(Bloomberg) — Former FTX CEO Sam Bankman-Fried said in a tweet that he made a mistake on the cryptocurrency exchange’s leverage levels. It was $13 billion, not about $5 billion.

Separately, Gemini Trust Co., the cryptocurrency platform run by the Winklevoss brothers. said in a tweet that its exchange is fully back online hours after the company said it paused withdrawals on its lending program. Gemini is a lender to crypto brokerage Genesis, which suspended redemptions at its lending business after facing what it described as “abnormal withdrawal requests” in the aftermath of the collapse of FTX.

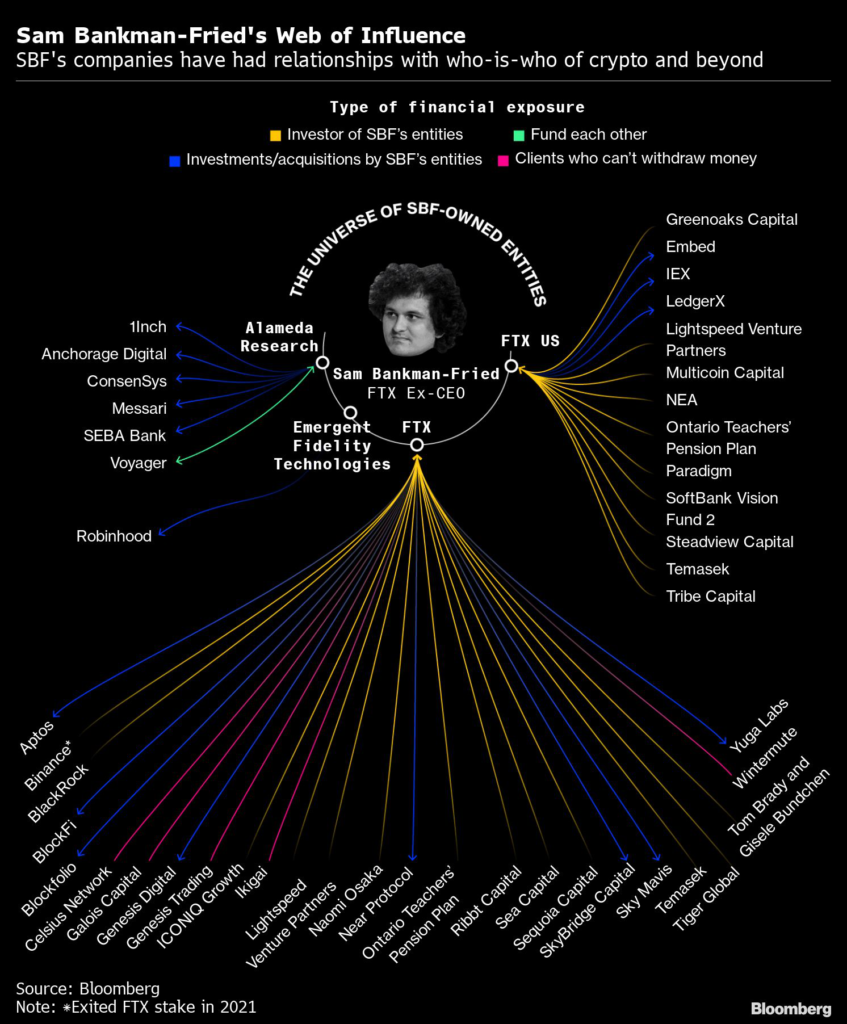

Meanwhile, Singapore’s state-owned investor, Temasek International, invested $200 million to $300 million in cryptocurrency giant FTX before its implosion and is preparing to write down the entire bet, people familiar with the matter said.

The fallout from the crisis is threatening the future of crypto lenders like BlockFi Inc. and Voyager Digital Ltd. Digital-asset markets extended losses Wednesday morning, with Bitcoin down 2% at 1:34 p.m. New York time.

Key stories and developments:

- Singapore’s Temasek to Write Down Over $200 Million in FTX

- FTX Leaves an Empty Black Box Where Due Diligence Used to Be

- FTX Hacker Emerges With a $288 Million Stash of the Token Ether

- Matter Labs Raised $200 Million Just Before Crypto Market Chaos

- FTX’s Crypto Kids Came Dangerously Close to Upending Futures

(Time references are New York unless otherwise stated.)

SBF Mistaken About FTX’s Leverage Levels (2:25 p.m.)

Bankman-Fried says he was mistaken about the cryptocurrency exchange’s leverage levels, thinking it was about $5 billion when it was $13 billion.

In his latest series of tweets explaining how FTX imploded, Bankman-Fried says the company got “overconfident and careless.”

Gemini Exchange Back Online (1:31 p.m.)

Gemini says its exchange is fully back online and that all customer funds held on it are “available for withdrawal at any time,” it said in a tweet.

Senate Banking Committee Hearing (1:18 p.m.)

Senate Banking Committee Chairman Sherrod Brown said he plans a hearing on the FTX exchange collapse before the end of the year.

Genesis Hires Alvarez, Cleary Gottlieb (10:29 a.m.)

Crypto brokerage Genesis is working with financial and legal advisers to explore options as it halts redemptions and originations at its lending business amid a liquidity crunch.

The company hired Alvarez & Marsal and law firm Cleary Gottlieb Steen & Hamilton for advice, according to a spokesperson for Digital Currency Group, the parent of Genesis.

Jay Sidhu’s Bank Says It Dodged the Crash (10:02 a.m.)

No US regional bank stock climbed higher during last year’s crypto mania than Customers Bancorp Inc. Now, the bank built by finance veteran Jay Sidhu and other firms riding the digital wave are trying to distance themselves from the crisis created by the unraveling of FTX’s empire.

“We have no exposure associated with FTX,” Sam Sidhu, Customers Bancorp’s chief executive officer and Jay Sidhu’s son, said in an interview, emphasizing his bank’s exposure was limited because it’s a “new entrant” in the market. “We’re still building our business and taking market share, and people are migrating over to us.”

Hearing Set for December (10:01 a.m.)

The House Financial Services Committee will hold a hearing in December on the collapse of cryptocurrency platform FTX, according to committee statement.

FTX and Celebrity Backers Sued (9:15 a.m.)

FTX and former chief executive officer Sam Bankman-Fried were sued by an investor over claims that the cryptocurrency exchange now in crisis targeted “unsophisticated investors” using celebrity endorsers including Tom Brady and Stephen Curry, who are also named as defendants.

In a complaint filed Tuesday in federal court in Miami, Oklahoma resident Edwin Garrison is asking to represent a class of “thousands, if not millions, of consumers nationwide.” That includes all investors in the US who were enrolled in yield-bearing FTX crypto accounts, which he alleges constitute unregistered securities in violation of US and Florida laws.

Winklevoss’ Gemini Pauses Withdrawals (8:35 a.m.)

Gemini Trust Co., the cryptocurrency platform run by the Winklevoss brothers, has halted withdrawals from its Earn program after partner Genesis Global did the same.

This does not impact any other Gemini products and services, the company said in a statement.

Genesis Suspends Withdrawals (8:00 a.m.)

Crypto brokerage Genesis is suspending redemptions and new loan originations at its lending business after facing what it described as “abnormal withdrawal requests” in the aftermath of the collapse of FTX.

The withdrawal requests exceeded current liquidity at Genesis Global Capital, the lending arm, according to interim Chief Executive Officer Derar Islim. Genesis has hired advisers to explore all possible options, including raising new funding, and will deliver a plan for its lending business next week, Islim said.

Temasek Takes a Hit (6:45 a.m.)

Temasek invested between $200 million and $300 million in FTX before its implosion, according to people familiar with the matter.

Temasek is now preparing to write off the entire amount, one of the people said, asking not to be identified as the matter is private. Another backer, Sequoia Capital, wrote down the full value of its $214 million bet on the exchange, while a person with knowledge of the situation said SoftBank Group Corp. is expecting a loss of around $100 million on its investment.

FTX Hacker’s Haul (6:05 p.m. HK)

The hacker who raided Sam Bankman-Fried’s collapsed crypto exchange FTX is now one of the world’s biggest holders of the token Ether.

A wallet linked with the exploit swapped about $49 million of stablecoins — mainly Dai — for Ether on Tuesday, security specialists PeckShield said.

Wallets on FTX were drained of over $663 million in tokens, with $477 million of that suspected to have been stolen and the remainder moved into secure storage by FTX, according to blockchain specialist Elliptic.

Novogratz Warns Worst May Lie Ahead (6 p.m. HK)

Mike Novogratz said the worst of the crypto crisis in the wake of the FTX exchange’s collapse may yet unfold. Galaxy, the crypto financial services firm founded by Novogratz, last week disclosed $76.8 million in exposure to FTX.com

Novogratz was speaking at a conference on Wednesday alongside Binance Holdings Ltd.’s Chief Executive Officer Changpeng ‘CZ’ Zhao. The Binance CEO said he saw a lot of investor interest in a crypto industry recovery fund he plans to set up to assist otherwise strong projects that are facing a liquidity squeeze.

Crypto Exchange AAX Needs Capital (5:55 p.m. HK)

Resuming operations on the cryptocurrency exchange AAX depends on whether it can raise funds, the company said. Hong Kong-based AAX suspended withdrawals on Monday citing a glitch in a system upgrade.

“If AAX is unable to secure funding to enable us to restart operations, AAX is committed to initiating legal procedures to secure and ensure the distribution of asset,” the company said.

Most Bitcoin Retail Buyers Lost (2:20 p.m. HK)

A study of how retail investors use cryptocurrency exchange apps suggests about three-quarters have lost money on Bitcoin, according to the Bank for International Settlements.

Data spanning 95 countries from 2015 to 2022 indicates the vast majority of app downloads occurred when Bitcoin’s price was above $20,000, the working paper from the Basel, Switzerland-based BIS says.

The world’s largest token has plunged over 70% from a record hit about a year ago, pressured by rapidly tightening monetary policy and a series of huge blowups at crypto outfits, most recently FTX.

FTX Digital Markets Files for Chapter 15 (noon HK)

Bahamas-based FTX Digital Markets Ltd. has submitted a Chapter 15 petition for recognition of a foreign proceeding in the Southern District of New York, according to a filing on the court’s website.

It’s a subsidiary of FTX Trading Ltd., which filed for Chapter 11 bankruptcy on Nov. 11.

–With assistance from Amanda Fung, Sidhartha Shukla and Suvashree Ghosh.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.