Two Favorites Tipped for PBOC’s Top Post as Women Also Make List

(Bloomberg) — The People’s Bank of China is likely to get a new leader next year, with speculation centering on two clear favorites to succeed current Governor Yi Gang or possibly the first woman to run the central bank in decades.

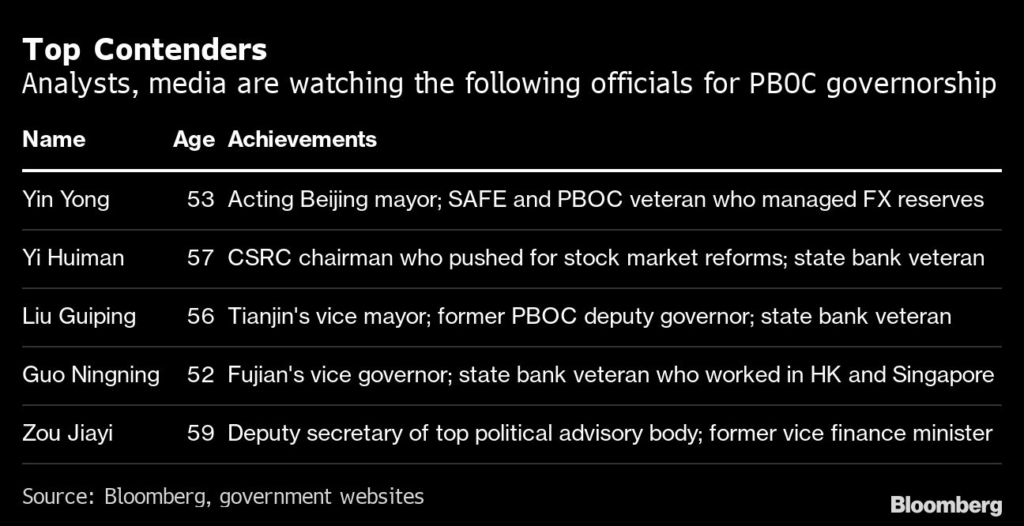

The acting mayor of Beijing, Yin Yong, and the country’s top securities watchdog, Yi Huiman, got five votes each in a survey of economists and political analysts by Bloomberg News this month.

Those two names have been making the rounds since last month, when the Communist Party’s congress signaled Yi Gang may retire. More recently, two women with experience in finance and politics, Guo Ningning and Zou Jiayi, have also been tipped, according to research firm REDD Intelligence.

The new PBOC governor, who may only be appointed in March when the legislature meets, will be tasked with navigating monetary policy for the world’s second-largest economy. The stakes are high as Beijing takes steps toward easing the two biggest risks facing the economy — Covid restrictions and a property market crisis — with investors on high alert for signs of a recovery in growth.

Unlike other major central banks like the Federal Reserve, the PBOC doesn’t have policy independence from the government. For example, it needs approval from the State Council, China’s cabinet, on major decisions regulating money supply, interest rates and exchange rates.

President Xi Jinping’s strengthened role within the Communist Party after securing a third term in power has also raised concerns that the role of the State Council and key agency officials, such as PBOC governor, may be weakened.

“Xi will be looking first and foremost for a PBOC governor who is capable of providing financial stability,” said Christopher Beddor, deputy China research director at Gavekal Dragonomics. “A major part of the PBOC’s role since 2017 has been to de-risk the financial sector, and Xi’s report at the 20th Party Congress clearly signaled that priority will continue into the coming years as well.”

Here’s a look at some of the key candidates tipped to be the next central bank governor.

Yin Yong

Xi’s strategy with political appointments has colored some of the discussion around the governor job. Yin Yong, a 53-year-old Harvard University graduate who previously worked for China’s foreign exchange regulator and the central bank, was regarded as a strong candidate before being named acting mayor of Beijing last month.

His elevation to that role signals Xi may want him for a more high-profile political role, since many senior state leaders have served as mayor — including current Politburo Standing Committee member Cai Qi and Vice President and anti-graft czar Wang Qishan.

But Yin still received five votes in the Bloomberg survey, suggesting economists think he has a good chance to become governor. Yin’s experience is well suited to the job, as he previously held a deputy governor role at the central bank and has years of experience at the State Administration of Foreign Exchange, the agency that manages the nation’s huge reserves.

If Xi wants Yin to become governor, such political maneuvering would likely keep current central bank head Yi Gang around for at least a little while longer, according to Hui Feng, co-author of “The Rise of the People’s Bank of China” and a senior lecturer at Griffith University. That’s because Xi would then be forced to look elsewhere for a new Beijing mayor, potentially delaying the PBOC process.

Yi Gang himself, meanwhile, is probably out of the running for another long-term stint, since he’s around the official retirement age and left the party’s elite central committee last month. But even that isn’t a sure bet — Yi’s predecessor Zhou Xiaochuan defied expectations back in 2013 that he would soon depart, only to extend his term another five years.

Yi Huiman

The political jockeying around Yin leaves open the possibility that Yi Huiman could be tapped as governor instead. The 57-year-old head of the China Securities Regulatory Commission was the Bloomberg poll’s only other vote-getter.

“Based on the current situation, Yi Huiman’s chances at the PBOC governorship have increased significantly,” said Bruce Pang, chief economist and head of research for Greater China at Jones Lang LaSalle Inc. He voted for Yi in the Bloomberg survey.

Unlike Yin, Yi has never worked at the PBOC. That would run against tradition, as many former PBOC leaders including Yi Gang and Zhou Xiaochuan served as deputy governors before they were promoted.

But Xi’s willingness to “ignore previous promotion norms” suggests a lack of prior PBOC experience, such as is the case with Yi Huiman, “may not be an impediment,” said Neil Thomas, senior China analyst at Eurasia Group. Thomas sees Yi as the strongest candidate, though said Xi’s norm-busting has made it harder to predict personnel movements.

Yi’s background is instead in commercial banking, having worked at Industrial & Commercial Bank of China Ltd. — the nation’s largest lender by assets — for more than three decades. His success running the CSRC may have boosted his odds, given the agency’s prominence in helping to carry out stock market reforms.

Liu Guiping

Liu Guiping, 56, is a state bank veteran who was the PBOC’s deputy governor from late 2020 until April of this year. During his time at the central bank, he pushed for a new law to better coordinate policies to maintain financial stability and prevent risks.

Liu, currently Tianjin city’s executive vice mayor, spent more than two decades working at Agricultural Bank of China Ltd., one of China’s largest state banks. That experience, though, could instead set him up to run the China Banking and Insurance Regulatory Commission, according to Pang of Jones Lang LaSalle. That agency is currently being run by Guo Shuqing, who is the PBOC’s party secretary and who just also exited party leadership.

Like Yin and Yi, Liu is also a veteran of China’s financial system and does not have significant international experience — a potential reflection of “Xi’s preference for economic statism over Western-style free markets,” said Thomas of Eurasia Group.

Guo Ningning

Elevating a woman to the post of central bank chief would be particularly notable, considering Xi’s new Politburo has excluded women for the first time in 25 years and stoked concerns about regressing gender representation.

Guo Ningning and Zou Jiayi are being considered by authorities, the research firm REDD Intelligence recently reported, citing unidentified sources. Each have extensive experience in politics or other roles involving monetary policy, banking and finance.

One of the few women leaders born in the 1970s, 52-year-old Guo is considered a member of “the Luckiest Generation” of Communist Party cadres whose careers were lifted by opportunities provided by China’s startling economic rise. Guo was promoted to an alternate member of the party’s central committee in October.

Before becoming the vice governor of Fujian province in 2018, Guo spent over two decades holding various roles at two of the biggest state-owned banks, the Agricultural Bank of China and Bank of China Ltd. She also holds a PhD in economics from the prestigious Tsinghua University in Beijing.

Guo is also media-savvy: She famously feasted on eels during a live stream in 2020 to promote local seafood on the e-commerce platform Taobao.

F

Zou, 59, is the deputy secretary-general of the the Chinese People’s Political Consultative Conference, a top political advisory body. From 2018 to 2021, she was a vice finance minister, and for part of that time she was also a member of the PBOC’s monetary policy committee.

She holds a master’s degree in economics from the Chinese Academy of Social Sciences, and spent most of her career at the Ministry of Finance in departments related to international economic relations. She speaks fluent English and served as the executive director for China at the World Bank from between 2005 and 2009.

While not a member of the Politburo, Zou was promoted to the Communist Party’s elite central committee in October — one of just a handful of women to achieve that distinction.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.