Musk Effort to Void Twitter Buyout Sets Up Delaware Court Fight

(Bloomberg) — Elon Musk’s move to dump his $44 billion deal for Twitter Inc. sets the stage for a titanic legal battle in a Delaware court that typically frowns on efforts to back out of merger agreements.

Minutes after Musk disclosed his intention to exit the deal, Twitter Chairman Bret Taylor responded with an unequivocal threat to take the world’s richest person to court.

“We are committed to closing the transaction on the price and terms agreed upon with Mr. Musk and plan to pursue legal action to enforce the merger agreement,” Twitter said in a statement. “We are confident we will prevail in the Delaware Court of Chancery.”

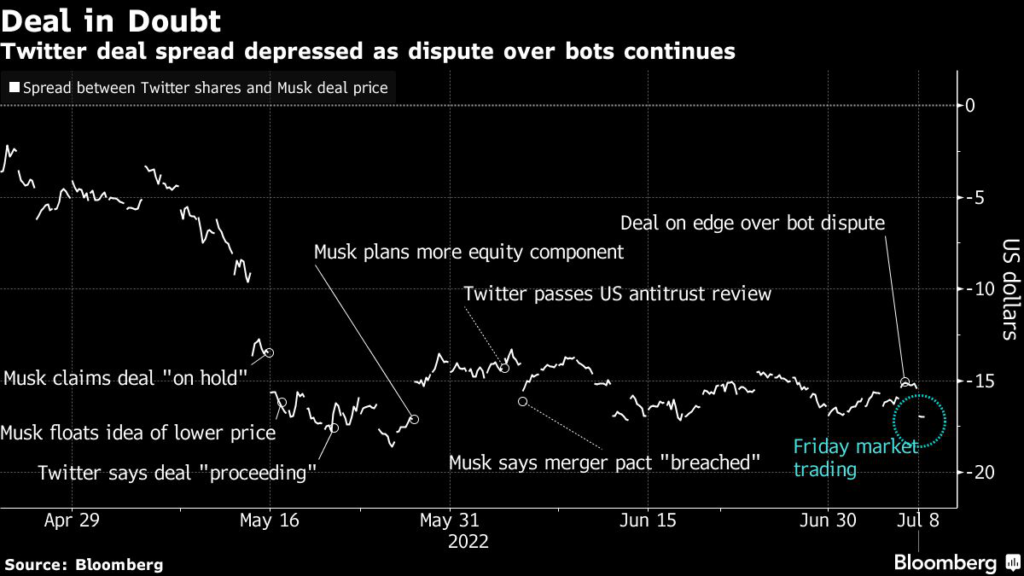

The Tesla Inc. co-founder is trying to blow up his own $54.20-a-share offer, claiming Twitter failed to fully disclose how much of the platform’s traffic is driven by spam and fake accounts known as bots. Twitter, now trading below $40 a share, has countered that it has provided Musk with that information and he’s obligated to complete the deal reached in April.

As with many other high-profile transactions, Twitter and Musk agreed that any legal disputes must be heard by Delaware courts, which are well versed in quickly sorting merger-and-acquisition complexities. Based on previous merger fights, efforts to terminate a deal can play out within a few months, often ending with settlements to avoid further wrangling.

Negotiating Ploy

Musk’s decision to publicly pull the plug on the deal is probably nothing more than a negotiating ploy, said Charles Elson, a retired University of Delaware professor and former head of the school’s Weinberg Center for Corporate Governance.

Despite Musk’s assertion that Twitter’s handling of the bots issue amounts to breach of the buyout agreement that justifies canceling the deal, he and his lawyers know they’ll have an extremely difficult time making that claim, Elson said.

“This is not a material adverse change,” Elson said. “That’s just a negotiating position. He knows the Delaware courts are extremely reluctant to find something like that in these deals.”

In his letter Friday, Musk repeated his claims that Twitter has failed to show that no more than 5% of its users are automated bots. He also contends that Twitter broke the agreement by deviating from its normal course of business by firing executives and imposing a hiring freeze.

Following Musk’s disclosure, Twitter’s shares fell about 5% after the close of regular trading. The shares, which have fallen about 15% this year, closed regular trading Friday at $36.81, giving the company a market value of $28 billion.

Chancery Powers

Any suit by Twitter or Musk over enforcing or voiding the deal will be heard by a Delaware Chancery Court judge. The state is the corporate home to more than half of U.S. public companies, including Twitter, and more than 60% of Fortune 500 firms. There, chancery judges — business law experts — hear cases without juries and can’t award punitive damages.

Under Delaware court rules, either Musk or Twitter would be able to ask a judge to put its case on a fast track, accelerating deadlines for exchanges of pre-trial information and enabling a quick trial. Under state law, judges can order parties to consummate a merger if the objector fails to make a legitimate case for walking away.

The judges also have a say over whether breakup fees must be paid. In the Musk-Twitter deal, that fee is for $1 billion.

Un-Patchable Hole

To escape the deal, Musk must prove some “unexpected fundamental, permanent adverse event” has occurred that blew an un-patchable hole in the transaction, said Larry Hamermesh, a University of Pennsylvania law professor.

Chancery judges have only recognized one case in which a so-called material adverse event occurred.

That case involved Fresenius SE’s $4.3 billion buyout bid in 2018 for rival drugmaker Akorn Inc. A Delaware judge blessed Fresenius’ decision to walk away from the deal after finding Akorn executives hid an array of problems that cast doubt on the validity of data backing up approval for some drugs and profitability of its operations.

No matter what happens in the legal arena, the jockeying over Twitter has left some deals lawyers marveling over Musk’s chutzpah and predicting he’ll get a price cut.

“Even after Twitter’s statement that it is sticking to its guns, the board might well be tempted to take a haircut in an effort to end what is, I think, perhaps the weirdest major-merger process in the last 50 years, if not ever,” said Robert Profusek, head of the merger-and-acquisition department at the Los Angeles based law firm Jones Day.

Musk is slated to speak Saturday at Allen & Co.’s Sun Valley Conference in Idaho and the deal is certain to be the elephant in the room regardless of whether he addresses it directly, especially with Twitter Chief Executive Officer Parag Agrawal also present at the conference.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.