the crypto platform.

Key stories and developments:

- FTX Bankruptcy Bombshells Squeeze Crypto Lenders Behind Bull Run

- Wall Street Beat: FTX Lesson for Taking Funds by Debt and Tokens

- FTX’s Point of No Return Was Ellison’s Tweet, Trade Data Show

- Bankman-Fried’s Island Haven Draws Scrutiny After FTX Demise

- FTX Existential Crisis Fix; TMT’s Mega-Cap Problem (Podcast)

(Time references are New York unless otherwise stated.)

FTX Starts Global Asset Review as Part of Chapter 11 (3:18 a.m.)

FTX Trading Ltd. and about 100 affiliated companies are starting a strategic review of global assets as a part of the Chapter 11 bankruptcy process.

“Based on our review over the past week, we are pleased to learn that many regulated or licensed subsidiaries of FTX, within and outside of the US, have solvent balance sheets, responsible management and valuable franchises,” FTX Group’s new Chief Executive Officer John J. Ray III said in a statement.

The FTX companies, known as FTX Debtors, have engaged Perella Weinberg Partners LP as lead investment bank and started preparing some assets for sale or reorganization, according to the statement.

FTX Japan to Develop System for Withdrawals: Asahi (11:54 p.m.)

The Japan unit of FTX has started developing a system that will enable customers to withdraw their funds, the Asahi newspaper reported Saturday, citing company executive Seth Melamed.

FTX Fires Sam Bankman-Fried’s Top Deputies, WSJ Reports (10:07 p.m.)

FTX said it fired three top deputies of former Chief Executive Officer Sam Bankman-Fried, the Wall Street Journal reported.

FTX co-founder and chief technology officer Gary Wang, engineering director Nishad Singh and Caroline Ellison, who ran Alameda Research, were terminated from their positions, the paper said, citing an FTX spokeswoman late Friday. The paper didn’t say if it attempted to reach the executives for comment.

They left those roles after FTX appointed John J. Ray to oversee the bankruptcy, according to the report. The newspaper had previously reported that the executives were aware of the decision to send client money to trading firm Alameda.

Hawley Seeks Democrats’ Emails as FTX Collapse Turns Political (4:04 p.m.)

The collapse of the crypto empire founded by political mega-donor Sam Bankman-Fried is being transformed into a new political battlefront as Republicans highlight links between Democrats and their one-time benefactor.

Missouri Republican Senator Josh Hawley on Friday sent a broad request for correspondence between federal agencies and Democrats, saying he’s trying to determine whether Bankman-Fried’s more than $37 million in political donations to Democrats may have created pressure on regulators to be lenient with the former crypto executive.

Short Sellers Jump on Crypto Stocks Despite Steep Cost of Wagers (2:44 p.m.)

Short sellers have pounced on crypto-focused equities as the digital-assets space crumbles in the wake of FTX’s public implosion.

Crypto stocks are nearly three times more shorted than the average share, even as short sellers are paying almost eleven times as much in financing costs to bet against them, according to data compiled by Ihor Dusaniwsky and Matthew Unterman at S3 Partners.

Traders banking on losses in a handful of crypto stocks, including Block Inc., Coinbase Global Inc., MicroStrategy Inc. and five others, added $55 million worth of new shorts in the week through Friday, according to S3’s analysis. Total crypto short interest for these eight stocks is more than $4.5 billion.

Silvergate Shares Slide as FTX Fallout Attracts Short Sellers (1:16 p.m.)

Silvergate Capital Corp. shares slumped, putting them on pace to lose a quarter of their value this week, as investors punished the bank for its ties to bankrupt FTX.

Shares of the company, which held deposits for FTX, dropped 9.9% to $25.14 at 1:03 p.m. in New York. Thursday’s nearly 11% drop triggered a short-sale circuit breaker. Data from S3 Partners indicates short interest levels in Silvergate are around 11% of the shares available for trading.

FTX Looks at Years of Lawsuits to Recover Billions From Customers (1:12 p.m.)

FTX’s bankruptcy opens the door to creditors’ likely lawsuits looking to claw back billions of dollars in assets that customers and insiders withdrew before the crypto company’s abrupt Chapter 11 filing.

As the company’s advisers scramble to get a handle on its finances, they’ll have a slate of bankruptcy tools available that will allow them to try to wrangle funds back into the FTX empire to try to pay all creditors, though the efforts will likely take years.

Crypto Fallout Leaves US Retiree Benefits Mostly Unscathed (12:35 p.m.)

Most of the largest US state and local government pension funds have dodged the ongoing fallout from the collapse of crypto exchange FTX by not directly investing in digital tokens. For the pensions that have dipped into the risky asset class, the investments represent just a small amount of the retirement funds’ portfolio, and much of the limited exposure is indirect via crypto-related stocks or other investment products.

Nearly all of the top 10 US pension funds by assets said they are not invested in Bitcoin or any other cryptocurrencies, according to an informal survey by Bloomberg.

House Panel Seeks Documents in Investigation on FTX Blowup (11:13 a.m.)

The chair of a House panel is asking FTX to turn over documents and information by Dec. 1 as part of its investigation into the collapse of the once-prominent crypto platform.

“FTX’s customers, former employees, and the public deserve answers,” said Representative Raja Krishnamoorthi, chairman of the House Oversight Subcommittee on Economic and Consumer Policy, in a Friday letter to former FTX CEO Sam Bankman-Fried and John J. Ray III, the new CEO and chief restructuring officer who oversaw the liquidation of Enron Corp.

He requested details on the circumstances surrounding the crypto firm’s spiral into bankruptcy last week, including an explanation of the company’s liquidity issues, how those issues of the Bahamas-based parent company affected its US arm, and details of how customer funds were being used. The subcommittee is also seeking internal documents and communications.

FTX Auditor Defends Work as New CEO Blasts Financials (10:57 a.m.)

The auditors of FTX Trading Ltd. are defending their work, even after the new management of the imploded crypto exchange lambasted the auditors in a stunning bankruptcy filing.

“We believe the financial statements of FTX Trading Ltd. as of 12/31/21 were fairly stated and we stand behind our audit opinion,” New York-headquartered accounting firm Prager Metis CPAs LLC said in a statement to Bloomberg Tax.

–With assistance from Stephen Stapczynski.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.