Shanghai’s Two-Month Lockdown Is Still Rippling Through Economy

(Bloomberg) — Three months after Shanghai lifted an unprecedented Covid lockdown that lasted more than 60 days, businesses in China’s richest and biggest consumer market are still struggling with a sluggish recovery as lingering restrictions continue to deter people from going about their normal lives.

Though city-wide curbs on movement were scrapped on June 1, the ordeal hasn’t ended altogether for Shanghai’s 25 million residents. China’s Covid-Zero policy still requires localized lockdowns of neighborhoods and apartment blocks whenever cases emerge, making that quick trip to a shop or a mall challenging. Then there’s the need for regular testing to use public transportation or to enter indoor spaces such as office buildings and restaurants, not to mention quarantine for as long as 14 days at a government facility in some instances.

As a result, demand for everything from dining out to movies and tourism are still far below pre-lockdown levels, while some indicators show Shanghai is taking longer to recover than Hong Kong and Singapore after rules were eased in those cities. Retail sales in the city dropped 4.3% in June from a year earlier and rose a meager 0.3% in July, following an average 35% slump in the preceding three months starting March, when the outbreak began.

Wang Yihan, owner of two role-playing game venues in the city, is praying for “no more Covid comeback.” “It’s just so difficult to get enough cash flow,” she said, adding about 60% of peers she knows have shut their businesses in recent months. “Even if we survive now, we can’t make it through if another lockdown comes.”

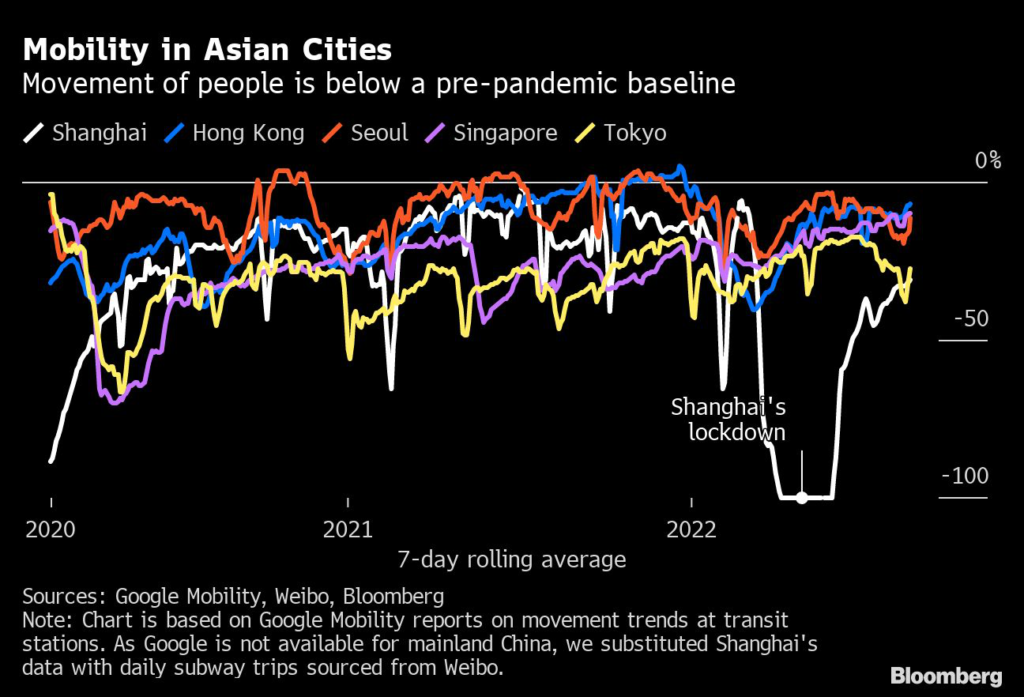

These five charts show how Shanghai is reeling from the aftermath of the lockdown:

1. Impact on Retail

Unlike Singapore or Hong Kong — even though these cities also placed strict social distancing rules — Shanghai’s recovery hasn’t been as swift when it comes to post-easing retail sales. For instance, Hong Kong experienced a wave of outbreaks earlier this year, but started to gradually ease restrictions from late March by lifting flight bans, cutting quarantine days and allowing dine-in services. Monthly retail sales returned to growth in April right after. In Singapore, where curbs also caused frustration among residents and businesses last year, growth barely stalled and accelerated immediately after the island-nation announced significant easing in March.

2. Mall Vacancies

Shopping malls in Shanghai are seeing a surge in vacancies that climbed to 7% in the second quarter, above a “warning line” of 5%, after Covid Zero lockdowns hammered consumer demand, China Real Estate Information Corp. said late August, citing research of 20 major malls. Worst-hit Super Brand Mall, which sits at the heart of Shanghai’s Lujiazui financial district, saw 34% of its shops shuttered, CRIC said. The 2.7-million-square-feet mall, just a few minutes away from the world’s second-tallest office tower, had been one of the most popular shopping centers since it opened more than two decades ago.

3. Consumer Spending

While people are starting to go out to have some fun, data still show Shanghai consumer spending — which usually centers around products linked to socializing, like cosmetics and apparel — still has a long way to return to normal.

Food and daily necessities remain the key driver of the post-lockdown recovery in Shanghai. Consumer staples including household care products such as tissue paper and laundry detergents, and in-home food and drinks are the most popular shopping categories, according to monthly consumer surveys compiled by consultancy Mintel by interviewing 100 Shanghai residents.

Tourism is another sector that still suffers from weak consumer sentiment in China, as recent Covid outbreaks in some of the top domestic travel destinations such as Hainan and Xinjiang further scare visitors from making travel plans.

China’s Covid-Hit Tourism Season Deals Fresh Blow to the Economy

Summer holiday travel bookings to Shanghai, which has usually been the top destination for Chinese visitors during the holiday period, fell 70% this year, according to a Ctrip survey done in July, though the city’s popularity picked up in the third quarter. Among Shanghai consumers, only half of interviewees in Mintel surveys said they spent on tourism in August, compared with February.

4. Hotels and Restaurants

The willingness to increase spending on dining out and entertainment such as cinemas and exhibitions, has started to pick up, though they were still below pre-lockdown levels in August.

The city’s hospitality and restaurant sales still posted 37% and 21% drop in June and July, after slumping more than 60% during the lockdown in April and May. Box-office revenue for Shanghai in July just reached less than half of last year’s level, according to ticketing platform Maoyan Entertainment. August sales returned to about the same level from a year ago.

“The lockdown hit the restaurant sector very hard in recent months,” said Cao Zhehui, general manager of Shanghai-based Haisu Foods, which supplies meals to both international and local hotels, restaurants and airports. “The recovery is still gradual,” he said, adding he’s positive over the long term, as about 70% of his business was back as of late August.

5. Traffic and Flights

The city’s traffic data point to the first positive sign that Shanghai is returning to normal, but that has also taken almost 3 months. Median metro traffic and daily flights in August both reached over 80% of the number for the first two months this year. That indicates most residents have been going to work as usual, likely due to limited adoption of work-from-home protocols by Chinese companies, although they are still reluctant to spend. But Shanghai’s metro mobility, which in 2021 almost returned to pre-pandemic level just like other major Asian cities such as Hong Kong and Seoul, was in late August still down nearly 30% from that baseline.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.