Twitter Buyout Revives $12.5 Billion Headache for Wall Street Banks

(Bloomberg) — Elon Musk’s shock proposal to proceed with his acquisition of Twitter Inc. for the original offer price poses a headache at the worst possible time for Wall Street banks already struggling to offload billions of dollars in buyout debt they committed to in better times.

After months of legal drama in an attempt to back out of the deal, billionaire Musk is now willing to buy the social-media giant for $54.20 a share. In a letter his lawyers sent to Twitter, Musk’s acquisition is now pending “receipt of the proceeds of the debt financing.”

That means it’s now time for a group of Wall Street banks led by Morgan Stanley to step up. They committed debt financing for the deal back in April, with the intention to sell most of that to institutional investors.

If terms of the original $12.5 billion financing package remain the same, bankers may struggle to sell the risky Twitter buyout debt just as credit markets begin to crack. With yields at multiyear highs, they’re potentially on the hook for hundreds of millions of dollars of losses on the unsecured portion alone should they try to unload it to investors. That’s because they would almost certainly have to offer the debt at a steep discount.

The Twitter debt package is the largest in a roughly $51 billion pipeline of risky committed financings that banks need to sell to asset managers, according to Deutsche Bank AG estimates.

It all threatens to fuel a wider fallout in corporate debt markets. New issues have come to a virtual standstill given muted investor appetite and rising balance-sheet constraints at the big banks as the Federal Reserve ramps up interest rates.

Read more: Confused by Musk’s Twitter LBO? Here’s What’s Weird: QuickTake

“It’s similar to a vegetarian going to a steakhouse: Very limited appetite,” said John McClain, a high-yield portfolio manager at Brandywine Global Investment Management, referring to investor demand for buyout debt. “Given the incremental company specific news flow since the deal was agreed to — combined with the meaningful deterioration in the economy — lenders will be very hesitant to provide financing.”

The most recent version of the Twitter debt package announced in April includes a $6.5 billion leveraged loan, $3 billion of secured bonds, and another $3 billion of unsecured bonds, with the latter particularly tricky to sell in recent months as the capital structure is riskier.

Banks had originally planned to sell all that debt to institutional asset managers. In addition, banks are providing a $500 million revolving credit facility that they plan to hold.

A spokesperson for Morgan Stanley declined to comment. Representatives for Twitter and Musk did not immediately respond to a request for comment.

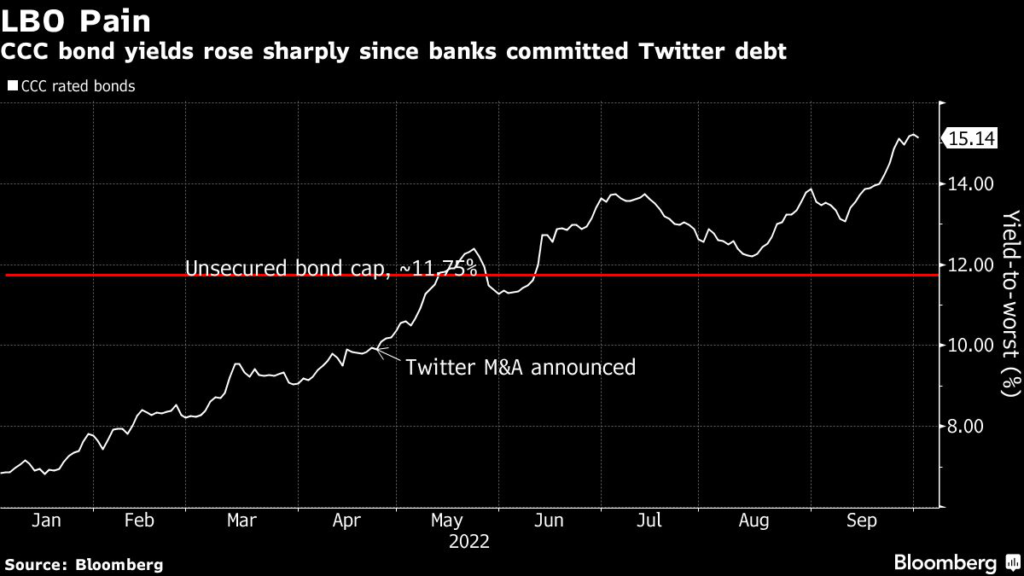

The group of banks was already facing potential losses of hundreds of millions of dollars on the riskiest unsecured bonds if they had to sell the debt at current market levels. They promised a maximum interest rate of about 11.75% on the unsecured bond portion, Bloomberg reported, but CCC debt now trades on average at around 15%, according to Bloomberg data.

Read more: Musk’s Debt Bankers Would Avoid Steep Losses If Deal Fails (1)

Twitter shareholders voted Sept. 13 to accept the buyout offer as Musk originally submitted it. Depending on the closing date of the deal, banks will have a limited amount of time to offload the debt to investors. That would force them to fund the financing themselves — as is expected on another big buyout deal in the pipeline for Nielsen Holdings Plc.

Wall Street has been struggling to offload leveraged buyout debt in recent months. Part of the package for Citrix Systems Inc., for example, sold in September at a steep discount and left the banks holding about $6.5 billion of debt and realizing roughly $600 million in losses. Shortly after, a group of banks got stuck with roughly $4 billion of bonds and loans tied to an Apollo Global Management Inc.-backed buyout that wasn’t able to garner much demand and was pulled from the market last week.

As the economy continues to tip toward a downturn, investors have shied away from risky transactions and are instead putting money into higher-rated credits. Some high-yield managers are even allocating cash to investment-grade obligations given that those companies are best positioned to weather a recession and are offering yields at levels not seen in more than a decade.

(Updates throughout with Musk’s official letter he is going through with the acquisition.)

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.